Table of Contents

when the United States 10Y Government Bond -United States 2Y Government Bond <0 ,we call it yield curve inversion 。

Usually longer-term bonds will have higher interest rates, but when the market have doubts about the economy ,yield cruve inversion happen! So in this article , we try to plot the Macroeconomic Index a year before it happened, and two years after it happened

Window10 Spyder(anaconda31)

macroeconomic data :macroeconomic data database code (GLOBAL/ANMAR)

#######################3

from datetime import datetime, timedelta

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

#########################3

import tejapi

import plotly.graph_objects as go

import plotly.io as pio

##################

pio.renderers.default = 'browser' ##PLOT IN WEB

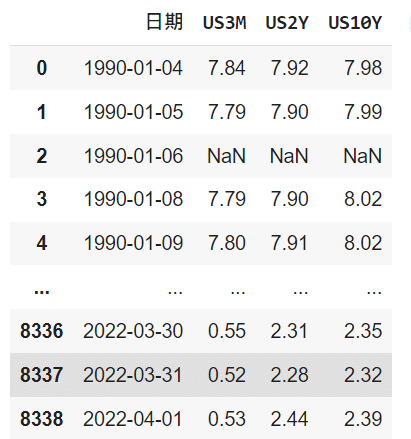

our bonds data is from Tej pro

df=pd.read_excel("C:\\Users/user/Desktop/Tej/美國公債殖利率.xlsx")

There is Nan in our data , so we should drop it ,After we reset index

df.dropna(inplace=True)df.reset_index(drop=True,inplace=True)

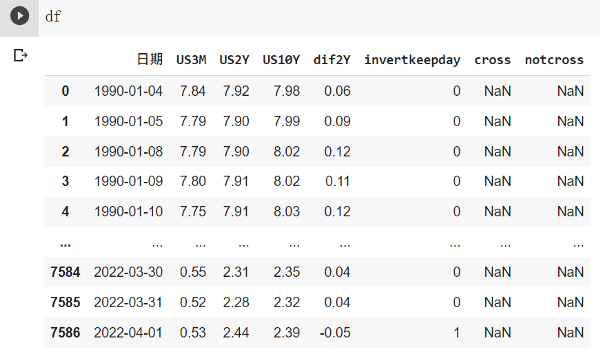

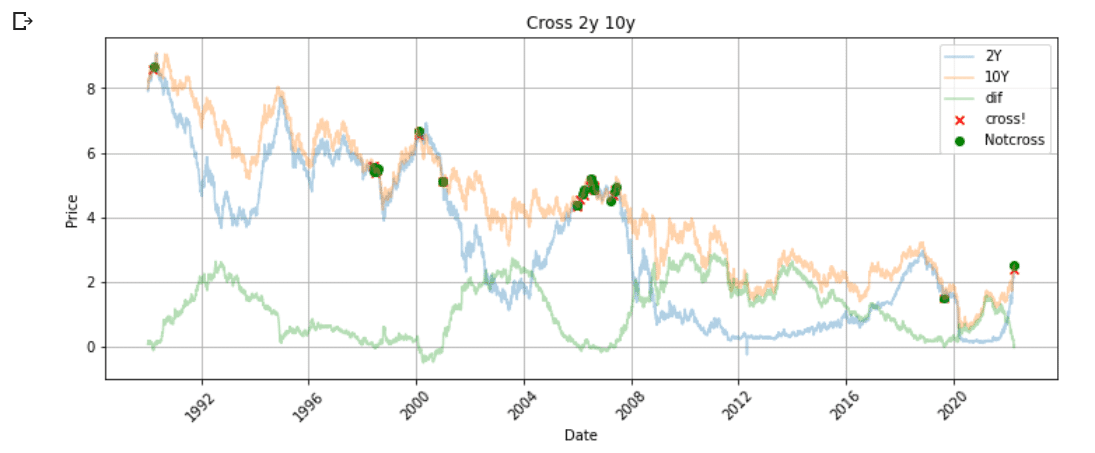

df["dif2Y"]=df.US10Y-df.US2Y

df["invertkeepday"]=df["dif2Y"].apply(lambda x : 1 if x < 0 else 0 )df["cross"]=np.nan

df["notcross"]=np.nan

calculate the 10y- 2y

find the inverse day and visualize it

startday=[]

endday =[]

keep = 0

df=df.copy()

for i in range(len(df)):

if df["invertkeepday"][i] >0 :

if keep == 0:

df["cross"][i]=df["US10Y"][i]

