Table of Contents

With the pursuit of ESG among companies, a fair evaluation and remuneration system are key stimuli of implementing actual actions. Given the support of relevant research and the success of real cases, the Financial Supervisory Commission (FSC) announced that this criterion will be included in the latest Corporate Governance Evaluation System. Therefore, linking ESG performance to executive compensation has become a key focus of ESG in Taiwanese companies. This article will introduce the recent global trends in linking ESG performance and compensation, provide examples from well-known domestic and international companies, and help you understand this new ESG trend in Taiwanese businesses.

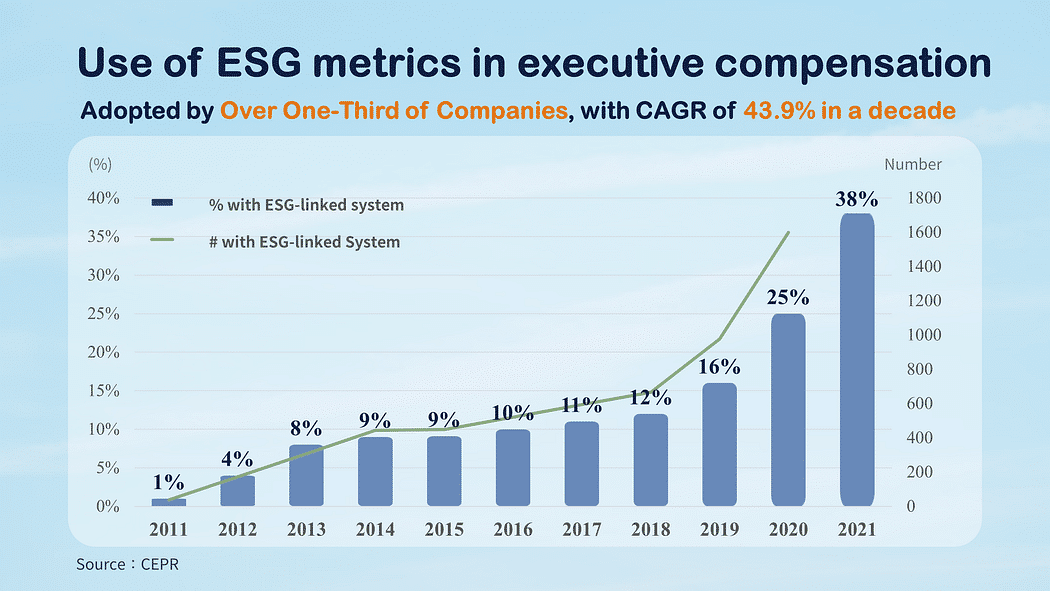

In recent years, ESG has become a global trend, and as more and more companies strive for ESG excellence, they have gradually integrated ESG metrics into their compensation assessment criteria. By providing salary increases or additional bonuses, they incentivize executives to incorporate ESG or CSR into their decision-making processes. According to the research from the Centre for Economic Policy Research (CEPR) in 2021, 38% have adopted ESG-linked systems for executive compensation out of over 1,600 companies worldwide. What’s even more remarkable is that this figure has grown from 1% a decade ago to the current 38%, representing a CAGR of 43.9%. We can know that, as more companies practice ESG transformation, they are also linking their actual results with executive compensation.

On the other hand, research has indicated that linking ESG metrics to executive pay does increase company value. Abdelmotaal and Abdel-Kader (2016), in their analysis of 212 companies in the FTSE 350 index from 2009 to 2011, found a positive correlation between ESG-related compensation and shareholder returns. Furthermore, Flammer et al. (2019), in their study of S&P 500 companies from 2004 to 2013, concluded that adopting such compensation systems increases long-term company value and improves ESG performance. Ikram et al. (2019), in their research on a similar sample of S&P 500 companies from 2009 to 2013, confirmed these findings, showing that companies adopting ESG-related compensation had higher ratings in MSCI KLD ESG.

Given the multitude of academic research supporting the positive effects of linking ESG to executive pay, this system has become a standard for evaluating ESG practices among businesses. However, in actual scenario, how do companies establish ESG metrics and link them to executive compensation?

