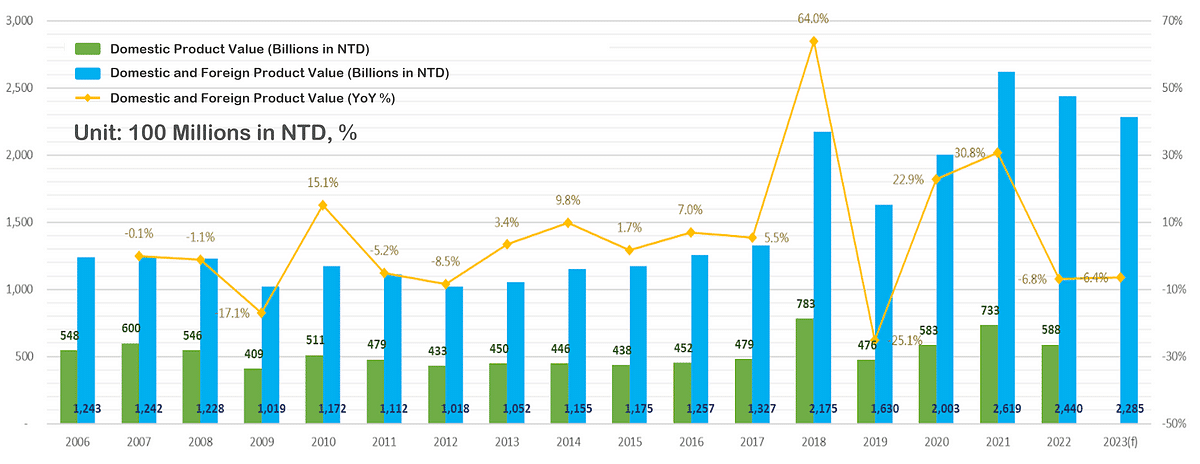

Following a period of supply shortages and price increases in 2018, the passive components industry in Taiwan experienced another peak due to the COVID-19 pandemic. Driven by trends such as remote work and distance learning, the output value reached NT$200.3 billion, marking a 22.9% YoY increase, and in 2021, it further rose to NT$261.9 billion, a 30.8% annual increase, reaching a nearly 15-year high.

Taiwan’s Passive Component Industry Output and Projected Trends. Source: TEJ Dataset

However, the industry faced challenges in 2022 with the outbreak of the Russia-Ukraine conflict, leading to surging energy prices and exacerbating global inflation. Many central banks worldwide implemented interest rate hikes, dampening the initial expectations of post-pandemic economic recovery. Consequently, demand for end products declined in the latter half of 2022, and manufacturers encountered inventory clearance issues. Despite these challenges, the industry maintained an output value of NT$244 billion in 2022, marking a 6.8% YoY decrease.

Prospects for 2023 appear challenging, with high-interest rates and high inflation creating a difficult environment for end-product demand to rebound significantly. On the supply side, manufacturers have reduced production to adjust inventory, causing the 2023 output value to drop further to NT$228.5 billion, a 6.4% annual decrease. As of today, referring to publicly traded companies (referred to as the industry), self-reported revenues for the first half of 2023 reached approximately NT$111.7 billion, showing a significant decline of 15.57% YoY. Even with the traditionally strong third quarter, it’s challenging to make up for the first-half shortfall due to limited downstream demand. The industry is expected to experience a double-digit decrease, with an annual decline of at least 10% or more. Faced with the industry headwinds, how are Taiwanese passive component manufacturers faring recently? How has the expansion plan of various manufacturers been impacted following the US-China trade war? This article will provide insights into the recent status and future outlook of Taiwan’s passive component industry by analyzing profit margins and capital expenditure, keeping you updated with the latest information on the passive components market and industry!

