Table of Contents

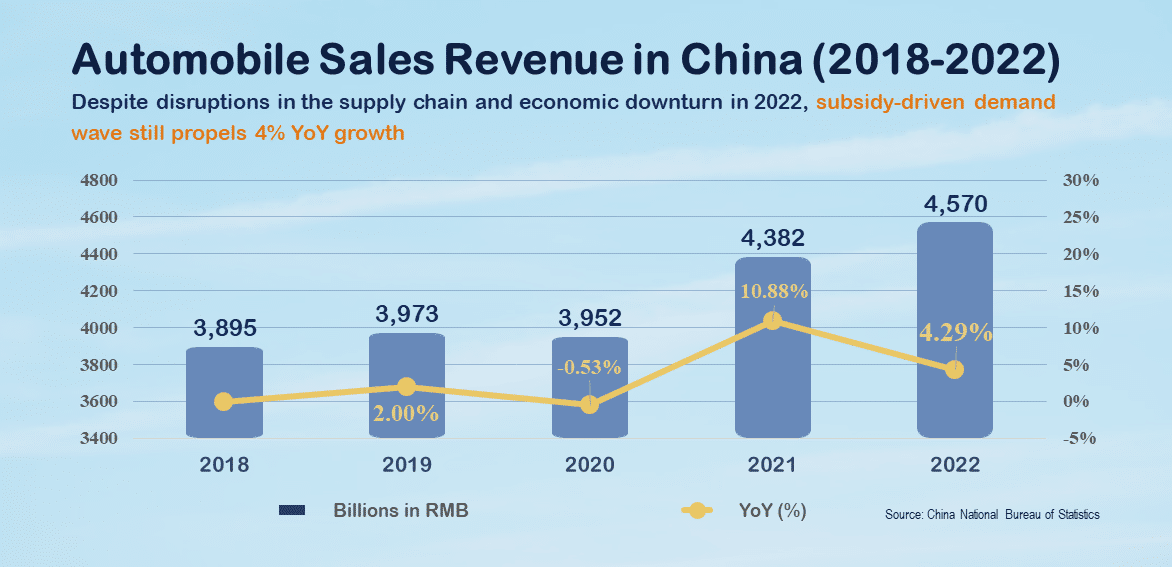

In 2022, the Chinese car manufacturer faced continued shortages of automotive chips, coupled with the challenges posed by the Russia-Ukraine conflict and domestic lockdown measures. It was anticipated that these factors would lead to negative impacts such as supply chain disruptions and economic downturn. However, in the latter half of 2022, the Chinese government proactively implemented various subsidy policies to encourage the growth of the automotive industry and stimulate market consumption. As a result, the year witnessed a modest growth of 4% in overall performance (as shown in the table below).

However, utilizing subsidy policies to incentivize consumer car sales essentially preloaded future demand. The purchase subsidy for EVs also phased out starting in 2023. The aftermath of the stimulus effect will follow suit once these policies wind down. Moreover, China’s “zero-COVID” strategy has just been fully lifted, yet consumer willingness to spend remains low. These factors collectively contribute to a lackluster environment in China. Various car manufacturers are adjusting their car prices in a bid to survive the wave of industry consolidation. In such a scenario, can the Chinese automotive market see a resurgence in 2023? How will the changing market dynamics impact Taiwanese automotive component suppliers? In this article, we provide you with insights into the underlying reasons for the price wars, delve into the effects of this year’s price wars on Taiwanese automotive component manufacturers, helping you stay updated with the latest developments in the Chinese automotive market and the automotive component industry!

Since the Chinese government’s decision to promote the EV industry in 2010, the growth in production and sales of EVs in China has far outpaced other regions globally. By 2015, sales had reached 330,000 units, establishing China as the world’s largest market for EVs. Tracing back, whenever subsidy amounts were reduced, there was a short-term surge in sales as consumers rushed to make purchases, resulting in an overextension of sales for the upcoming months. However, with the phase-out of subsidy policies starting this year, pricing strategies among major automakers have begun to shift, with impacts extending across the entire Chinese automotive market.