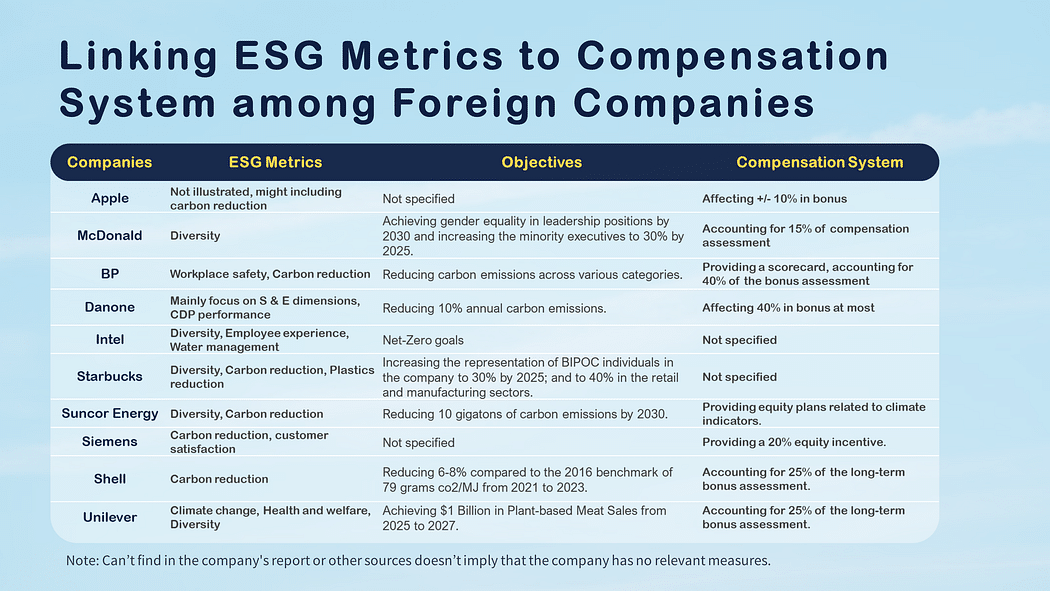

In addition to the aforementioned companies, many well-known companies have already adopted ESG-linked remuneration systems. TEJ has compiled information on several companies and organized it into a table, including the ESG key metrics and assessment systems. It is evident that these companies have identified ESG issues that are relevant to their own operations and have developed corresponding indicators.

However, the majority of companies still tend to focus on metrics within the environmental (E) and social (S) dimensions, with carbon emissions and employee diversity emerging as prominent trends.

Within the context of Taiwan’s companies, while there may not be many companies currently adopting such systems, there is still notable technology companies such as TSMC (2330.TW) taking steps in this direction. In 2021, TSMC implemented a restricted employee stock plan worth approximately 857 million TWD, which includes linking their rewards to shareholder interests and ESG performance. The number of granted shares is calculated based on Total Shareholder Return (TSR), and the compensation committee adjusts the final remuneration based on ESG performance, with a potential impact of up to ±10%. Although the specific performance metrics used have not been publicly disclosed, it can be inferred from company updates that they likely include issues such as water management and carbon reduction, which have garnered attention in recent years.

Other companies, including Taiwan Cement, are committed to low-carbon transformation. Taiwan Cement incorporates non-financial performance aspects such as corporate governance, green finance, social care, and sustainable environment into its evaluation scope. The considered ESG metrics include occupational safety, environmental pollution control, energy efficiency, and carbon reduction, among other sustainability performance metrics.

