To construct a portfolio based on Jim Slater’s principle

Table of Contents

Jim Slater is one of the well-known U.K. investors. He used to write column articles of portfolio recommendation for Sunday Telegraph and was famous for earning around 68.9% return during the period between 1963 to 1965, while the U.K. stock market only grew at 3.6% at the same period. Jim Slater’s ‘Zulu Principle’ stresses the importance of focusing on your own niche field, where you can take advantage of. Therefore, Jim Slater especially pays attention to small and medium size firms that have long-term profit growth and relative strength and adopts price/earnings to growth ratio (PEG ratio) as an important standard for valuation, as the following shown:

We use Windows OS and Jupyter Notebook in this article

import pandas as pd

import numpy as np

import tejapi

import matplotlib.pyplot as plt

tejapi.ApiConfig.api_key = "Your Key"

tejapi.ApiConfig.ignoretz = True

Since Jim Slater’s stock-picking standards include some subjective judgement factors, we present the following objective and quantitative indicators based on them and also adjust them by considering Taiwan stock market environments

Condition1: Firm market value < Market average market value

Condition2: Positive net incomes in the past five years

Condition3: Net income growth > 15% in three consecutive years

Condition4: Expected net income growth ≥ 15%

Condition5: 5-year average cash flow from operating > 5-year average net income

Condition6: Recent cash flow from operating > recent net income

Condition7: Recent operating margin ≥ 10%

Condition8: Recent return on capital employed ≥ 10%

Condition9: Recent debt/equity ratio < 50%

Condition10: Recent shareholding ratio of directors and supervisors ≥ 20% or recent increase in this ratio

Condition11: Expected PE ratio ≤ 20

Condition12: Expected PE ratio/Expected net income growth ≤ 1.2

Condition13: Monthly excess return > 0

Step 1. Obtain the codes of TSE listed common stocks

security = tejapi.get('TWN/ANPRCSTD',

paginate = True)

stock_list = security[(security['mkt'] == 'TSE') & (security['stype'] == 'STOCK')]['coid'].tolist()

Step 2. Obtain all the data we need and create condition column

#container for outputs

data = pd.DataFrame()

for coid in stock_list:

#Obtain financial data

finance = tejapi.get('TWN/AIM1A',

coid = coid,

mdate = {'gte':'2000-01-01'},

opts = {'pivot':True, 'columns':['coid','mdate','MV','R531','R405','7210','R106','2402','0010','1100','R504']},

paginate = True,)

#Select data in December to annualize the data

finance = finance[finance['mdate'].dt.month == 12].reset_index(drop=True)

#Add 'match year' column for the later combination purpose

finance['MatchYear'] = finance['mdate'].dt.year

#Calculate expected net income growth by using 5-year moving average of net income growth

finance['ExpectedNetIncomeGrowth'] = finance['R531'].rolling(5).mean()

#Calculate 5-year moving average of cash flow from operating activities

finance['5_YearAverageOperatingCashFlow'] = finance['7210'].rolling(5).mean()

#Calculate 5-year moving average of net income

finance['5_YearAverageNetIncome'] = finance['R531'].rolling(5).mean()

#Condition2: Positive net incomes in the past five years

finance['positive_profit'] = np.where(finance['R531'] > 0, 1, 0)

finance['condition2'] = np.where(finance['positive_profit'].rolling(5).sum() == 5, 1, 0)

#Condition3: Net income growth > 15% in three consecutive years

finance['net_income_growth_higher_than_15'] = np.where(finance['R405'] >= 15, 1, 0)

finance['condition3'] = np.where(finance['net_income_growth_higher_than_15'].rolling(3).sum() == 3, 1, 0)

#Condition4: Expected net income growth ≥ 15%

finance['condition4'] = np.where(finance['ExpectedNetIncomeGrowth'] >= 15, 1, 0)

#Condition5: 5-year average cash flow from operating > 5-year average net income

finance['condition5'] = np.where(finance['5_YearAverageOperatingCashFlow'] > finance['5_YearAverageNetIncome'], 1, 0)

#Condition6: Recent cash flow from operating > recent net income

finance['condition6'] = np.where(finance['7210'] > finance['R531'], 1, 0)

#Condition7: Recent operating margin ≥ 10%

finance['condition7'] = np.where(finance['R106'] >= 10, 1, 0)

#Condition8: Recent return on capital employed ≥ 10%

finance['ROCE'] = (finance['2402']/(finance['0010']-finance['1100']))*100

finance['condition8'] = np.where(finance['ROCE'] >= 10, 1, 0)

