Table of Contents

As investors, formulating strategies only after observing news events can often prove to be too late. The recent ownership transfer event involving TaiShan (1218.TW), was not a sudden occurrence confined to a few days of media coverage. Rather, it spanned several months, involving a back-and-forth struggle between the management faction and the market faction. This included three shareholder meetings that seemed unclear in their objectives and swift divestment of securities along with reinvestments.

Changes in ownership are often preceded by signs. By closely observing a company’s policies, statements, and plans over a period of time, one can often discern longstanding internal conflicts among the top management of a company, as was evident in the Taishan case. However, in the case of smaller companies with less media coverage, would investors still be able to timely detect these management warning signs?

In 2014, the Corporate Governance Center of the Taiwan Stock Exchange introduced the “Stewardship Code for Institutional Investors.” This initiative aims to encourage institutional investors such as government funds, insurance companies, and mutual funds to actively engage with the listed and OTC companies they invest in as shareholders. As their influence in the market grows, these investors are expected to fulfill their election and communication responsibilities, prompting companies to enhance their corporate governance practices both locally and internationally.

According to the Stewardship Code for Institutional Investors issued by Taiwan Stock Change (TWSE), it broadly refers to:

In today’s diversified financial services market, the influence over the market environment and the businesses is significant. As a result, investors should consider the long-term interests of capital providers rather than short-term capital gains. They need to approach this from a shareholder perspective by focusing on the operational management of invested companies. This involves participating in shareholder meetings, voting on resolutions, appropriately communicating with management, disclosing or establishing conflict-of-interest management, etc. The document also outlines six stewardship principles for institutional investors to follow:

Moreover, TWSE periodically discloses the results of stewardship list ratings and sets criteria for rating scores, assisting investors in staying updated on the latest trends.

