We use Python to backtest Kenneth L. Fisher’s growth stocks strategy on the Taiwan stock market.

Table of Contents

Kenneth L. Fisher, founder and president of Fisher Investments, and his father Philip A. Fisher, a representative of Qualitative Investment in the United States. Warren Buffett cites Philip A. Fisher as one of his two main inspirations for investing [the other is, of course, Benjamin Graham], which shows that Kenneth Fisher’s investment pedigree is very profound.

Fisher believes that a perfect superstock should have the following characteristics: First, it uses its capital to create the future and has a long-term average growth rate of about 15%-20%. Second, a long-term average after-tax profitability rate of more than 5%. Third, the stock price/revenue ratio is 0.75 or lower. In terms of stock selection, Fisher considers two factors: one, the stock price/revenue ratio, and two, the stock price/R&D expense ratio.

1. Stock price/revenue ratio (PSR)

a. Avoid stocks with a PSR over 1.5 and never touch any company with a PSR greater than 3.

b. Actively look for super companies with a PSR below 0.75.

c. When the PSR of any super company rises between 3 and 6, sell your holdings.

2. Stock price/R&D expense ratio (PRR)

a. Don’t buy a company with a PRR higher than 15, there are plenty of super companies with a low PRR.

b. Look for super companies with PRR between 5 and 10. There are not many companies with a PRR less than 5 times.

![]() We summarized and adjusted the above conditions to take into account the change in times.

We summarized and adjusted the above conditions to take into account the change in times.![]()

1. Debt ratio below 35%

2. Average revenue growth rate for the last 5 years≧15%

3. Average net interest rate after tax for the last 5 years≧5%

4. Stock price to revenue ratio (PSR) ≦ 1.5

5. Stock price to R&D expense ratio (PRR) ≦ 15

In addition, since the strategy does not have a clear exit point, but the monthly revenue of Taiwan companies is announced at the beginning of each month, we screen on a monthly cycle and rebalance the portfolio.

IFRS Financial Accounting Accounts Explanatory File (TWN/AIACC)

Listed company adjusted stock price(daily)-ex-right and dividends adjustment (TWN/APRCD1)

Securities Attribute Information Sheet (TWN/ANPRCSTD)

IFRS Consolidated Primary Financial Reports(Single Quarter) — All Industries IV (TWN/AIFINQ)

Listed Monthly Sales(TWN/ASALE)

First, we searched for the required accounting codes from the “IFRS Financial Account Description File”, and then downloaded the debt ratios, net profit margins, and R&D expenses of all listed companies from the “IFRS Consolidated Primary Financial (Quarterly) — All Industries IV” database, while the revenue growth rates and stock price to revenue ratios were additionally retrieved from the “Listed Monthly Sales” database.

Next, Use company codes and specific accounting codes to download the required financial data and monthly revenue information.

After collecting both financial and monthly data, we combined them into one table.

Based on the strategy, we need to calculate the past five-year average annual revenue growth rate, stock price to revenue ratio, and stock price to R&D ratio.

We compose the filter into a function to facilitate further parameter optimization comparisons later, and simply calculate the annualized return, annualized standard deviation, and annualized Sharpe ratio.

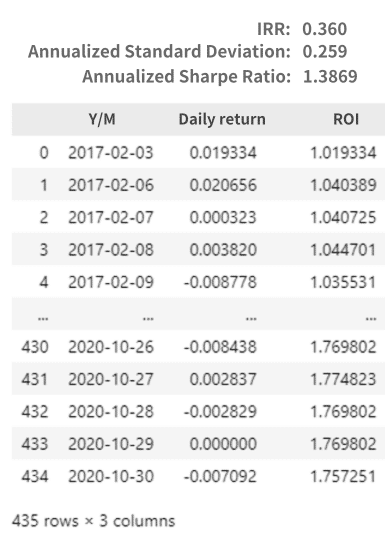

According to the table below, we can see that the three-year investment period eventually has a cumulative rate of return of 75.7%, the annualized rate of return reached 36%, and the Sharpe ratio is 1.3869. Note: The risk-free interest rate is set at 0%.

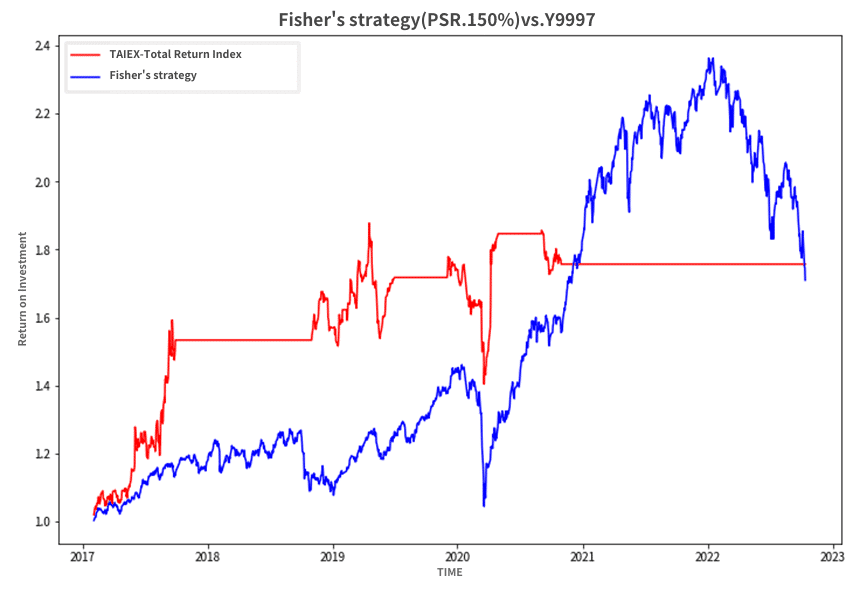

Furthermore, To have a more intuitive view of the strategy’s performance, we have downloaded the broad market return index Y9997 as a benchmark to see if the strategy can beat the general market.

