Table of Contents

In the 1980s, Taiwan experienced a landmine debt crisis where numerous companies defaulted on their corporate bonds, leading to severe liquidity problems. To address this issue, guidelines for handling “domestic” troubled corporate bonds were established. Non-performing and illiquid positions were classified into separate sub-accounts to prevent a significant impact on realized values due to insufficient liquidity. Over two decades later, a similar liquidity crisis emerged in funds holding Russian assets during the Russo-Ukrainian War last year. Similarly, the United Kingdom implemented the “side pocket account” mechanism to segregate assets with liquidity issues.

How necessary is asset liquidity? In simple terms, asset liquidity refers to the ability to meet various funding needs and recover funds. When markets experience insufficient trading volume or a lack of willing market participants, liquidity risk can arise. In severe cases, a liquidity crisis may trigger investor panic, leading to massive fund outflows, and financial institutions face more considerable losses or even bankruptcy. Therefore, liquidity risk management is crucial for financial institutions.

This article will briefly explain the liquidity crisis in funds caused by the Russo-Ukrainian War last year and introduce the side pocket account mechanism implemented by the United Kingdom in response to this event. This will help you understand what side pocket accounts are and why they are essential.

In 2022, the outbreak of the Russo-Ukrainian War triggered multiple countries to impose financial and economic sanctions on Russia. As a result, Russia-related assets faced severe liquidity shortages, indirectly impacting the operations of funds holding such assets. Some of these assets became challenging to value or liquidate. In the event of irrational redemptions during this period, funds might incur even greater losses due to the urgency of asset disposal.

Taking the example of the Barings East Europe Fund, which invested in Russian stocks, the fund suspended the calculation of its net asset value and the rights of shareholders to subscribe, redeem, or convert fund units starting from March 2022 to address liquidity issues arising from the war.

To address the fallout from the “foreign” corporate bond event, the Investment Trust and Consulting Association referred to the side pocket mechanism released by the United Kingdom in July 2022. They proposed amendments to the “Calculation Standards for Securities Investment Trust Fund Net Asset Value” and the “Rules for Dealing with Troubled Corporate Bonds.” These revisions were approved by the Financial Supervisory Commission to better cope with the impact of the international corporate bond event.