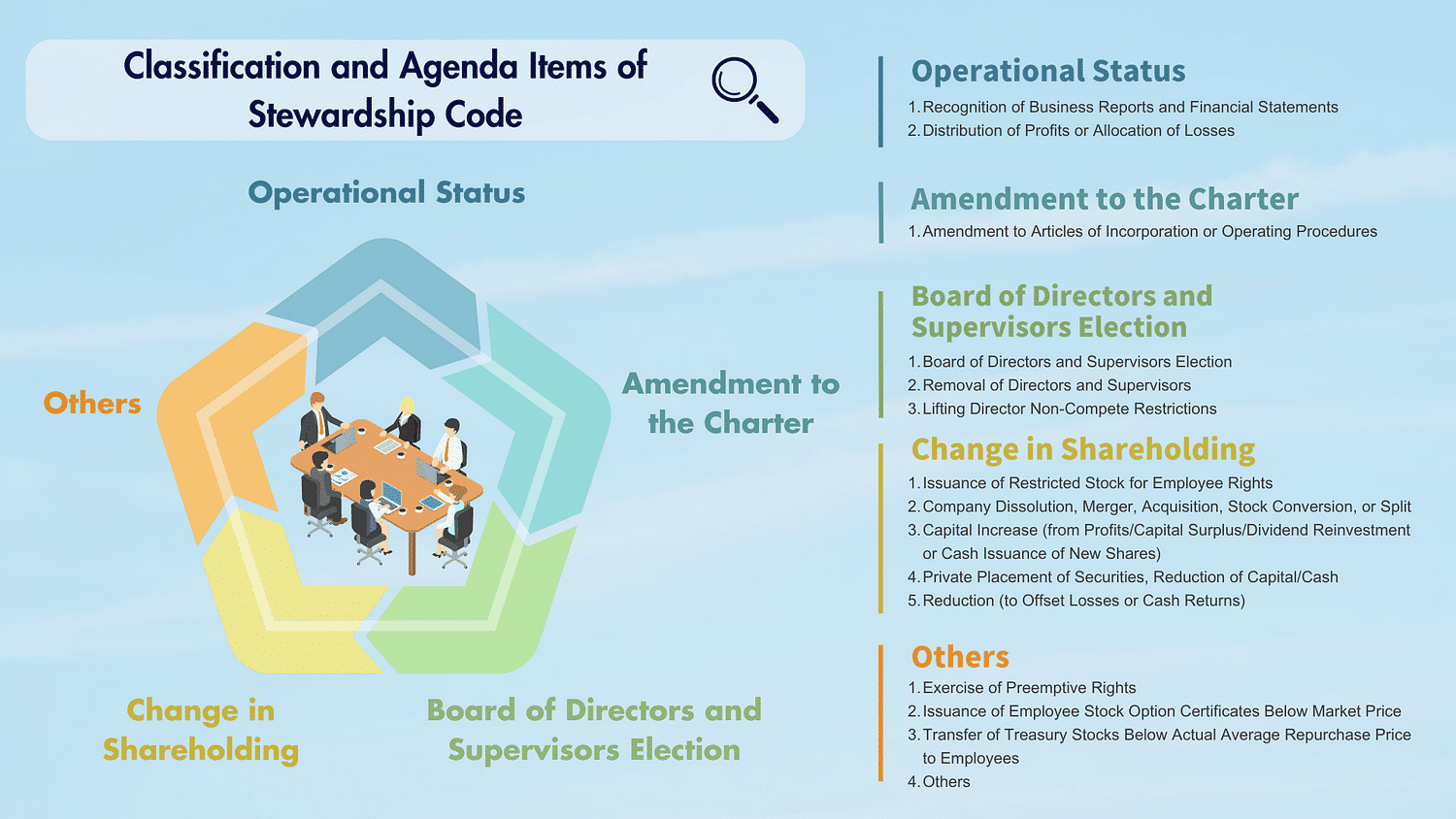

As for TEJ, we listed 15 directly relevant resolution categories to stewardship principles, which can be roughly grouped into five types:

The Stewardship Code, born as institutional investment proportions gradually increased within the market, has been an established investment theory for years. It has the potential to create a win-win situation for corporations, fund providers, and investment institutions, benefiting the entire market.

However, institutional investors in this process need to play multiple roles, acting as observers and implementers from different standpoints. They are not only investment planners wielding significant capital, but also shareholders of invested companies. Furthermore, they might be individuals responsible for significant obligations towards fund providers. This complexity can lead to confusion regarding how to fulfill the broad objectives of the Stewardship Code.

Numerous studies indicate that investors sometimes struggle to take on the role of company managers due to potential conflicts with their inherent investment philosophies. For instance, a heavily diversified portfolio to mitigate risk and the pursuit of maximum short-term gains for fund providers can clash with such a role. This might result in institutional investors wielding considerable influence yet making incorrect or passive interpretations of shareholder responsibilities and proposals, even lacking the basis to veto significant proposals.

Since 2017, the stock exchange has released the Stewardship Code and related Q&A sets. Furthermore, through the Stewardship Information Disclosure and Rating Reports of 2019 and 2021, there has been a continuous drive to promote the practical significance of stewardship governance assessment, disclose preferred lists and recommendations, incorporate and strengthen ESG policies, and facilitate collaboration among multiple institutions to drive proposals. These efforts enable external investment institutions to more easily grasp the practical aspects of stewardship governance.

In March 2023, the Financial Supervisory Commission (FSC) introduced the “Sustainable Development Action Plan for Listed Companies” by referencing foreign corporate sustainability practices. An illustrative case for the prospective application of this initiative is the recent dividend distribution controversy involving Catcher (2474.TW), a notable publicly listed company. Earlier this year, several foreign institutional shareholders questioned the company’s intent in repurchasing treasury shares five times within three years. Additionally, concerns arose due to the mismatch between the company’s EPS and cash compared to subsequent dividend distribution. As a result, a proposal was put forth to allow shareholders to determine the dividend amount through a shareholders’ meeting.

