With the advancement of technology, the amount of data computers need to process has become increasingly massive. The transmission speed of computers in the past has become insufficient to meet the demands of next-generation high-speed computing. Therefore, when faster transmission interface specifications are introduced, high-speed transmission IC design companies must also increase their investment in developing related products. However, in recent years, high-speed transmission IC design companies have experienced declining revenues and profits. After a two-year inventory adjustment period, by the second half of 2023, most manufacturers’ inventories have returned to a healthier level. Additionally, with inflation gradually cooling down and the surge in AI demand, terminal demand is expected to gradually recover. This article will introduce you to the high-speed transmission IC design industry and provide insights into the latest trends in the IC industry.

Table of Contents

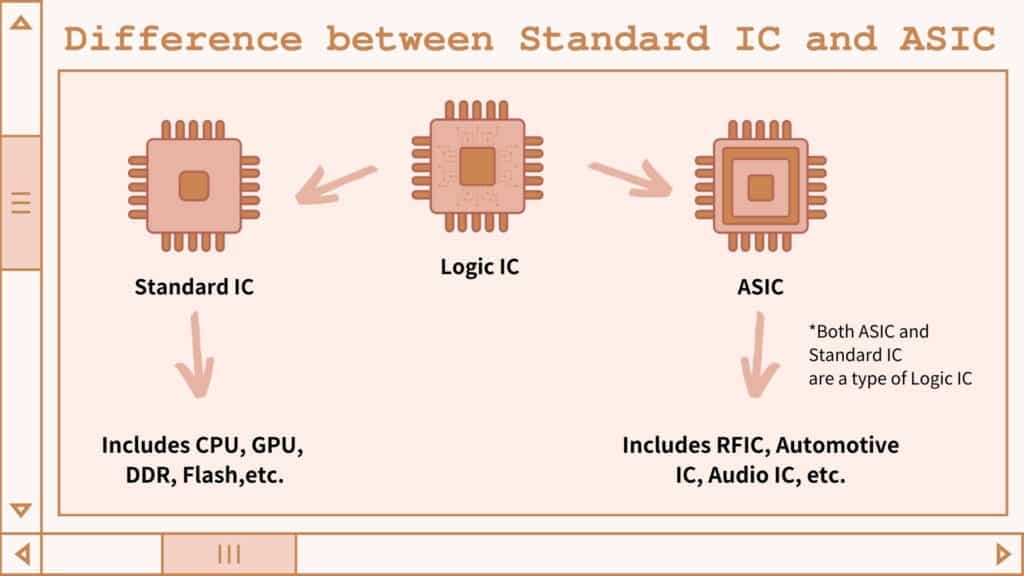

Before introducing high-speed transmission IC design, we must first understand Application-Specific Integrated Circuit (ASIC). ASIC is a custom-designed integrated circuit tailored to specific product requirements. ASIC chips are commonly used in various specialized domains such as automotive assistance systems, audio processing, weapon systems, and communication transmission. High-speed transmission IC design, which falls under the category of ASIC design, serves as a bridge for communication between CPUs, GPUs, and memory. With “Information Explosion” and the emergence of AI, the demand for data transmission has significantly increased. As a result, there are notable requirements for improving the specifications of high-speed transmission ICs, and the pace of iteration continues to accelerate.

High-speed transmission IC design companies, like other IC design firms, create circuit diagrams and then hand them over to downstream wafer foundries and packaging & testing facilities for manufacturing and packaging testing. The IC design companies themselves are not involved in the production process; therefore, they do not construct factories, resulting in lower capital expenditures and fewer fixed assets. Due to the lower required capital investment, they tend to retain a higher proportion of cash, which typically reduces liquidity concerns. Recent data shows that for other types of manufacturers, fixed assets account for more than 30% of total assets, with some even exceeding 50%, while cash represents only about 20% of total assets. In contrast, high-speed transmission IC design companies generally have fixed assets accounting for less than 10% of total assets, primarily consisting of offices and computer equipment, while cash makes up around 40% of their assets.

As mentioned above, this industry doesn’t rely on capital for profit; instead, it thrives on intellectual prowess and technical expertise. Consequently, research and development (R&D) expenses constitute a significant proportion. For high-speed transmission IC design companies, the recent transition in specifications has further elevated R&D investment. On average, these companies allocate approximately 20-30% of their revenue to R&D, where across the entire IC design industry, R&D spending typically falls within the range of 10-20% of revenue.