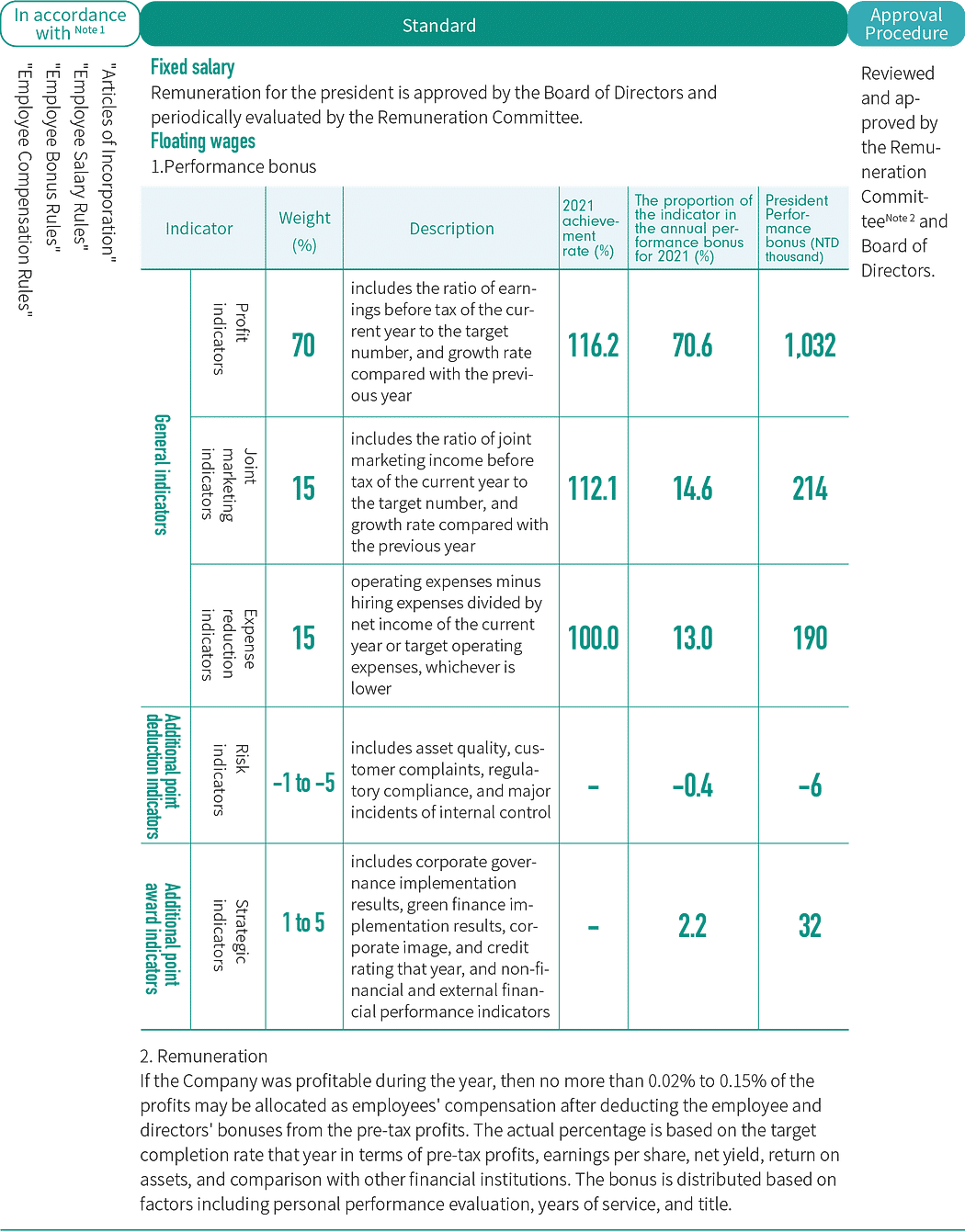

In the financial industry, multiple companies have adopted this system. Taking First Financial Holding Co. as an example, as shown in the diagram below, it includes non-financial indicators such as corporate governance, green finance, social participation, and sustainable environment as bonus factors. The evaluation results are used as a basis for the compensation committee to recommend the annual remuneration for employees (including the CEO) and directors, with an impact of 1–5% on the bonus weighting.

From the above cases, it can be observed that each company is dedicated to implementing ESG performance and linking it to executive compensation. This connection encourages management or decision-making levels to pay more attention to and prioritize the achievement of ESG goals. Such a linkage can also enhance the management’s understanding and awareness of ESG issues, enabling better integration of ESG principles into the company’s day-to-day operations. However, linking ESG with compensation systems still presents some challenges. The potential drawbacks of this system include:

Under the guidance of FSC, Taiwanese companies are expected to follow this ESG trend. Although further analysis cannot be made in this article since the current number of companies implementing this system is still low, stakeholders can use the TESG Sustainability Dataset to examine the ESG performance of companies through 3 dimensions and sub-items, as well as review the data on executive remuneration to identify companies that may only appear to be ESG-compliant but have not actually achieved their ESG goals.

Moreover, academic researchers can utilize the TESG Sustainability Dataset to access executive remuneration data and further explore the relationship between executive remuneration and ESG performance. As more and more companies adopt this linkage system in the future, this approach will help understand the impact of the system on the sustainability development of Taiwanese companies and provide corresponding recommendations and improvement measures.

Lastly, when ESG performance is linked to executive compensation, as stakeholders, we need to pay more attention to companies’ performance in the ESG field. Stakeholder concerns will drive companies to establish and foster a culture of sustainable governance, thereby creating long-term value and higher shareholder returns. Additionally, with more supporting research in the future, it is hoped that this system will further promote the progress of sustainable development.

Read More:

About us

⭐️ TEJ Website

⭐️ LinkedIn

✉️ E-mail: finasia@tej.com.tw

☎️ Phone: 02–87681088