startday.append(df["日期"][i])

keep = 1

elif keep == 1 :

df["notcross"][i]=df["US10Y"][i]if df["invertkeepday"][i] < 1 :

endday.append(df["日期"][i])

keep = 0

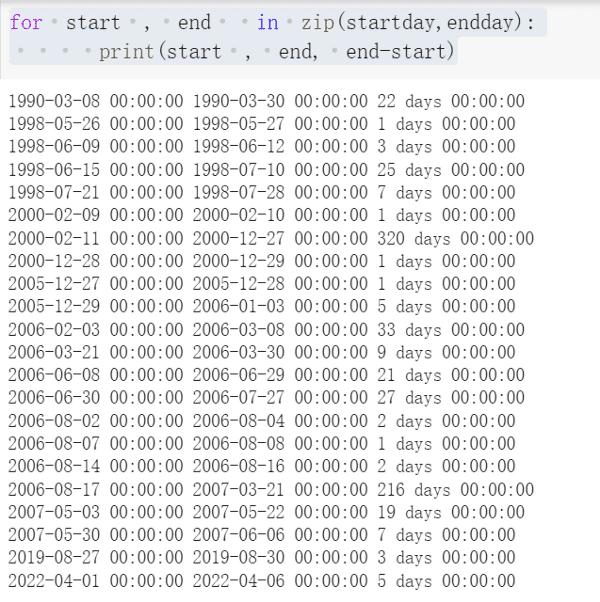

and we want to see how long did it happen

for start , end in zip(startday,endday):print(start , end, end-start)

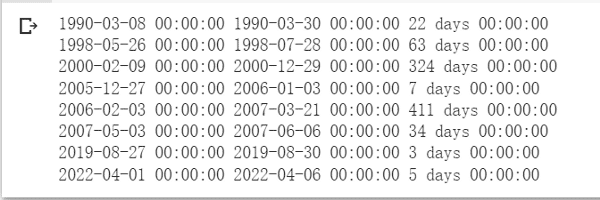

We found that some times were really close ,so we make them in a group

inverted=pd.DataFrame(endday,startday)

inverted.reset_index(inplace=True)

inverted["year"]=inverted["index"].dt.year

datetime=inverted.groupby('year')

datetime=list(datetime)

getstart=[]

getend =[]

for i in datetime :

i[1].reset_index(drop=True,inplace=True)

start = i[1]["index"][0]

end = i[1][ 0][len(i[1])-1]

getstart.append(start)

getend.append(end)

for start , end in zip(getstart,getend):

print(start , end, end-start)

Now we can see the approximately situation

Nearly three years we found that there have about 6 times yeild curve inverse

df.set_index("日期",inplace=True)plt.figure(figsize=(12.2,4.5))

plt.scatter(df.index,df['cross'],color='red', label='cross!',marker='x',alpha=1)

plt.scatter(df.index,df['notcross'],color='green', label='Notcross',marker='o',alpha=1)

plt.plot(df["US2Y"], label='2Y', alpha=0.35)

plt.plot(df["US10Y"], label='10Y', alpha=0.35)

plt.plot(df["dif2Y"], label='dif', alpha=0.35)plt.title('Close Price Buy & Sell Signals')

plt.xticks(rotation=45)

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend()

plt.grid()