In the future, the widespread adoption of AI applications will lead to a shift in computing endpoints from the cloud to decentralized physical endpoints, a concept known as “Edge Computing”, requiring even greater data transfer capabilities. While CPUs and GPUs have become faster, memory technology has evolved to DDR5, and network speeds have upgraded to 5G, the data transfer rates between these electronic components remain insufficient. The same issue persists in data transmission between computers and external devices.

To address this challenge, the USB Implementers Forum (USB-IF) and the PCI-SIG organization introduced the USB 4.0 and PCIe 5.0 standards in 2019, while these high-speed transmission IC design companies are responsible for designing chips abided by these rules.

The most common type of transmission standards, mostly used for the connection between PC and external devices. Despite having a slower transmission speed compared to PCIe, USB are easier to swap and compatible to other devices, resulting in a higher versatility. Based on application, USB can be categorized as:

USB-IF released USB 4.0 v2 standards in November 2022. However, since it usually takes 1-2 years for manufacturers to develop a new product, and it generally takes another 1-2 years for the product to be verified and promoted, products now are mostly still based on USB 4.0.

PCIe is primarily used for internal connections and transmissions within computers and host systems, such as connecting CPUs, memory, and other devices. It offers the fastest speed, but due to its placement within the host system, it cannot be casually removed. In January 2022, the PCI-SIG announced the PCIe 6.0 specification. However, similar to USB, current vendor development still focuses on PCIe 5.0 products

During high-speed signal transmission, signal attenuation occurs, leading to a decline in signal integrity and quality. As the signal travels farther, the transmission speed also slows down. To mitigate this, repeaters are introduced to adjust the signal and prevent excessive attenuation. Repeaters can be further categorized into Retimers and Redrivers.

According to a Skyquest survey, the global transmission interface IC market had reached USD $9.871 billion in 2022. It is projected to exceed USD $17.041 billion by 2030, with a CAGR of 7.76%. However, the transmission interface IC market is still dominated by European and American IC design companies and IDM (Integrated Device Manufacturer) factories. These companies have large scales and broad product lines. They can bundle transmission interface ICs with other types of chips, offering competitive pricing and comprehensive product services. As a result, Taiwanese manufacturers account for less than 10% of the overall market size.

High-speed transmission IC design companies can be divided into three categories based on their operation,

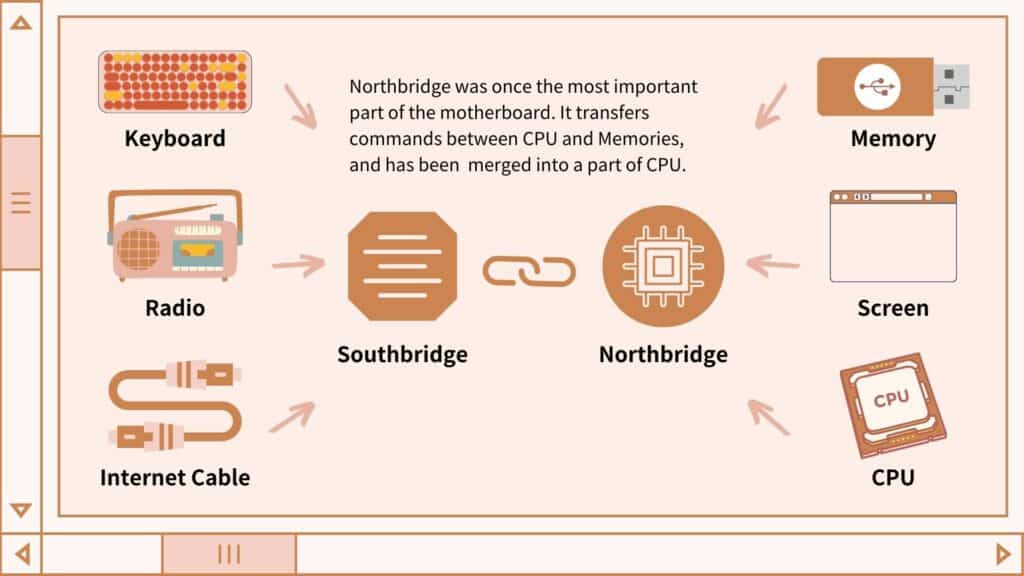

Initially, chipsets were divided into northbridge and southbridge. The northbridge chipset facilitated communication between the CPU and memory. However, over time, the northbridge’s functionality was integrated into the CPU itself. As a result, chipsets nowadays primarily consist of only southbridge components. Initially, most chipsets were produced by CPU manufacturers. However, in recent years, AMD shifted its focus to compete with Intel in the CPU market and invested resources in developing AI-related processors. Consequently, AMD entrusted the design of its mid-range and low-end chipsets to ASMedia (5269.TW); therefore, ASMedia’s chipsets are directly supplied to AMD. This revenue stream has contributed to ASMedia’s overall stable performance compared to other competitors.