#Condition9: Recent debt/equity ratio < 50%

finance['condition9'] = np.where(finance['R504'] < 50, 1, 0)

#Remove NaN data

finance = finance.dropna().reset_index(drop=True)

#Obtain shareholding ratio data

chip = tejapi.get('TWN/ABSTN1',

coid = coid,

mdate = {'gte':'2000-01-01'},

opts = {'columns':['coid','mdate','fld005']},

paginate = True)

#Check if the latest shareholding ratio of insider increases

chip['if_shareholding_ratio_increase'] = np.where(chip['fld005'] > chip['fld005'].shift(1),1,0)

#Select February data, since the latest shareholding data we have at portfolio formation data is February data

chip = chip[(chip['mdate'].dt.month == 2)].reset_index(drop=True)

#Condition10: Recent shareholding ratio of directors and supervisors ≥ 20% or recent increase in this ratio

chip['condition10'] = np.where((chip['fld005'] >= 20) | (chip['if_shareholding_ratio_increase'] == 1),1,0)

#Add 'match year' column for the later combination purpose, the reason of 'minus 1' is because this ratio data matches last year's financial data

chip['MatchYear'] = chip['mdate'].dt.year - 1

#Creat a temporary dataframe by merging finance data with ratio data on firm's code and matchyear

temp = finance.merge(chip, on = ['coid','MatchYear'])

#Store this temporary dataframe in data

data = data.append(temp).reset_index(drop = True)Each loop deals with each stock. Because of the huge amount of data obtained, it takes around 30 ~ 40 minutes. The procedure includes data frequency adjustment, using np.where() to create condition columns, combining data from different databases and storing the outputs in data. Besides, since the index might be disordered after selecting, adding, sorting or removing data, we usually add reset_index(drop=True). The following is the final content of data:

data_cp = data.copy()

To avoid modifying the raw data, we copy data and proceed it with data_cp

#Calculate market average market value

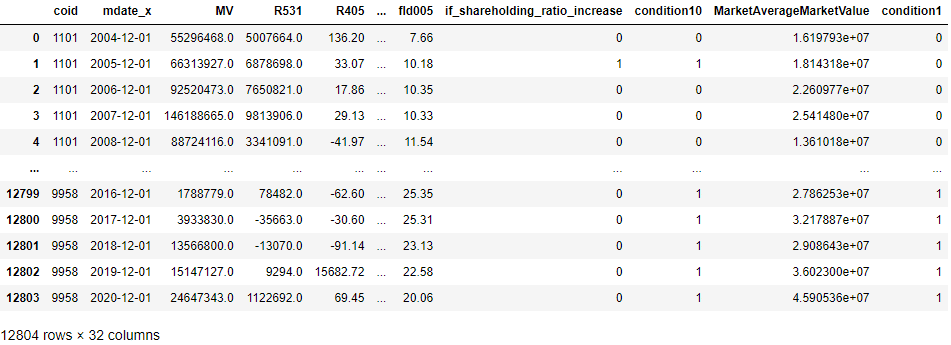

avg_mv = data_cp.groupby(by = 'mdate_x')['MV'].mean()#Map market average market value to data_cp by date column

data_cp['MarketAverageMarketValue'] = data_cp['mdate_x'].map(avg_mv)#Condition1: Firm market value < Market average market value

data_cp['condition1'] = np.where(data_cp['MV'] < data_cp['MarketAverageMarketValue'], 1, 0)

Once we have the market value of whole firms, we can now create condition1 column. Here we use map() to map market average market value to data_cp by its date column.

#We choose the columns we need

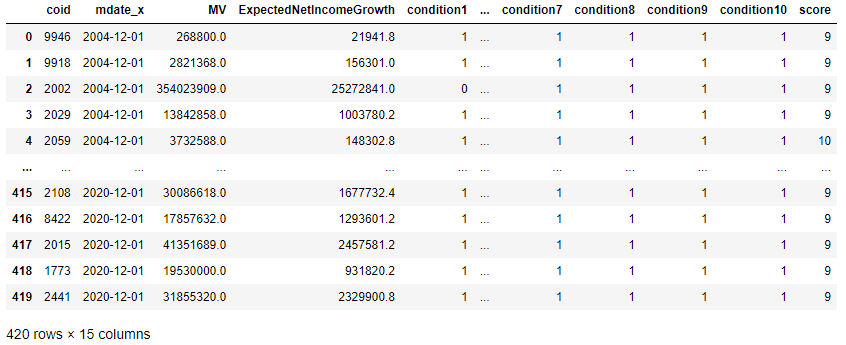

data_cp = data_cp[['coid','mdate_x','MV','ExpectedNetIncomeGrowth','condition1','condition2','condition3','condition4','condition5','condition6','condition7','condition8','condition9','condition10']]

