As America continues to maintain a high-interest rate, the borrowing cost for companies still remains at a peak. However, compared to other bonds, bonds related to ESG enjoy a lower yield, but seldom do we see small or startup companies issue green bonds. This is because issuing green bonds requires the funds only to be used on certain ESG projects, which is normally not the primary goal for small and startup companies. Hence, a new type of bond, Sustainability-Linked Bonds, is created. In this article, we will briefly introduce the concept and principle of Sustainability-Linked Bonds.

Table of Contents

Sustainability-Linked Bonds (SLBs) are fixed-income financial instruments that usually have a yield lower than normal bonds. However, on SLBs, there are some conditions, requiring the company to meet certain sustainability or ESG goals in a given timeframe. If the company fails to achieve those targets, a penalty of higher interest is given to investors. SLBs are designed to be a supplement of green bonds, aiming to provide easier access to finance in the sustainable debt market for small companies.

In order to provide a clear guideline for issuers, investors and underwriters on SLB, ICMA (International Capital Market Association) issued the Sustainability-Linked Bond Principles (SLBP) with 5 main components:

In September 2019, ENEL, an energy company based in Italy, became the first issuer of SLB with a total initial issuance of US$1.5 billion, which then got oversubscribed by almost three times. Normally, a conventional bond without sustainability elements is priced 10 bp higher than US Treasuries. However, the SLB that ENEL issued was priced at 125 bp over US Treasuries, suggesting both great interest and potential in SLB. Moreover, the funds raised through SLB can be allocated to any project, as long as ENBL fulfills the SPT of having renewable energy to account for 55% of its installed electricity generation capacity by 2021. Otherwise, ENEL will suffer a 25 bp increase in coupon as a penalty.

After 2019, ENEL continued issuing new SLBs, and received great favor from the market. At the end of 2021, ENEL met its targets for its first SLBs, and successfully met its target for 2022, which is achieving 60% of its overall installed generation capacity from renewables. Despite the speculation, ENEL continues making ambitious SPTs, and has now become the world’s largest issuers of SLBs.

Green bonds and Sustainability-Linked Bonds (SLBs) are distinct in their application and flexibility:

SLBs aim to further develop the key role that debt markets can play in funding and encouraging companies that contribute to sustainability from an ESG perspective. However, like every green bond, SLBs have the risk of greenwashing. Since companies define their own SPTs and KPIs, it is possible for ill-intentioned companies to set up targets that can be easily achieved. As a result, companies can raise funds with less interest, while investors can gain a reputation from “Green Investment”, thereby reducing the incentive for companies to set more challenging goals.

Trends in the SLB market suggest a promising trajectory with significant growth potential. As more companies prioritize sustainability and investors seek impactful ESG investments, SLBs offer a dynamic solution that aligns financial goals with environmental and social objectives. The evolving landscape of sustainable finance continues to foster innovation, leading to the development of new financial instruments like SLBs that catalyze positive change.

For investors looking to make a difference while achieving financial returns, exploring sustainability-linked bonds is a prudent step. Incorporating SLBs into a diversified investment strategy focused on sustainability not only supports responsible business practices but also positions portfolios for long-term resilience in a changing world.

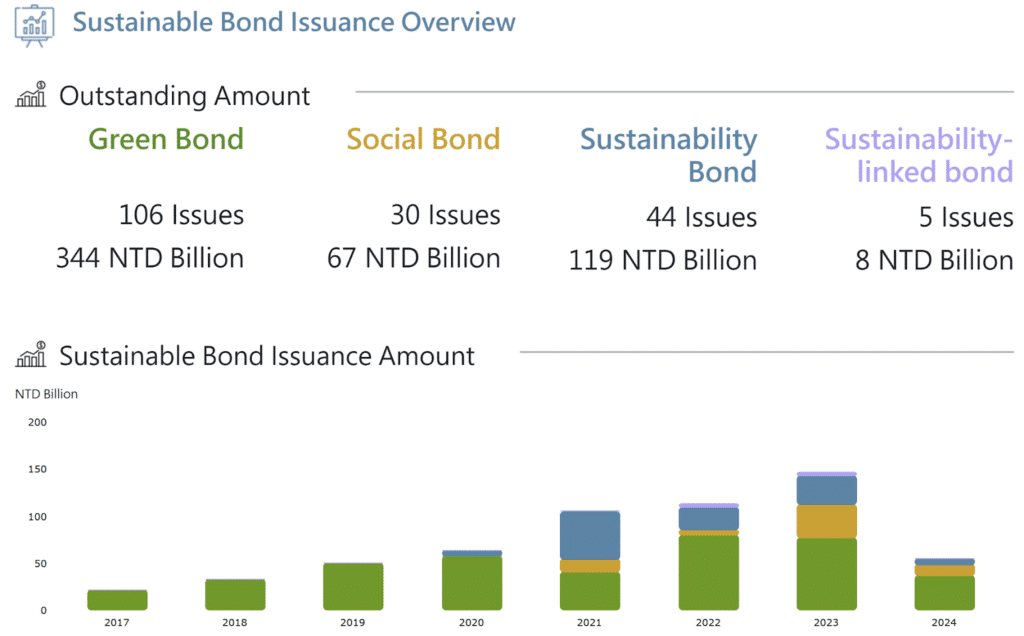

In recent years, ESG-related bonds in Taiwan have gradually gained the favor of investors. Based on data from Taipei Exchange (TPEx), until May 2024, ESG-related bonds in Taiwan have accumulated 538 billion NTD starting from 2017, with green bonds accounting for 64%.

With the development of ESG issues, related financial instruments have also seen vigorous growth. Investors can utilize ESG datasets to monitor issuers’ ESG performance and ensure that the objectives of SLB bonds are gradually being achieved.TEJ Sustainable Dataset includes ESG bond data from seven Asian countries, allowing for in-depth exploration based on individual bonds and horizontal data integration based on issuers. Moreover, leveraging its extensive database for quantitative analysis and international ESG standards, TEJ has developed the TESG Sustainability Development Index specific to Taiwanese listed companies. Get TEJ Sustainable Dataset provides you with stronger data support for your sustainable investments.