Table of Contents

Hota (1536.TW), formerly known as Hehsing Industrial Co., was founded in March 1966 by Fu-Chu Tseng, who started as an apprentice in the industry. It wasn’t until January 1973 that the company was reorganized as Hota Industrial Manufacturing Co., Ltd.; in December 1975, it was renamed Hota Industrial Development Co., Ltd. At that time, the motorcycle industry was flourishing, which allowed Hota, engaged in the production of automotive components, to operate smoothly. Consequently, the company lacked the necessary sense of crisis.

In 1985, Bajaj, a motorcycle industry player, exported goods to China but was unable to recover the payment. The company’s owner also engaged in the unauthorized sale of company assets for personal gain. As a result, the checks issued by Bajaj to Hota bounced, leading to a bad debt of NT$105 million. Over the next five years, Hota, though not collapsing, found itself in financial turmoil. It wasn’t until 1990, under the recommendation of creditor banks, that Guo-Rong Shen took over as the chairman. The company underwent a comprehensive restructuring and was renamed Hota Industrial Co., Ltd.

Following its successful restructuring, Hota firmly established itself in the market. In March 2000, the company was listed on the OTC market, and by September 2001, it transitioned to become a publicly traded company. With Guo-Rong Shen as the ultimate controller, the Hota Group took shape.

Over the past two decades, how did the Hota Group grow and expand its conglomerate? What motivated its strategic decisions to invest in companies such as Kafo, Duro, and Mediera? In this article, we will provide an overview of each member’s operations within the Hota Group and explain the timing and methods of the Hota Group’s acquisitions, offering you a deeper insight into the development history of the Hota Group.

Kafo (4510), formerly known as Kafo Iron, was founded by its founder, Chun-Ding Chuang, in May 1968. In 1972, it was reorganized as Kafo Machinery Co., Ltd.; in February 1979, it became Kafo Machinery Industrial Co., Ltd. In October 1991, the company went public with its stock offerings. At that time, Kafo was a standalone company and had yet to form a group.