Earlier we mentioned that USB host chips and repeaters are primarily installed internally in computers or hosts. USB hubs, on the other hand, are used to expand connection ports, while USB device chips control peripherals like flash drives. Consequently, the first two types of products are mainly supplied to motherboard manufacturers, while the latter two are primarily provided to peripheral accessory manufacturers. For the former group of manufacturers, since their chips are installed on the motherboard and connected to the CPU via the southbridge chipset, compatibility issues and certification concerns are common. Therefore, they maintain close relationships with customers and often have stable supply arrangements. In contrast, manufacturers of the latter group face higher product homogeneity and may engage in price competition due to the lack of differentiation. Generally, the operational performance of the former tends to be more stable than the latter. Additionally, companies that offer multiple product categories are less susceptible to the impact of competition in a single product area, resulting in more stable operations.

Taiwan has 9 companies setting foot in High-Speed Transmission IC Design with the following main products in the list:

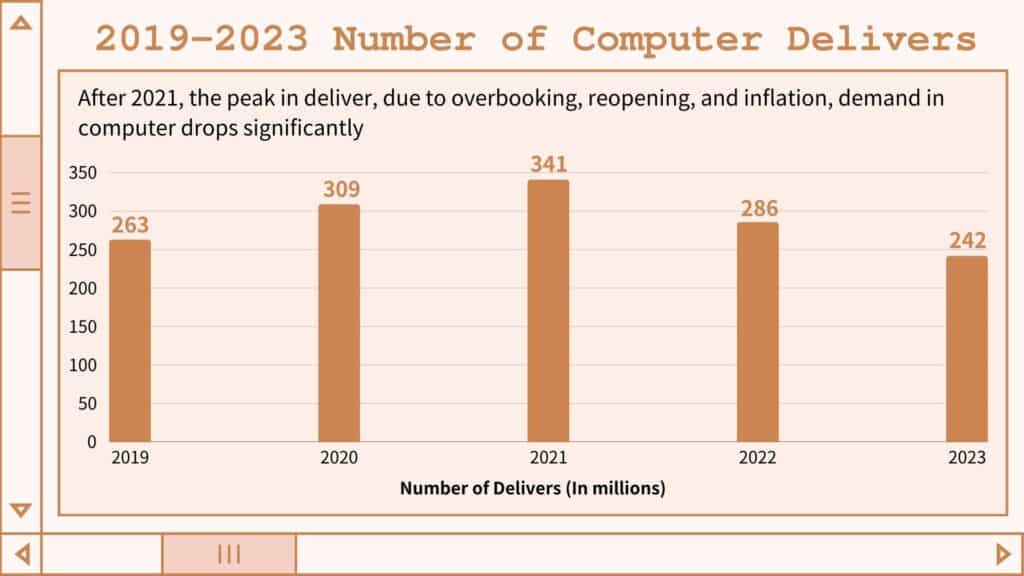

Due to the widespread use of high-speed transmission ICs in consumer electronics products such as laptops and desktop computers, the demand for end products significantly impacts the operational performance of upstream IC design companies. According to data from Gartner research firm, the fourth quarter of 2023 finally marked the end of eight consecutive quarters of declining shipments. Considering overall inventory levels and the official discontinuation of Microsoft Windows 8 updates in September 2023 (with Windows 10 also scheduled to end updates in 2025), there is a potential trend of consumers replacing laptops and computers in 2024, which may lead to a boost in product shipments.

In the year 2020, at the outbreak of the pandemic, issues such as labor shortages and material scarcity emerged. Additionally, transportation disruptions due to port congestion exacerbated the situation. Semiconductor foundries faced tightening production capacities, while the pandemic escalated, leading to a surge in demand for consumer electronics products like laptops. However, upstream IC design companies found themselves in a predicament of having full order books but insufficient inventory to fulfill them.

