Table of Contents

In 1990, as law enforcement agencies began cracking down on underground investment companies, the Hong Yuan Company collapsed due to multiple runs, leaving over 90 billion NT dollars of unpaid debt and 160,000 investors with nothing but losses. Over 33 years later, in early 2023, the “Real Estate Lending and Matchmaking Platform, im.B” defrauded over 5,000 people of more than 2.5 billion through a “false debt, real fundraising” scheme. Whether in the past or the present, financial fraud has never stopped, and there is always a large number of investors who fall for the lure of high-interest rates and end up losing all their assets.

With the rise of fintech in recent years and the convenience brought by P2P lending, it has become essential for us to identify Ponzi schemes. However, judging a crisis has never been a simple task. In this article, we will explore what constitutes financial fraud through the recent im.B case and analyze how to identify potentially risky enterprises based on group structures and other aspects, helping you overcome information asymmetry and make the most accurate judgments.

im.B was established in 2015 by “Taiwan Jinlong Technology Co., Ltd.” It’s an online real estate lending platform, focusing on financial technology and various loan matchmaking services. It attracted investors with promises of legal operations, stable and high returns (9~12%), and diversified risk. In fact, im.B provided second-mortgage lending (where properties with existing loans apply for a second loan from another bank) matchmaking services, commonly known as “P2P lending.” Its main function was to connect investors with borrowers seeking second-mortgage loans. Once investors deposited funds, im.B would pay monthly interest based on the debt investments they subscribed to.

Initially, interest payments were stable, but starting from December 2022, they stopped. In subsequent platform briefings, internal executives confessed that 95% of the debt investments did not actually exist. They were fabricated by the platform by repeatedly listing non-existent debt investments. In other words, there were no borrowers seeking second-mortgage loans at any point. When investors transferred money into the original debtors’ accounts, it would be directly transferred to im.B’s account to pay interest to other investors. Thus, the platform continually patched its funding gap through a “robbing Peter to pay Paul” scheme.

Afterward, the investigative authorities arrested several individuals responsible for the platform, including Tseng Yao-Feng, Tseng’s father Tseng Ming-Hsiang, Tseng’s girlfriend Zhang Shu-Fen, financial director Pan Chih-Liang, as well as Zhang Sheng-Er and Gao Ying-Yuan. Following the investigation, 39 victims initially filed reports with the police, with financial losses totaling 150 million NTD. However, the self-help group of victims comprised over 5,000 members, and the total amount of losses reached 2.5 billion NTD.

In the past, one of the most well-known financial fraud cases was the “Hong Yuan Institution.” Hong Yuan advertised monthly interest rates of 4% to 6%, attracting a massive influx of 100 billion NTD. However, after the amendment of the Banking Act in 1989, law enforcement agencies began cracking down on underground investment companies, leading to multiple runs on Hong Yuan. The company ended up collapsing, leaving over 90 billion NTD of unpaid debt and 160,000 investors with significant losses. The modus operandi of Hong Yuan was a classic Ponzi scheme, wherein it established shell companies and offered unrealistic returns to lure investors. Initially, it managed to pay interest to investors by using new investments to repay old ones. However, once a run or liquidity issue occurred, the scheme unraveled, and investors had to wake up from their wealth dreams.

Over 30 years since the Hong Yuan case, illegal Ponzi schemes have continued to evolve, especially with the widespread adoption of fintech. The accessibility of peer-to-peer lending platforms has lowered the threshold for public borrowing and investment, providing fraud groups with more opportunities for packaging their Ponzi schemes. In modern times, real estate, forex margin, bonds, and even the currently popular cryptocurrencies can serve as enticing elements for Ponzi schemes, increasing the likelihood of investors falling into such traps.

The P2P lending involved in this case is a decentralized lending method that directly matches borrowers and funders. In fact, P2P lending defaults have been numerous in recent years, especially in China, with companies like NEO Capital implicated in the illegal fundraising of 102.6 billion Chinese yuan. In Taiwan, P2P lending is still in its early stages of development and is subject to less regulatory oversight from financial regulatory authorities. In the worst-case scenario, some high-interest P2P investments may turn out to be mere shell companies, where the invested money does not go towards lending but ends up in the pockets of the responsible individuals. In such cases, the im.B incident and the Hong Yuan case share the same DNA, merely wrapped in the guise of P2P lending.

The term “shell company,” refers to a company lacking substantive business operations, which may be used to evade legal responsibilities, engage in fraud, or money laundering activities. However, not all shell companies are established for fraudulent purposes; as long as they comply with legal and regulatory requirements, shell companies can exist legitimately in many cases. The challenge lies in identifying whether a shell company under a group is involved in fraudulent or money laundering activities. What are the clues to look for?

The key to this question lies in understanding the ownership structure of the group and its subsidiary members, and then examining financial statements, actual business operations, and related-party transactions of the subsidiary companies. However, in the case of Taiwan Jinlong Technology Co., Ltd. and its affiliated group, ChuanCheng Property Group, all companies are non-public companies, and their financial statements are not publicly available. This lack of information hinders investors from analyzing their operational stability. Nevertheless, insights can still be gleaned from TEJ GCRI.