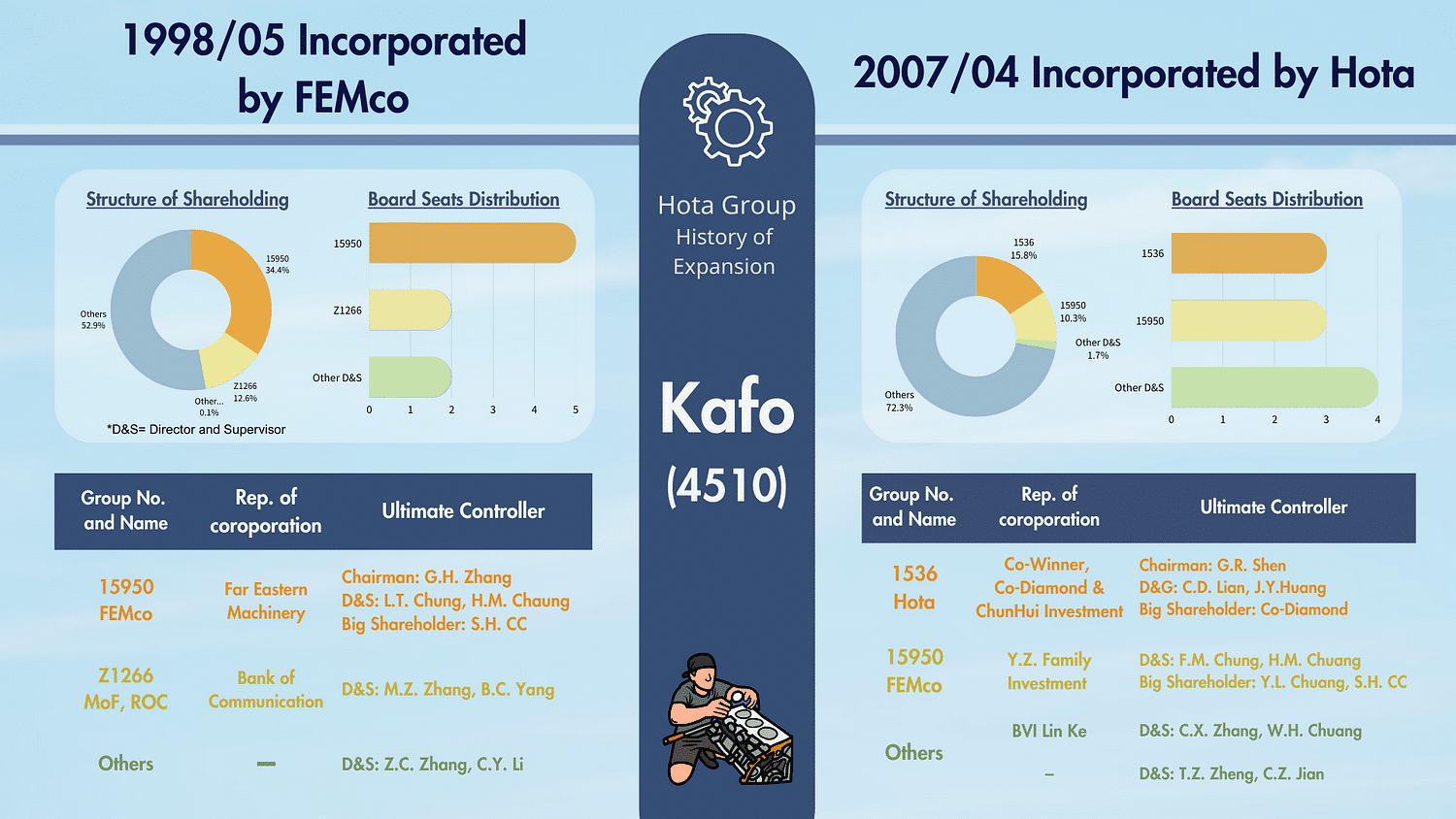

In 1992, Chun-Ding Chuang expressed his intention to relinquish the management rights of Kafo. Kafo, in a strategic alliance, entered into a stock-swap agreement with the Chuang family of the Far Eastern Machinery Group. In October of the same year, an extraordinary shareholders’ meeting was held for the election of directors and supervisors. Chun-Ding Chuang stepped down as the chairman of Kafo, handing over the position to Guo-Qin Chuang of the Far Eastern Machinery Group. Other family members from the Far Eastern Machinery Group also joined the board of directors. Concurrently, Kafo changed its name to Kafo Industrial Co., Ltd. In February 1998, it was officially listed on the OTC market. In May 1998, out of a total of 9 directors and supervisors, individuals associated with the Far Eastern Machinery Group secured 4 director seats and 1 supervisor seat, holding a 34.35% share. Kafo became a part of the Far Eastern Machinery Group from then onwards.

In 2005, Kafo faced the impact of macroeconomic regulation in mainland China, with its operating profit plummeting from NT$59,005 million in 2004 to a loss of NT$-58,225 million in 2005, transitioning from profit to deficit. Concurrently, the domestic machinery industry was undergoing a resource integration movement involving several major players such as Hota, Yawei, Chengtai, and Chunxin De. They planned to jointly establish the “Automotive Component Manufacturing Machinery Association” to capture a significant global market share. In response, Kafo held an extraordinary shareholders’ meeting in January 2006 to elect two vacant director positions, allowing Hota Group to enter the board of directors.

By May 2006, Far Eastern Machinery Group gradually withdrew from the Kafo management. Chairman Guo-Hui Chuang stepped down from his dual role as general manager. In January 2007, he resigned as chairman, citing busy business commitments, and was succeeded by Guo-Rong Shen from the Hota Group.

In January 2007, the management of Kafo underwent a change, with Hota Group taking over, thereby becoming a part of Hota Group. By April 2007, Kafo had a total of 10 directors and supervisors. Through Co-Winner Investment, Co-Diamond Investment, ChunHui Investment, and Guo-Rong Shen, Hota Group collectively held a 15.78% share in the company and held three director positions, including the chairman’s position. This gave Hota Group both significant ownership and control over the board seats.