#Calculate the score and select those higher than 9

data_cp['score'] = data_cp['condition1'] + data_cp['condition2'] + data_cp['condition3'] + data_cp['condition4'] + data_cp['condition5'] + data_cp['condition6'] + data_cp['condition7'] + data_cp['condition8'] + data_cp['condition9'] + data_cp['condition10']

data_cp = data_cp[data_cp['score'] >= 9].sort_values(by = 'mdate_x').reset_index(drop=True)

Step 3. Market-side condition and portfolio return calculation

Panel = pd.DataFrame() #To store complete data for each stock

Return = pd.DataFrame() #To store portfolio return

date_list = pd.DatetimeIndex(data_cp['mdate_x'].unique()) #Transform unique date into DatatimeIndex list

for date in date_list:

#Each year has a dataframe

table = data_cp[data_cp['mdate_x'].dt.year == date.year].reset_index(drop=True)

#Get the previous year's PE ratios at portfolio formation date

stocks = table['coid'].tolist()

pe_ratio = tejapi.get('TWN/APRCD1',

coid = stocks,

opts = {'columns':['coid','mdate','per_tse']},

mdate = {'gte': date + pd.Timedelta(days = 120 - 365) , 'lte': date + pd.Timedelta(days = 120)},

paginate = True)

#Calculate one-year average PE ratio as expected PE ratio

pe_estimate = pe_ratio.groupby(by = 'coid').mean().reset_index()

#Obtain the excess monthly return data

relative_performance = tejapi.get('TWN/APRCD2',

coid = stocks,

opts = {'columns':['coid','mdate','rois_m']},

mdate = {'gte': date + pd.Timedelta(days = 120 - 5), 'lte': date + pd.Timedelta(days = 120)}, #We just need the data closest to portfolio date

paginate = True)

#Pick the last data for each stock

relative = relative_performance.groupby(by = 'coid').last().reset_index()

#Combine expected PE with stock relative performance

merge = pe_estimate.merge(relative, on = 'coid')

#Alter column name to combine with table

merge = merge.rename(columns = {'mdate':'mdate_x', 'per_tse':'ExpectedPE_ratio'})

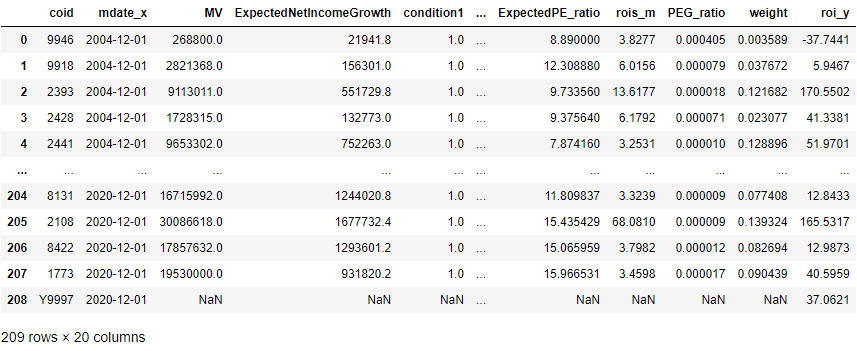

merge = table.merge(merge[['coid', 'ExpectedPE_ratio','rois_m']], on = 'coid')

#Calculate PEG ratio

merge['PEG_ratio'] = merge['ExpectedPE_ratio']/merge['ExpectedNetIncomeGrowth']

#Filter by market-side conditions, get the final constituent stocks

final = merge[(merge['ExpectedPE_ratio'] <= 20)&(merge['PEG_ratio'] <= 1.2) & (merge['rois_m'] > 0)].reset_index(drop=True)

#Calculate the weight by firm's market value

final['weight'] = final['MV']/ final['MV'].sum()

#Obtain return data (including market as benchmark)

stocks = final['coid'].tolist()

ret = tejapi.get('TWN/APRCD2',

coid = stocks + ['Y9997'],

paginate = True,

opts = {'columns':['coid','mdate','roi_y']},

mdate = {'gte': date + pd.Timedelta(days = 120), 'lte': date + pd.Timedelta(days = 120+365)})

#Period Return: get the last return data of each stock, which is yearly return

period_ret = ret.groupby(by = 'coid')['roi_y'].last().reset_index()

#Assign date for later combination

period_ret['mdate_x'] = date

#Combine it with final, outer can make sure market return data is not removed

temp = final.merge(period_ret,on = ['coid','mdate_x'], how = 'outer')