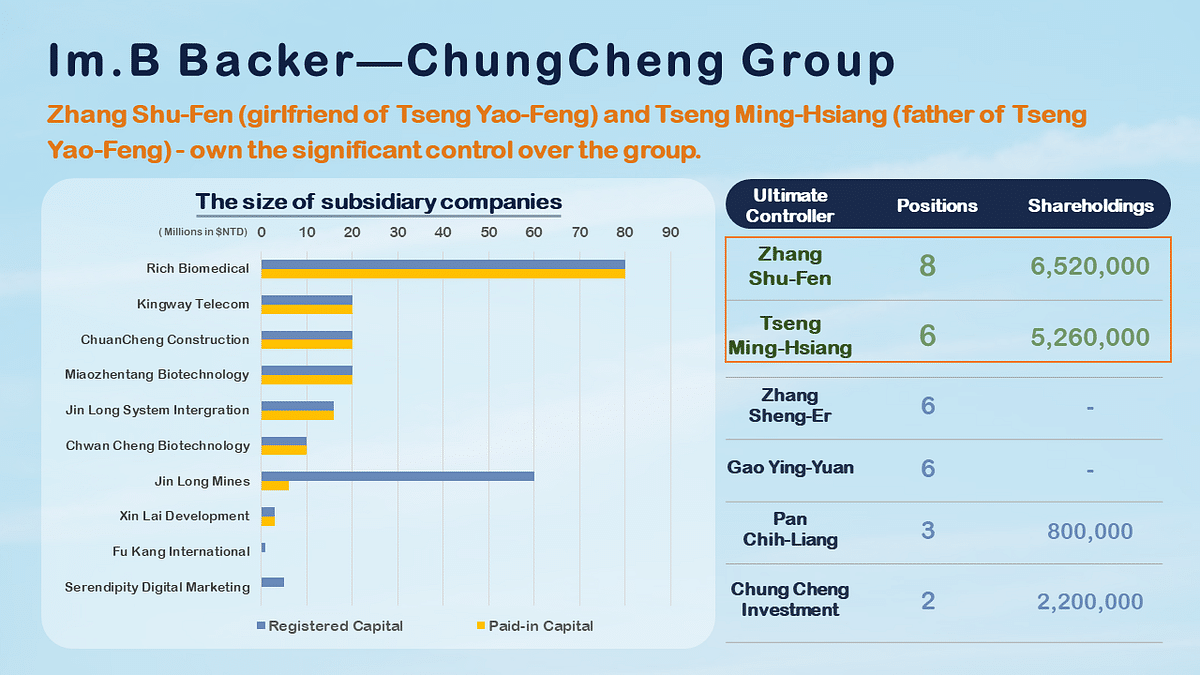

TEJ GCRI has compiled the most comprehensive information on corporate groups, covering publicly listed companies and small and medium-sized enterprises. This data provides a clear view of the corporate structure and ultimate controllers. Taking im.B as an example, im.B’s main financial backer, Taiwan Jinlong Technology, is affiliated with ChuanCheng Property Group, which includes ten member companies such as Rich Biomedical, Kingway Telecom, and ChuanCheng Construction. Among the company heads of the group members, seven are affiliated with Zhang Shu-Fen, two with Tseng Ming-Hsiang, and one with Pan Chih-Liang. Regarding control rights, Zhang Shu-Fen holds eight positions in the board of directors and supervisors, Tseng Ming-Hsiang, Zhang Sheng-Er, and Gao Ying-Yuan each hold six positions, while Pan Chih-Liang holds three positions. All the individuals mentioned above have been listed in the name list of those detained by the investigative authorities, indicating that the companies under ChuanCheng Group are likely involved in illegal fundraising cases. The summarized information of the group is shown in the figure below:

From the above figure, it can be observed that Zhang Shu-Fen and Tseng Ming-Hsiang, who were detained in this case, hold shares and board positions in multiple companies under the group, indicating their significant control over the group. This also suggests their direct involvement in the illegal fundraising case. Further, many of companies share the same registered address, increasing the possibility that some of them may be shell companies. However, this point would need verification through on-site visits. Armed with this information, you can also scrutinize the companies through their physical business presence, recruitment information, official websites, and other channels to check for any lack of specific information or conflicting data. By doing so, the issues arising from information asymmetry can be improved.

In summary, there often exists an information asymmetry in financial matters. In the past, financial institutions could rely on databases that recorded customer credit ratings, account information, and other data to assess whether to grant loans. However, with the advent of financial technology, information asymmetry becomes more evident, potentially leading to the emergence of fraudulent borrowing entities, resulting in unrecoverable loans. Investors should exercise caution and conduct research on the borrowing entities before making decisions. In this case, one can observe the related parties’ information within the group by examining group data, including the responsible persons, directors, supervisors, or shareholders. Further online searches can be conducted to find additional information to avoid falling into financial fraud traps.

In addition, when fintech brings greater convenience to us, the question remains whether “technology starts from human nature.” Whether viewing P2P lending platforms as innovations or changes, the P2P industry in Taiwan is still relatively early-stage. It may face challenges in the future that could be more severe than this current incident. Learning from precedents in other countries and being vigilant are important aspects. However, not all P2P lending platforms are Ponzi schemes. they can still have positive effects and significant importance.

Most importantly, when we see slogans like “guaranteed profits” and “low-risk, high-return,” we must thoroughly consider their reasonableness. Why can such high-interest rates be offered? What are the underlying investment targets? By gathering more information and considering various aspects, we can avoid falling into the fraud, risking the hard-earned savings we have diligently accumulated!

Read More

Want to know more?

TEJ TAIWAN DB → TESG Sustainability Solution→ TESG Sustainable Dataset

Accessing TESG Sustainable Dataset, you can obtain information on companies’ ESG practices!

If you have any questions about this article or want to obtain further access to the TEJ database, please feel free to leave a comment, call, or mail us.

About us

⭐️ TEJ Website

⭐️ LinkedIn

✉️ E-mail: tej@tej.com.tw

☎️ Phone: 02–87681088