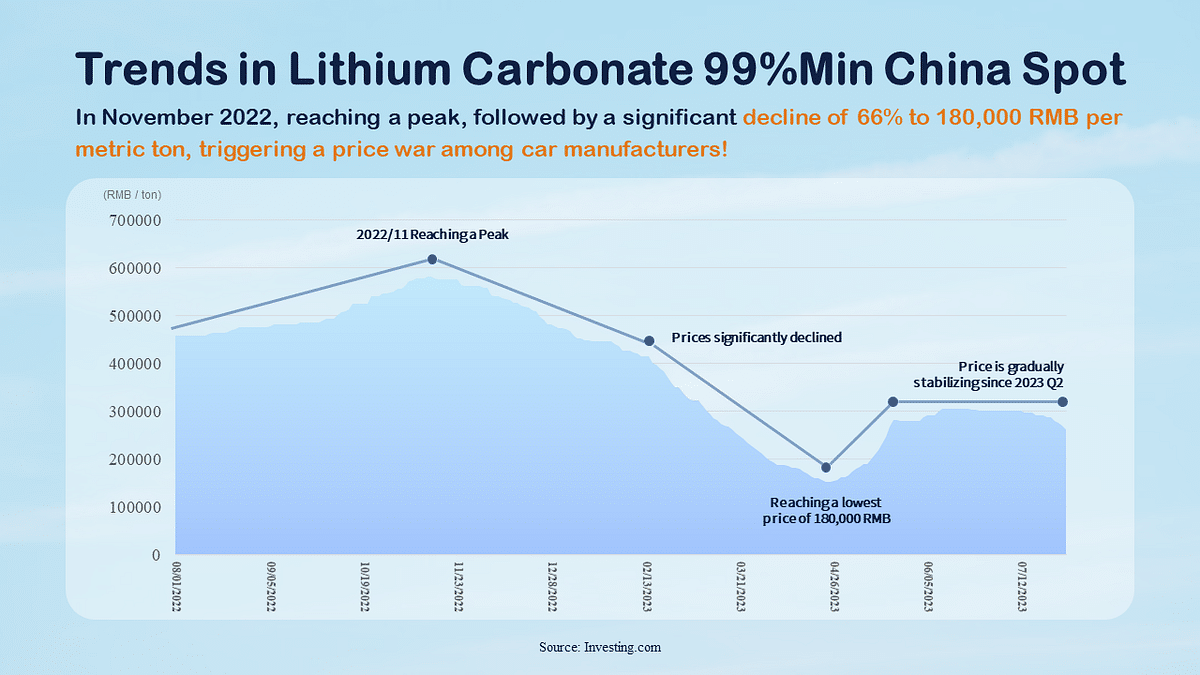

First and foremost, BYD announced at the end of 2022 that it would raise prices from 2023 onwards to reflect the rising costs of battery materials. Yet, due to the subdued market conditions resulting from the subsidy withdrawal, end-demand has not seen improvement. On the other hand, Tesla adopted a contrasting strategy by lowering prices, posing a threat to other automakers’ sales. This led BYD to adjust its pricing strategy shortly afterward and opt for a lower pricing strategy.

According to statistics from the China Passenger Car Association (CPCA), the accumulated sales volume for China’s automotive market in the first quarter reached 4.26 million units, marking a YoY decrease of 13.4%. Following BYD’s price hikes, other automakers observed this scenario while also considering that battery raw material prices had significantly fallen. As a result, they gradually initiated a price war in the second quarter.

In this ongoing price war, the primary objective for each automaker is to secure market share as a means of survival. For the upstream automotive component manufacturers, there are two significant risks they encounter: (a. ) reducing product prices to avoid losing orders and (b. ) customer market exit due to poor operations.