As a result, many companies increased wafer production, and some even signed long-term capacity supply agreements with semiconductor foundries to secure production capabilities. By 2021, inventory levels and days inventory outstanding (DIO) gradually rose. Moving into 2022, although the pandemic eased, macroeconomic challenges such as inflation and geopolitical tensions persisted. Declining end-demand further slowed down inventory reduction. Moreover, the previously signed long-term capacity agreements required prepayments or deposits and specified minimum wafer shipments, contributing to elevated inventory levels and days inventory outstanding in 2022.

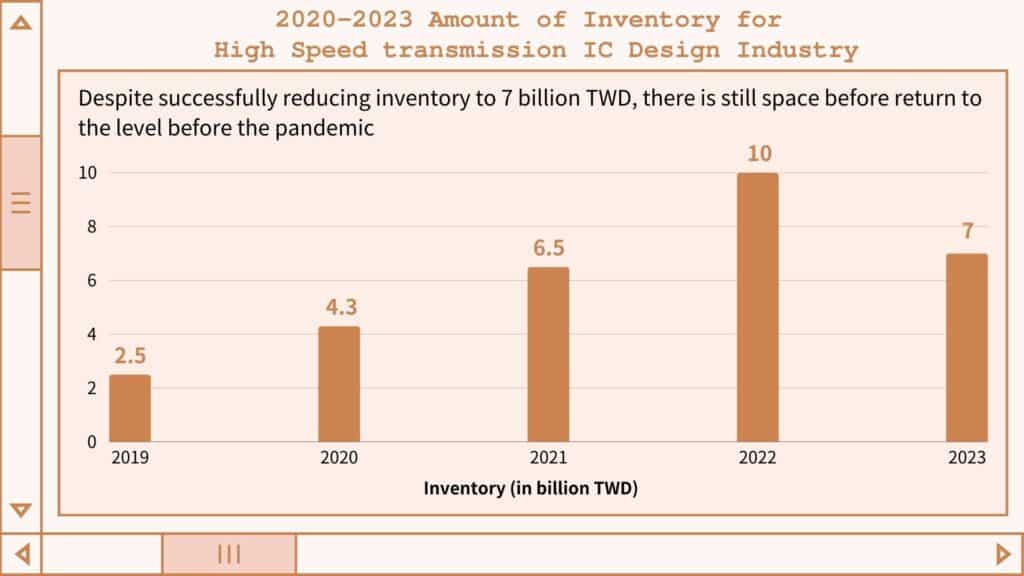

In the latter half of 2023, as end-product manufacturers gradually depleted their inventories, high-speed transmission IC design companies implemented inventory management measures. Inventory levels decreased from $10 billion at the end of 2022 to $7.5 billion in September 2023, and days sales outstanding (DSO) reduced from 179 to 156. With inventory control in place, the previously tied-up capital in inventory was released, leading to improved cash flow for most companies. It is speculated that the pressure on working capital eased during this period.

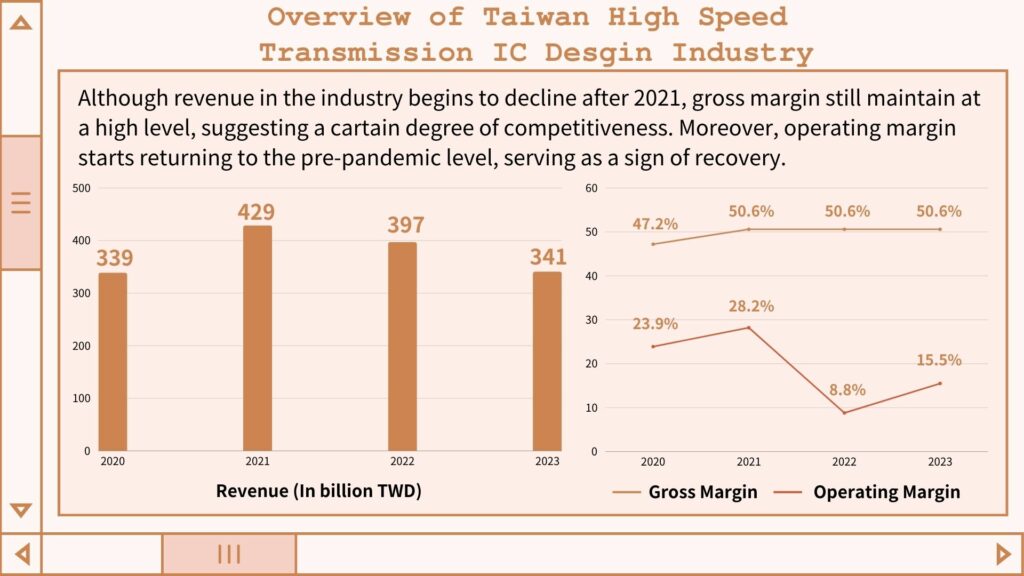

In 2020 and 2021, despite benefiting from the increasing demand caused by the ‘stay-at-home’ economy, subsequent factors such as reopening and the ‘bullwhip effect’ caused by excessive ordering gradually emerged. As a result, overall revenue declined continuously after reaching its peak in 2021—a necessary path toward inventory reduction. However, gross profit margins remained relatively stable, hovering around 50%, and profitability rates showed signs of bottoming out in the second half of 2023.