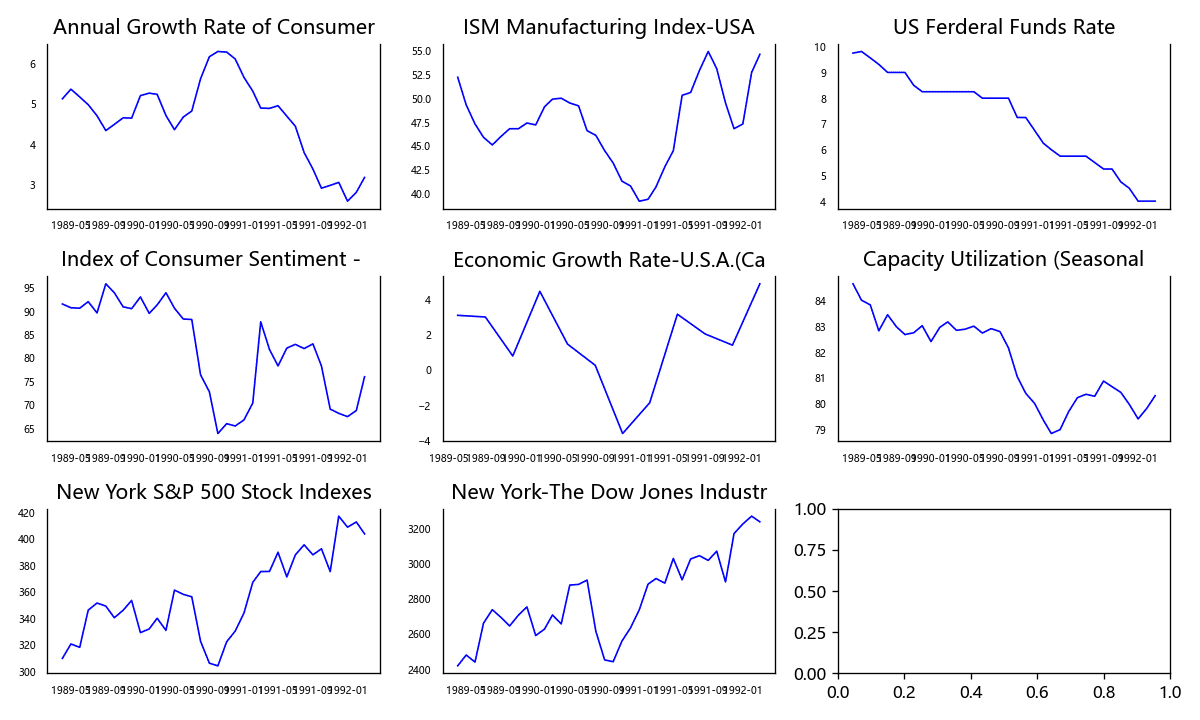

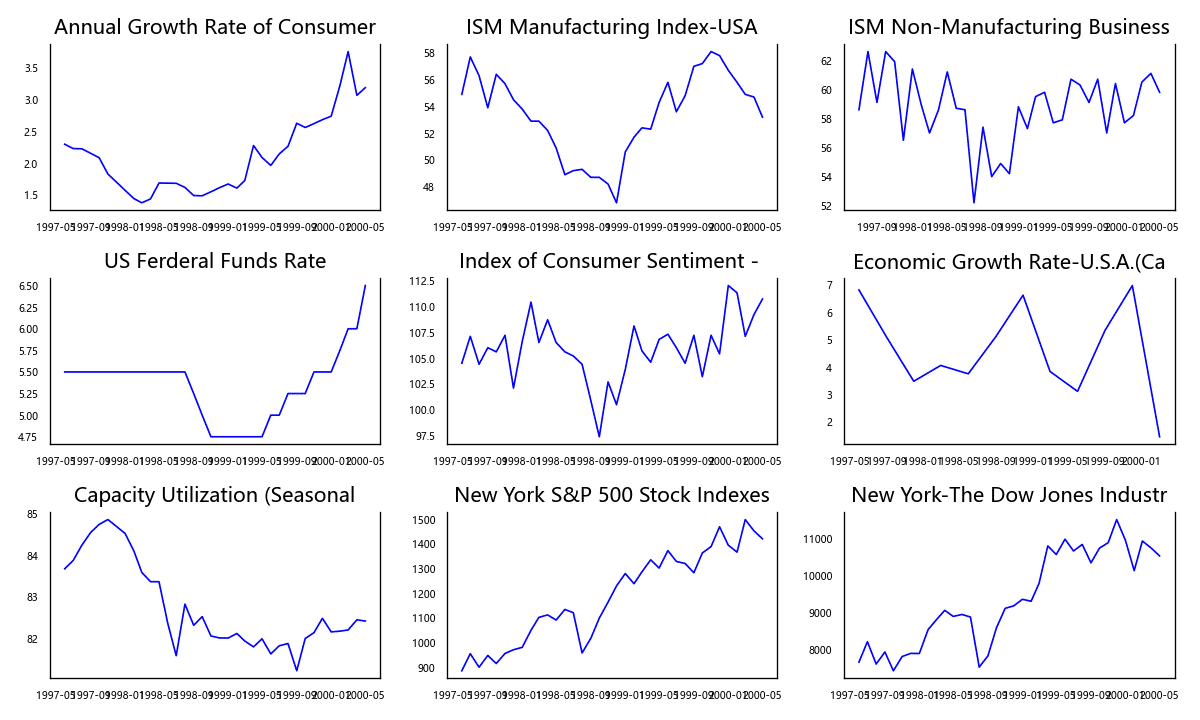