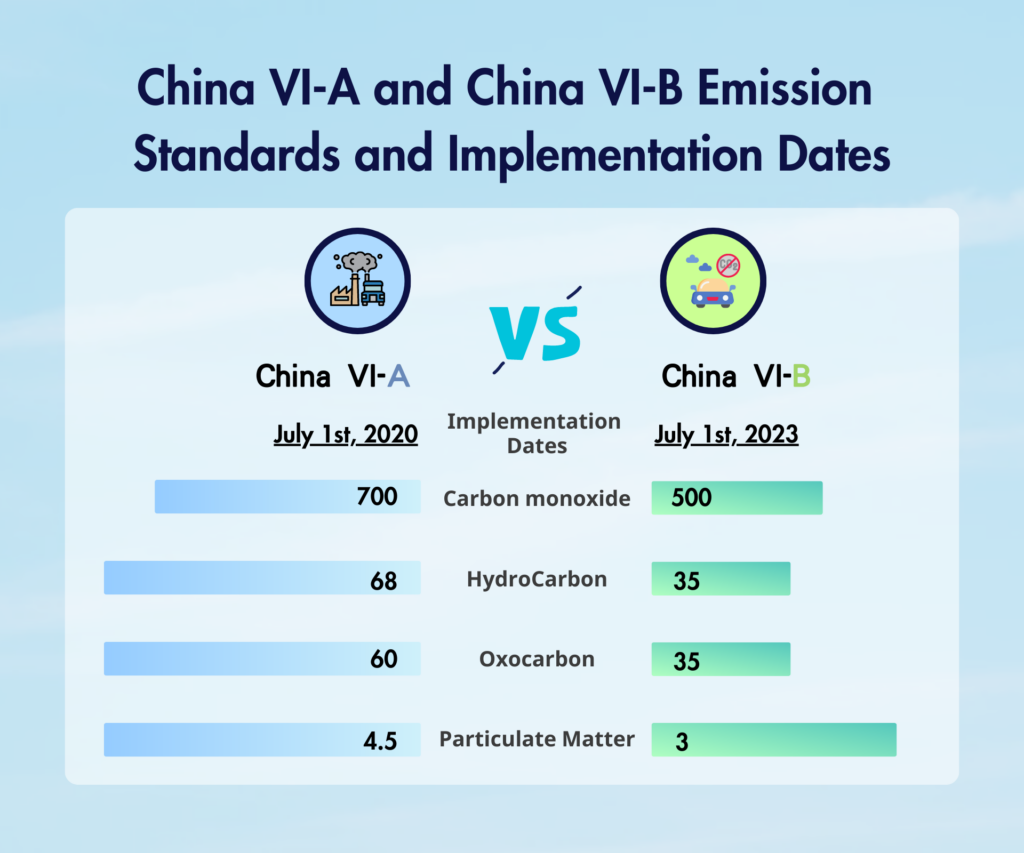

Another policy impacting sales is the China VI policy, which refers to the sixth stage of the national vehicle emission standards in China. It is implemented in two phases: China VIa and China VIb. China VIa was enforced in July 2020, while China VIb is scheduled to be implemented in July 2023. By then, vehicles that do not meet the China VIb emission standards will be prohibited from production, import, and sale. However, a transition period of six months is provided for the sale of certain light-duty vehicles due to dealerships still having substantial inventory, allowing sales until December 2023.

According to statistics from the China Passenger Car Association (CPCA), as of February 2023, there were over 2 million vehicles in inventory that had not undergone Real Drive Emission (RDE) testing for China VIb standards. To accelerate the reduction of inventory, the gas vehicle market initiated numerous price reduction and promotion activities in March 2023. As a result, by May 2023, the non-RDE China VIb compliant vehicles had reduced to less than 1 million units in inventory, showcasing the significant impact of these price reduction and promotion efforts.

However, for upstream automotive component manufacturers, the risk lies in the short-term focus of customers on destocking inventory, leading to a reduction in order placements.

Substantial subsidies has led to the rapid emergence of numerous new car companies, some of which are established solely to exploit these subsidies. Once the subsidies lose their impact, automakers that have never focused on the mass market will inevitably exit the competition. Additionally, when automakers become embroiled in a price-cutting competition, automotive component manufacturers may need to adjust their product prices in response. Given the numerous competitors in the component manufacturing sector, losing customers or experiencing revenue decline is around the corner.