From the chart, we can see that the initial good targets can quickly outperform the general market. However, after the V-shaped rebound in the stock market at the end of 2020, we can not find very good growth stocks. It is mainly because the influx of capital is likely to disconnect the stock price from revenue performance in a short period, which results in the setting of the ratio of stock price to revenue, even limiting the targets that can be found in the surging stock market. In addition, companies that have no R&D expenses in the last year will cause the stock price R&D ratio to be infinitely large, making it eliminated by the condition of stock price R&D ratio <15, and eventually there will be no more suitable targets after the end of 2020.

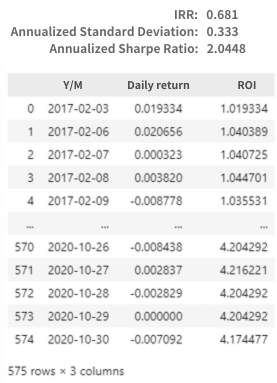

Therefore, to test whether the strategy can outperform the market more significantly, we further relaxed the previous parameters, especially the price-to-revenue ratio, from 1.5x to 2x. As you can see. Although the standard deviation increased after the relaxation, the resulting return was more significant, raising the overall Sharpe ratio from 1.3869 by 47% to 2.0448.

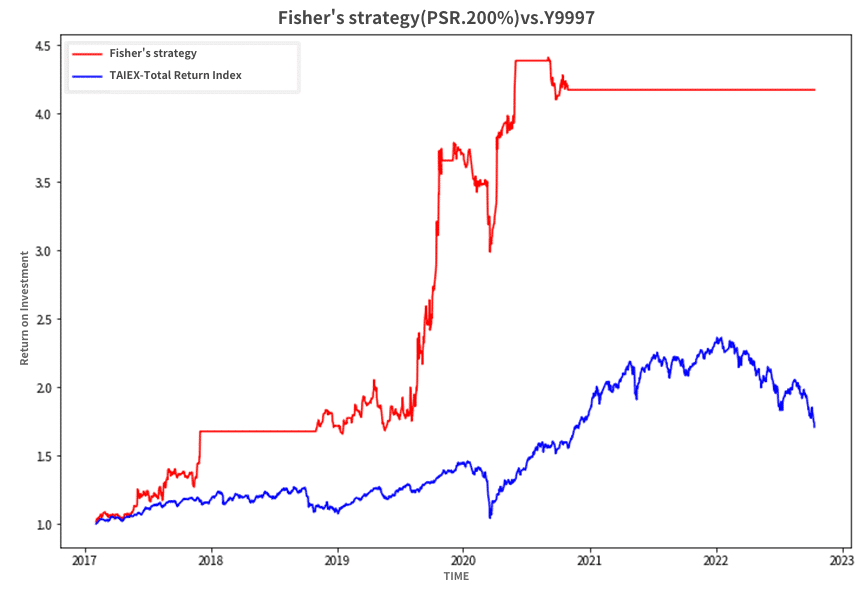

As shown below, there is at least a two-fold difference against the Y9997 benchmark for the same period, and we can even find out that the major payoffs are coming from the mid to late 2019 period.

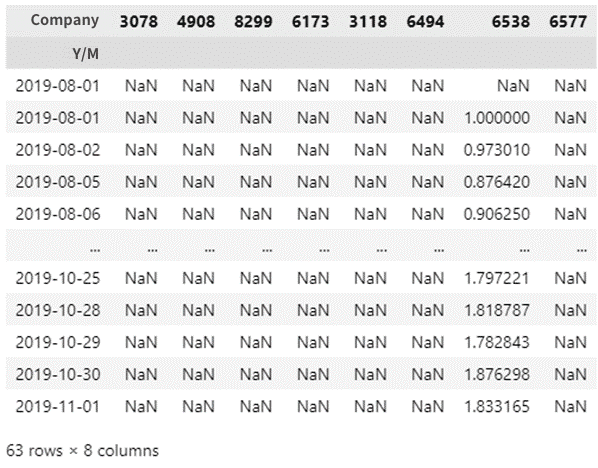

If we break down and further look at this period from 2019/08/01 to 2019/11/01, we will find out that only 6538.TW has a return rate of 83%, making an impressive contribution to the overall investment group.

Overall, Kenneth Fisher’s strategy is centered on finding undervalued growth stocks on a PSR basis, while the company itself also needs to have a continuous investment in R&D and a low debt ratio to increase revenue growth and maintain a certain level of after-tax net profit margin.

However, the original PSR of 0.75x~1.5x is too strict for Taiwan stocks, which makes it hard to find targets with low PSR during a major stock market rebound, but after relaxing to 2x PSR, we have successfully found a starting point for 6538.TW and even increased the return of the investment group. It is important to note that this strategy only provides the logic of stock selection, but not the exit or stop loss settings. If we want to build an investment portfolio based on this strategy, it is recommended to refer to other indicators as the basis for exit points and stop losses.

Last but not least, a profitable investment strategy comes with a comprehensive database, if you are interested in issues like Creating Trading Strategy, Performance Backtesting, and Evidence-based research, welcome to click the link below to see all-encompassing data of TEJ.

TEJ Quantitative datasets allow decision makers to get access to accurate data in real-time and improve strategy performance:

• Avoid look-ahead bias and reduce inaccurate assumptions

• Finding effective factors that facilitate quantitative modeling

Assess to databank