As end-demand gradually rebounds, operational performance is expected to stabilize. Additionally, the gradual ramp-up of USB 4.0 and PCIe 5.0-related products in 2024, coupled with the industry’s lower base in the current year, should contribute to a gradual recovery trend. The extent of profit performance due to specification transitions will depend on the pace of economic recovery. If overall economic conditions do not fully improve, consumers may be less willing to replace existing products, decelerating the recovery of companies’ revenues.

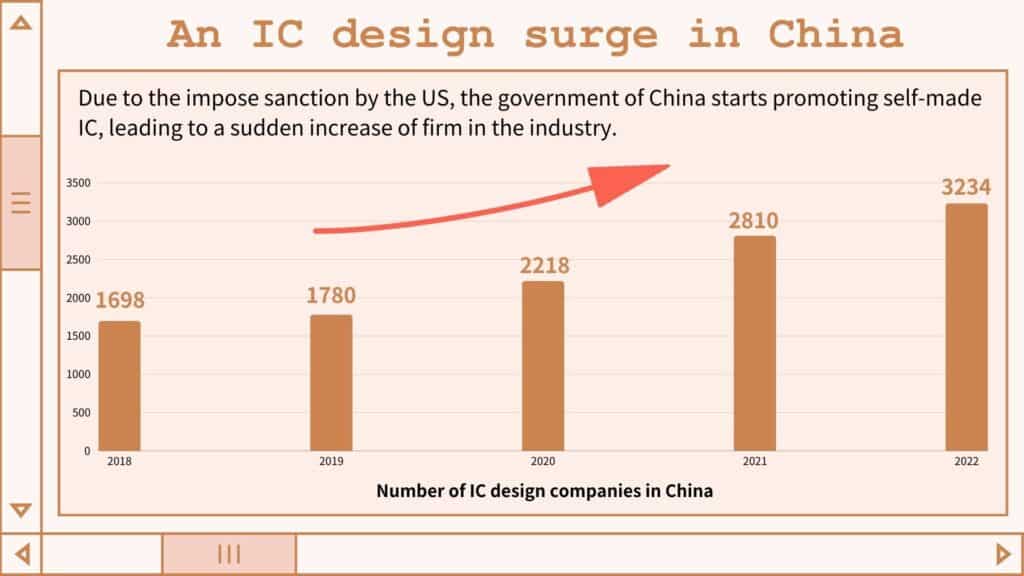

Due to the lack of difference in products between USB hub-side and device-side manufacturers, the competition in the industry has become increasingly fierce. In recent years, the United States has consistently targeted China’s semiconductor industry, prompting China to enhance its entire semiconductor supply chain to achieve self-sufficiency and reduce reliance on the U.S. market.

While the U.S. semiconductor restrictions primarily focus on advanced processes, the control over IC design mainly targets high-performance chips, including those related to AI computation. Notably, high-speed transmission-related chips are not within the scope of U.S. restrictions. Additionally, Chinese manufacturers have a history of excelling in cost reduction and adopting low-price competition strategies.

If the Chinese government redirects funds originally intended for high-performance chips toward other product categories, it could pose a threat to USB hub-side and device-side manufacturers with relatively small competitive differentiation. Despite a recent downturn in market demand, some Chinese IC design companies established for subsidy purposes have faced closures. Consequently, existing Chinese IC design companies are adopting more conservative strategies, focusing on existing product lines rather than pursuing cutting-edge processes. As a result, this shift may intensify competition in the high-speed transmission IC design industry.

Looking ahead to 2024, despite ongoing unfavorable macroeconomic factors and incomplete recovery in end-demand, but since

The outlook suggests a gradual recovery, and the high-speed transmission IC design sector should continue to adapt and grow in 2024.

TEJ datasets specifically provides the information required for basic analysis of the securities financial market, quickly solve your data needs, and efficiently help your decision-making.

Check what TEJ dataset provide