Dominance and Consolidation of Industry Giants

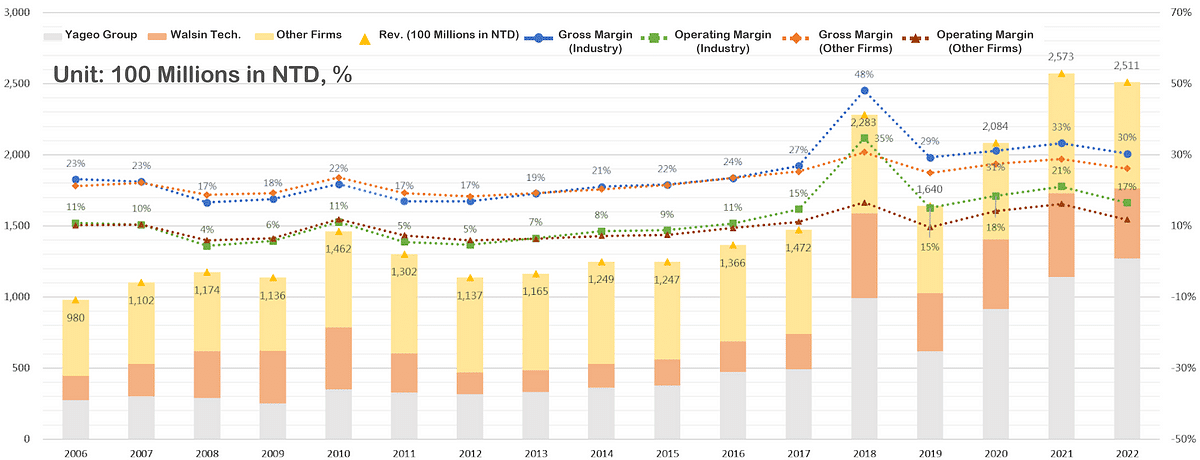

The passive component industry is marked by technological maturity and fierce competition, where the adage “the bigger, the better” often holds true. In Taiwan, this industry has undergone significant consolidation over the years, gradually falling under the dominion of two major conglomerates: the Yageo Group and the Walsin Tech Group. In 2006, the combined revenue of these two giants reached approximately 44.5 billion NTD, constituting about 45% of the industry’s total revenue.

As depicted in the chart below, starting in 2016, the Yageo Group embarked on a series of acquisitions, including local competitors such as Jamicon, Mag Layers, Magic Tech, Bothhand, BrightKing, and more. Furthermore, they extended their reach to European and American companies, including Pulse and Kemet. By 2022, the Yageo Group’s revenue had surged to nearly 127 billion NTD, commanding a significant 51% share of the industry’s revenue and propelling it to become the world’s third-largest passive component manufacturer, surpassing Japan’s TAIYO YUDEN.

On the other hand, the Walsin Tech Group’s acquisition targets included local companies such as Inpaq, Joyin, and Japanese firms like Soshin and Matsuo Electric. While the scale of their acquisitions may be relatively smaller compared to the Yageo Group, the Walsin Tech Group’s revenue, as of 2022, still amounted to around 49.2 billion NTD, constituting about 20% of the industry’s total revenue.

The combined revenue of these two major conglomerates alone reached approximately 176.2 billion Taiwanese dollars, nearing a substantial 71% share of the entire industry.

Trends in Revenue and Profitability of the Passive Components Industry in Taiwan. Source: TEJ Dataset

Overview of Passive Component Mfrs.’ Profitability

As depicted in the chart above, between 2006 and 2016, the average gross profit margin and operating profit margin for the entire industry, including the two major conglomerates, stood at approximately 20% and 8%, respectively. For other manufacturers (referred to hereinafter as “other firms”), the average gross profit margin and operating profit margin were around 21% and 8%, showing a relatively minor difference. However, in the period from 2017 to 2018, several factors came into play. TAIYO YUDEN, a prominent Japanese manufacturer, gradually withdrew from the standard component market. Additionally, the surge in cryptocurrency prices fueled a boom in digital mining, leading to a substantial increase in demand for computer-related equipment such as GPUs and power suppliers. This indirectly led to an expansion of the supply-demand gap in passive components, resulting in a price surge due to shortages.

The two major conglomerates, benefiting from their scale advantages, experienced significant advantages during this period. In 2018, the industry’s overall gross profit margin and operating profit margin jumped to an astonishing 48% and 35%, respectively. This outperformed other firms by 17% in gross profit margin and 18% in operating profit margin, showing a considerable difference. Although the cryptocurrency mining frenzy waned after 2019, the opportunities brought about by the ICT product demand, owing to the unforeseen pandemic, helped slow down the cooling of the passive component market. From 2020 to 2022, the industry’s average gross profit margin and operating profit margin maintained at 32% and 19%, respectively, while other firms’ average gross profit margin and operating profit margin were 27% and 14%, preserving a 5% gap. This indicates the sustained profitability advantage of the two major conglomerates over other manufacturers.