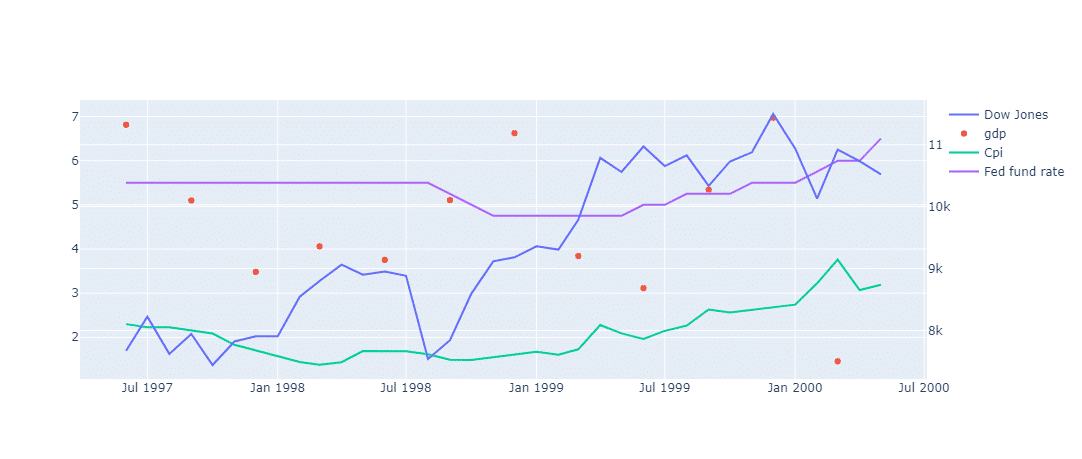

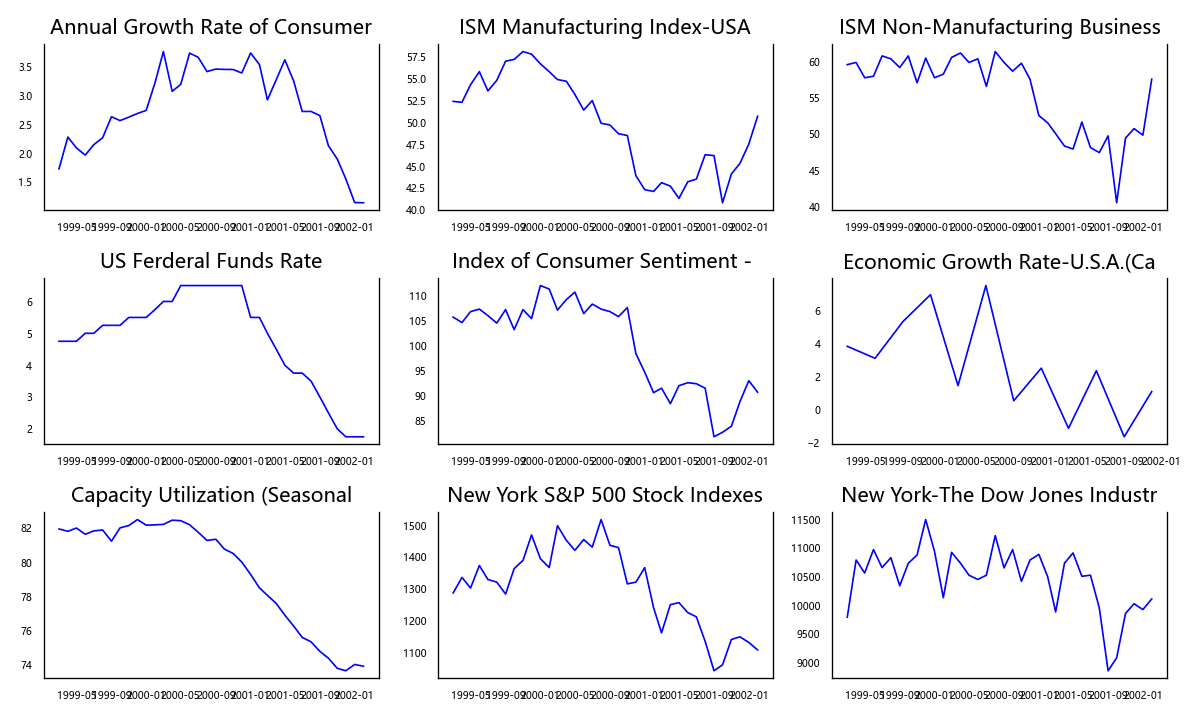