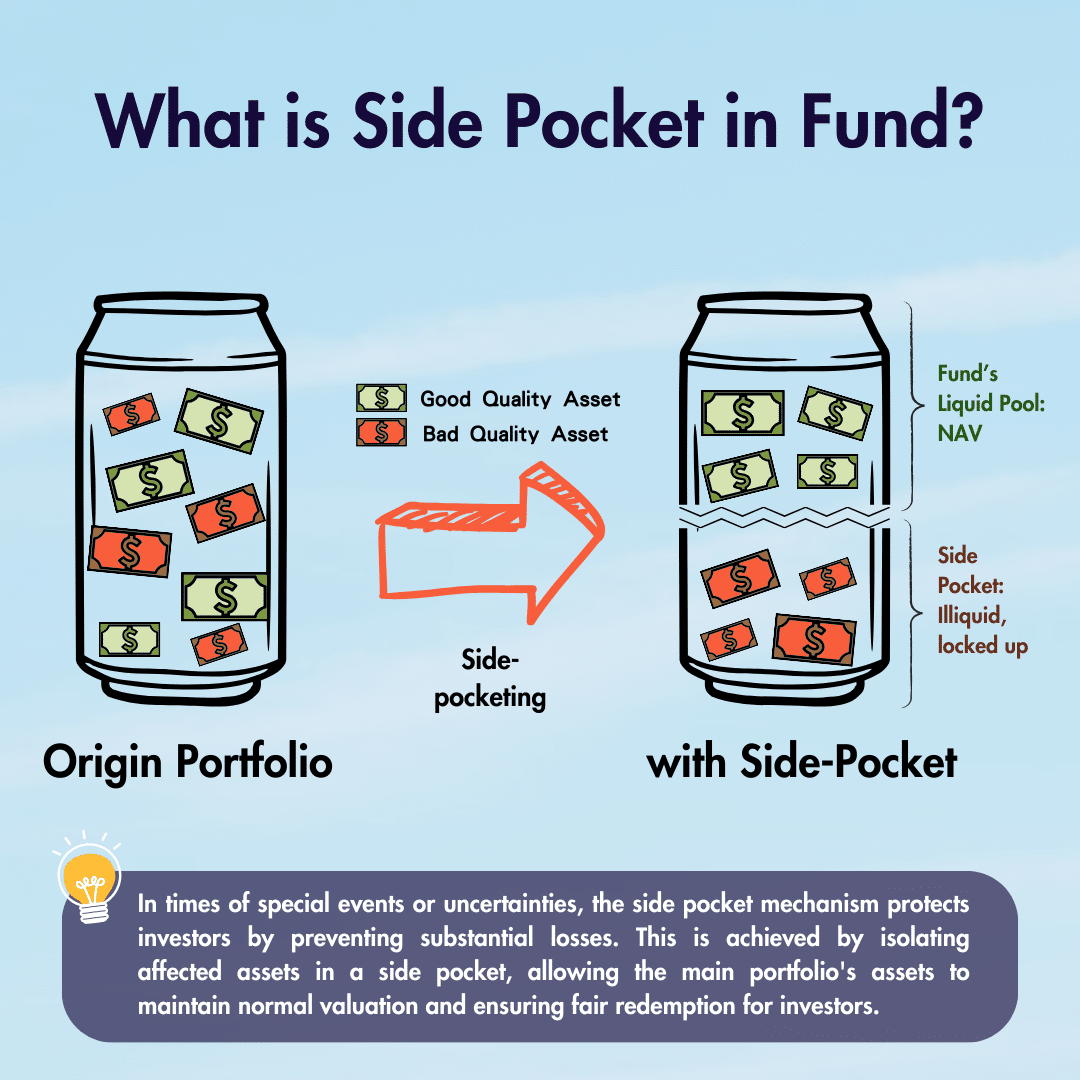

The side pocket account mechanism involves segregating specific assets from a fund’s investment portfolio into a dedicated account, independently managed from the original fund account. It serves as a tool for managing liquidity risk. The fund’s assets are divided into two parts: assets in the side pocket (Liquid Pool) are affected by special events, while assets in the main portfolio are not influenced by these events. Both types of assets are managed and operated independently.

Once the side pocket account is activated, the assets in the main portfolio can be valued. If an original investor chooses to redeem their investment, they will only receive the redemption proceeds from the main portfolio. The assets in the side pocket, however, will need to wait for improved conditions and realization before redemption proceeds are distributed.

For investors who joined after the activation of the side pocket account, they are not associated with the side pocket and only invest in the main portfolio. Consequently, during redemption, they will receive redemption proceeds only from the main portfolio. In essence, transactions are limited to the main portfolio, while the side pocket is held in abeyance until favorable circumstances arise.

In the case of the Barings East Europe Stock Fund mentioned earlier, the fund management explained that, due to investments in Russian stocks, the fund was divided into two funds based on liquidity from July 21. From July 24, the fund with liquidity could be redeemed but not purchased. The other fund, separated into the side pocket account, would no longer incur management fees on illiquid assets. It would undergo liquidation when the assets regain liquidity, and the net assets after liquidation would be redistributed to the original beneficiaries.

The side pocket mechanism in Taiwan is not mandatory but is at the discretion of asset management companies to adopt. To activate this mechanism, amendments must be made to the fund trust agreement and the prospectus, incorporating relevant details regarding the establishment and procedures of side pocket accounts. Asset management companies are required to establish, within their internal control systems, management measures related to the activation of the side pocket mechanism, including the timing, reference date, activation procedures, announcement and notification matters, and regular monitoring mechanisms, all subject to approval by the board of directors.

Upon deciding to activate the mechanism, it is mandatory to announce and notify investors before the established reference date to safeguard investor rights. The side pocket account holds significant advantages in addressing financial market risks. In the face of special events or uncertain situations affecting the fund, this mechanism safeguards investor interests, preventing substantial losses for some investors due to the inability to immediately liquidate assets. By segregating affected assets into the side pocket, the main portfolio’s assets can still be valued normally, ensuring that investors can redeem their shares fairly.

However, side pocket accounts also come with some potential drawbacks. The assets in a side pocket account may be subject to special terms or rules, restricting investors from redeeming or transferring these assets immediately, thus limiting the utilization of investors’ funds. Additionally, the effective use of side pocket accounts requires asset management companies to establish robust internal control measures to ensure their proper functioning and the realization of expected benefits.

In addition to addressing issues such as liquidity and uncertainty, side pocket accounts are commonly employed internationally for long-term investments, particularly in areas such as private equity funds and real estate funds. These investments typically take a longer time to generate returns, and side pocket accounts prove valuable in helping fund managers more effectively manage liquidity and risks. With regulatory improvements, they serve as an effective tool to assist investors in better navigating market challenges, providing reliable protection for both investors and asset management companies!

Read More:

Want to know more?

Datasets→ Fund Data

Daily net worth, holdings, dividend allocation, and performance information for domestic and international funds in Taiwan is available in the TEJ Dataset; click here for full details!

If you have any questions about this article or want to obtain further access to the TEJ database, please feel free to leave a comment, call, or mail us.

About us

⭐️ TEJ Website

⭐️ LinkedIn

✉️ E-mail: finasia@tej.com.tw

☎️ Phone: 02–87681088

Your encouragement drives us to continue sharing more on TEJ Dictionary!

If you think this article is helpful, click the clap button until it hits 50. You can also leave a comment and share any ideas with us.