Overview of Passive Component Mfrs.’ Capital Expenditure

In addition to acquisitions, the two major conglomerates have continuously expanded their production capacity. Between 2006 and 2016, the industry’s expenditure on purchasing fixed assets, including real estate, facilities, and factories (referred to as “fixed asset expenditure”), ranged from 6.2 billion to 15.1 billion NTD, averaging approximately 10 billion NTD annually. Notably, the Yageo Group accounted for an average of about 30%, while the Walsin Tech Group averaged about 21%. The combined share of these two conglomerates reached a significant 51%.

Trends in CapEx in the Passive Components Industry in Taiwan. Source: TEJ Dataset

As illustrated in the chart above, in 2018, driven by the profitability resulting from the surge in passive component demand, the entire industry aggressively expanded its production capacity. This led to a substantial increase in fixed asset expenditure, soaring to 28.9 billion Taiwanese dollars, marking an astonishing 84% YoY growth. The Yageo Group contributed roughly 14 billion NTD, comprising 48% of the total, while the Walsin Tech Group invested approximately 7.4 billion NTD, making up 26% of the total. Together, these two conglomerates accounted for around 21.4 billion NTD, elevating their combined share to 74% and significantly widening the gap with other manufacturers. However, as the excess capacity gradually became evident, coupled with market conservatism during the early stages of the pandemic, fixed asset expenditure across the industry started to converge from 2019 to 2020. Nonetheless, the industry still maintained fixed asset expenditures above 20 billion NTD.

In 2021, the surge in demand for ICT products, combined with supply chain disruptions, resulted in downstream manufacturers stockpiling materials and multiple order placements. Responding to the optimistic market, the entire industry again increased its fixed asset expenditure to 32.9 billion Taiwanese dollars, marking a 47% YoY increase. In 2022, despite the looming shadows of global conflicts and inflation, the postponed equipment purchases from the early pandemic period gradually materialized as lockdowns were lifted, bringing fixed asset expenditures to approximately 28 billion NTD, on par with the levels seen in 2018. As the market rapidly shifted in terms of supply and demand, the suddenly apparent excess capacity became a significant concern.

Expansion Status and Future Prospects

As the Russia-Ukraine conflict rages on, it has evolved into an enduring war of attrition, leading to sustained global economic pressures such as inflation and interest rate hikes. Consequently, end-user consumer demand has stagnated and even waned. Furthermore, in the midst of the ongoing battle for technological supremacy between China and the United States, Taiwanese electronics manufacturers have been compelled to establish new production capacities outside the cross-strait region. As cross-strait travel and cargo movement return to normal with the pandemic’s resolution, electronic contract manufacturers like Hon Hai (2317), Pegatron (4938), Quanta (2382), Kinpo (2312), Compal (2324), Wistron (3231), and Inventec (2356) have expedited their global expansion, thereby influencing the migration of upstream component supply chains to various locations.

Passive components, due to their small and lightweight nature and their non-critical status in the China-U.S. tech dispute, have prompted most manufacturers to adopt a cautious stance toward expanding or relocating their production bases. Therefore, aside from the two major conglomerates that already have manufacturing facilities worldwide, most other firms are still in a wait-and-see mode. Some prefer to expand to domestic areas with more familiar political and economic environments, such as Holy Stone and Tai Tech. However, a few scattered manufacturers with a higher concentration of production and sales in mainland China have taken precautions by announcing the establishment of subsidiaries in Southeast Asia. This includes Ta-i and Thinking Electronic, which are expected to invest $10 million and $27 million USD, respectively, in new facilities in Vietnam, and Lelon, which plans to invest 260 million Thai Baht in a new Thai plant. The related capacity expansion is estimated to begin in 2024.

In summary, it is now evident that the passive component industry is experiencing a downturn in 2023. However, whether 2024 will mark a recovery remains uncertain. The two major conglomerates, with diverse product portfolios and economies of scale, can adapt to challenges and potentially sustain growth through acquisitions. On the other hand, other firms should consider preserving their resources to weather the economic challenges and patiently await the recovery.