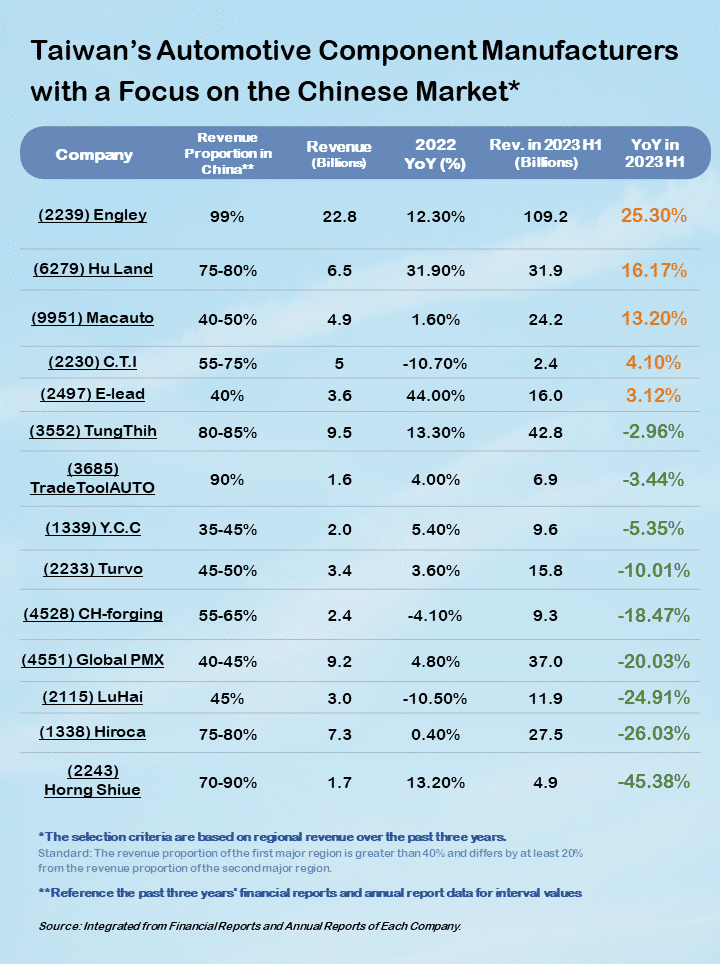

The revenue performance of Taiwanese automotive component manufacturers primarily targeting the Chinese market (a total of 14 companies) is as shown in the table below. In 2022, the majority of these manufacturers experienced revenue growth due to increased car sales driven by Chinese subsidy policies. However, in the first quarter of 2023, only a few of these manufacturers maintained a year-on-year growth trend, with most entering a phase of decline. The revenue disparities depend on whether these component manufacturers’ primary customers are Chinese leading, mid-tier Chinese manufacturers, or European and American car companies.

Firstly, leading Chinese automakers maintain a higher market share, ensuring consistent demand and a stable pull for components, thus minimizing concerns for component manufacturers. Secondly, mid-tier car manufacturers, if on the brink of elimination, might focus on capital recovery and stop placing orders. Even if there is no immediate risk of elimination, they might reduce orders to prevent inventory accumulation. Lastly, some European and American car manufacturers have been affected by local regulations and the increasing operational risks in China, leading to gradual production line shifts out of China. This negatively impacts component manufacturers due to the effect of shifting orders.