One of the objectives behind the FSC’s introduction of this sustainable development plan is to foster a collaborative platform for institutional investors. This platform enables investors to engage in cooperative discussions with companies to identify areas for improvement. The Securities and Futures Institute also intends to propose the establishment of domestic proxy advisory firms to the FSC. This move aims to enhance the appeal for foreign investors to participate in Taiwan’s market as shareholders. This undoubtedly significantly increases investors’ influence over company operations and bolsters their responsibility in overseeing companies and disclosing potential issues.

From the perspectives of both investors and shareholders, shareholder meeting resolutions can contain substantial operational information. Actions such as exercising voting rights and frequent treasury stock operations can reveal hidden information through long-term or cross-sectional analysis of resolutions. Responsible stewardship also encompasses actively proposing risk-reducing measures to the company.

For instance, we can illustrate this concept using the TEJ’s Stewardship Code resolution database. By gathering data from the announced or completed stewardship resolutions of 2142 shareholder meetings up until 2023, we can observe the distribution of two less common resolutions as follows:

If your investment portfolio includes the company that initiated the aforementioned resolution and the company hasn’t provided detailed explanations within its disclosure information, it becomes essential to conduct a more in-depth analysis of the company’s underlying risks to protect your investment assets and interests.

Utilizing the warnings provided by Table 1, adjusting the sorting order, and selecting all companies that proposed the “Transfer of Treasury Shares Below Average Price Resolution” in 2023, you can then undertake a more extended observation of these specific companies. Remarkably, some companies have even proposed this resolution twice within a three-year span. If shareholders find themselves questioning this operational strategy, initiating a engagement with the management becomes a prudent step.

Furthermore, if a company proposes something that completely contradicts the overall environmental allocation, it will stand out. You can start by observing the overall situation from the previous table and then examine the distribution or trends within each subgroup. This helps you compare ongoing or upcoming shareholder meeting resolutions and identify potential conflicts of interest or risks.

Afterward, institutional investors can utilize Stewardship Code Disclosure Assessment Reports from the TWSE. This data helps identify and manage shareholder meetings held by target companies, assess the potential impact of the Stewardship Code on gains and losses, determine their stance on resolutions, offer recommendations, potentially adjust their investment portfolios, and strategically plan for the governance of target companies and the disclosure of conflicts of interest in the long term.

So far, we have understood the significance of company resolutions, the disclosure of risks and conflicts of interest, the prospect of driving discussions, communication, and accelerating ESG development. In fact, both domestically and internationally, scholars continue to research various relationships between resolutions, management, and shareholder voting. This ranges from the impact of voting turnout to whether management releases positive news before shareholder meetings. Shareholders are motivated and obliged to exercise their responsibility to oversee company operations to protect their assets and interests. Similarly, companies need shareholders to exercise their voting rights to ensure the smooth operation of the company.

However, another factor limiting investors in fulfilling their responsibilities is the allocation of limited time. Considering an investment portfolio, it may not be feasible to focus on just one or a few companies; investors might need to attend numerous company shareholder meetings each year. Each company could have multiple resolutions and changes in ownership structure that require organization. This necessitates thorough preparation before participation in shareholder meetings and post-meeting work involving data organization and record-keeping.

Want to know more?

TEJ’s database offers detailed records of shareholder meeting agendas, including proposals, director nominations, voting outcomes, dividend distributions, and more. Using these tools helps streamline data management, making it easier to uncover key insights amid dynamic information changes, greatly supporting stewardship code implementation.

If readers have questions about this article or would like to obtain further information about TEJ’s database, please feel free to leave a comment and send us an email for inquiries.

Read More:

The Stewardship Code emphasizes institutional investors’ responsibility for stewardship, including considering ESG factors in their investments and engaging in constructive communication with investee companies. The goal is to promote investee companies’ sustainable development, benefit clients in the long term, and contribute to society positively.

TEJ provides the TESG Sustainable Solution, which includes ESG ratings and company ESG information, providing a one-stop solution that saves you time and effort, making your engagement more efficient and enabling precise ESG scrutiny!

About us

⭐️ TEJ Website

⭐️ LinkedIn

✉️ E-mail: tej@tej.com.tw

☎️ Phone: 02–87681088