#Store this year's complete data

Panel = Panel.append(temp).reset_index(drop=True)

#Hold the portfolio since 2005(built on 2004 data), 2020 year is excluded because its portfolio hasn't been held for a year

if 2020 > date.year >= 2004:

#Calculate portfolio return and market return

fee = 0.1425*2 + 0.3

eq_port = temp.loc[:,'roi_y'].values[:-1].mean() - fee #Equally-weighted portfolio return (excluding market return)

val_port = (temp['weight']*temp['roi_y']).dropna().sum() - fee #Market-Cap-weighted portfolio return (excluding market return)

mkt = temp['roi_y'].values[-1] #Market return

#Store whole return

Return = Return.append(pd.DataFrame(np.array([date,eq_port,val_port,mkt]).reshape((1,4)),columns = ['mdate_x','Equally-Weighted Portfolio Return','Market-Cap-Weighted Portfolio Return','Market Return'])).reset_index(drop=True)Here we use each year as one loop and make the second filtering by market-side conditions and calculate portfolio return. It’s worth noting that the time window of PE ratio we obtain is the previous year at portfolio formation date. For example, if mdate_x is ‘2020–12–01’, it means we’ll construct the portfolio on ‘2021–03–31’(120 days later) and we need PE ratio from ‘2020–03–31’ to ‘2021–03–31’). Since this portfolio will be held until ‘2022–03–31’ which hasn’t happened yet, we will exclude 2020-based portfolio while calculating portfolio return.

Panel

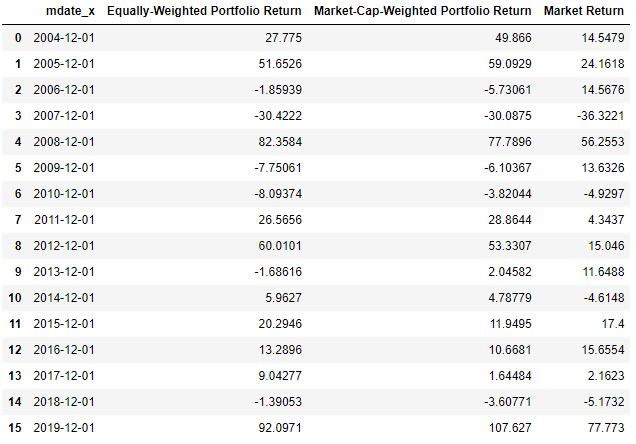

Return

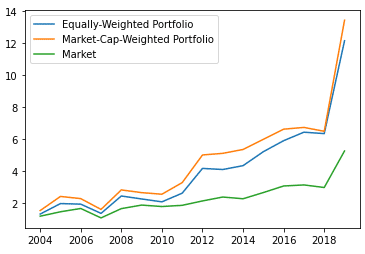

Step 4. Visualize cumulative return (Code can be found in Source Code)

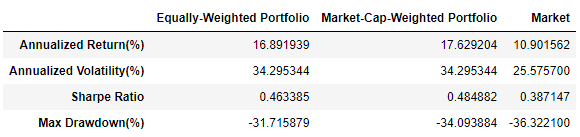

Step 5. Performance (Code can be found in Source Code)

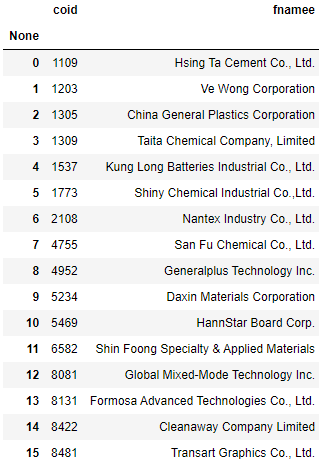

Step 6. Constituent stocks of 2020-based portfolio (Code can be found in Source Code)

Due to the huge data that covers financial, shareholding status and market-side data, we suggest readers begin with fewer firms, shorter time windows or fewer stock selection standards. If the output meets your expectation, then you can examine it from a longer period. In addition to time length, the quality and various data are required. Therefore, we recommend readers to purchase different databases in TEJ E Shop, in order to put those well-known investors’ investing philosophy into practice!

The content of this webpage does not constitute any offer or solicitation to offer or recommendation of any investment product. There may be survivor bias existing since we use current listed companies. It is for learning purposes only and does not take into account your individual needs, investment objectives and specific financial circumstances. Investment involves risk. Past performance is not indicative of future performance. Readers are requested to use their personal independent thinking skills to make investment decisions on their own. If losses are incurred due to relevant suggestions, it will not be involved with the author.