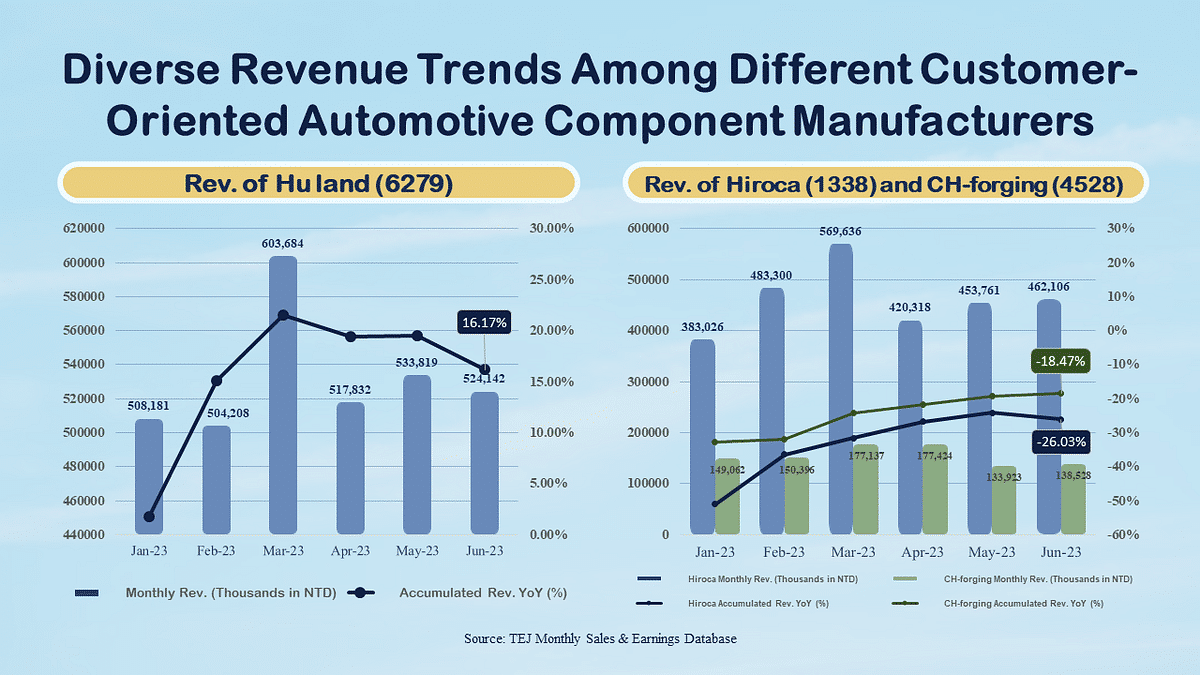

Taking Hu Lane (6279.TWO) as an example, its major customers include BYD, Changan Automobile, and Geely. In 2022, due to the surge in EV sales propelled by Chinese subsidy policies, the company’s shipments increased, resulting in a revenue growth of 32%. Furthermore, as customer car production continues to grow, the company’s Q1 2023 revenue displayed a growth of 21%. As of the first half of 2023, the accumulated revenue still exhibited a yearly growth of 16%.

If we consider Hiroca (1338.TW) and CH-forging (4528.TWO), their primary customers are Japanese joint-venture automakers. However, the impact of recent Chinese pandemic situations has led to shorter orders (spanning only one quarter) from Japanese clients. Consequently, their revenue performances have been lackluster since Q4 2022. In Q1 2023, revenue declined by 32% and 24% respectively, with the decline narrowing slightly to 26% and 18% in the first half of 2023.

In the past few years, Chinese automakers have sprung up like mushrooms, enjoying a thriving market driven by substantial demand. However, as the demand propelled by subsidies comes to an end, Chinese car companies are compelled to face challenges of elimination and consolidation. Lagging manufacturers will be acquired by larger players or possibly even pushed out of the competition entirely.

Nevertheless, recent commitments by Tesla and other Chinese automotive manufacturers to avoid malicious price competition bring a positive tone to the currently intense price wars. However, the impact of these commitments on sales still needs to be observed.

What’s even more critical is that for Taiwanese automotive component manufacturers, the downstream effects of car assemblers engaging in price wars could potentially lead to a cascading drop in component prices. These manufacturers might even face order reductions due to cost considerations. Overall, the development of the Chinese car market in 2023 remains uncertain.

It’s advisable to adopt a cautious stance towards future developments and remain attentive to the following three risks: (1) Decreased customer demand, (2) Customer market exit, and (3) Short-term concentrated destocking of inventory by customers.

Read More:

About us

⭐️ TEJ Website

⭐️ LinkedIn

✉️ E-mail: tej@tej.com.tw

☎️ Phone: 02–87681088