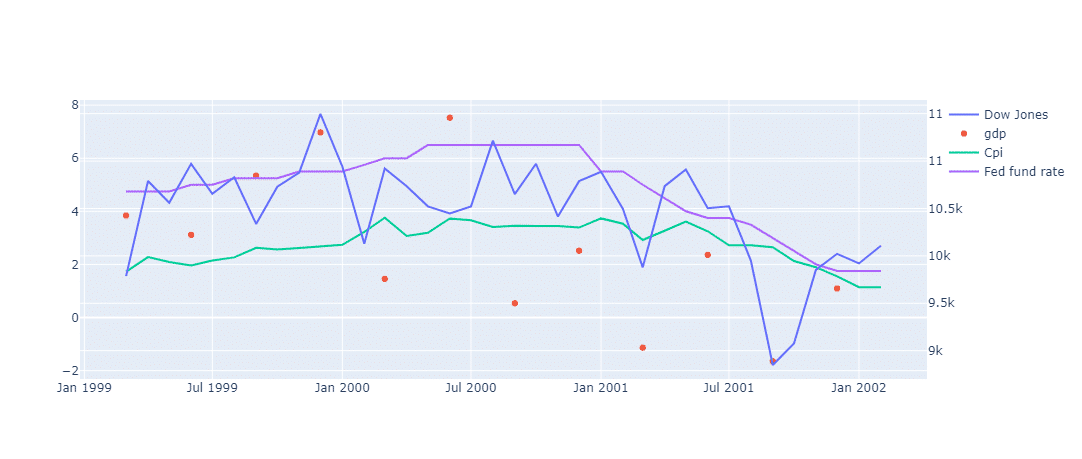

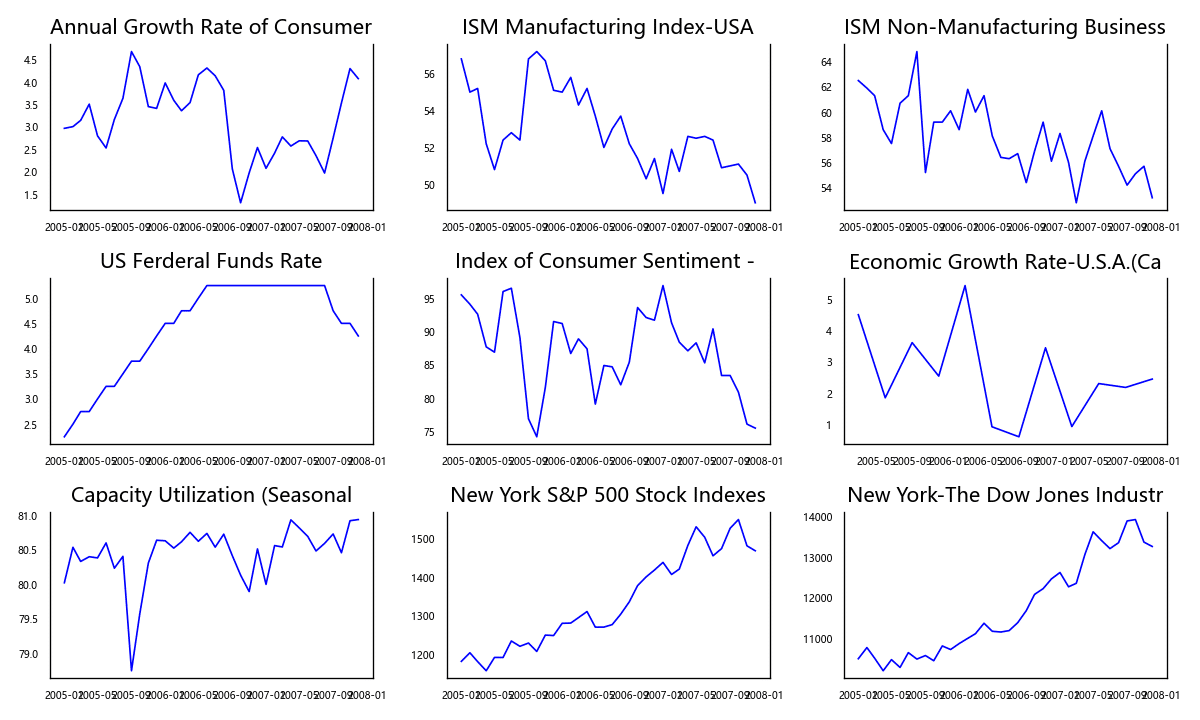

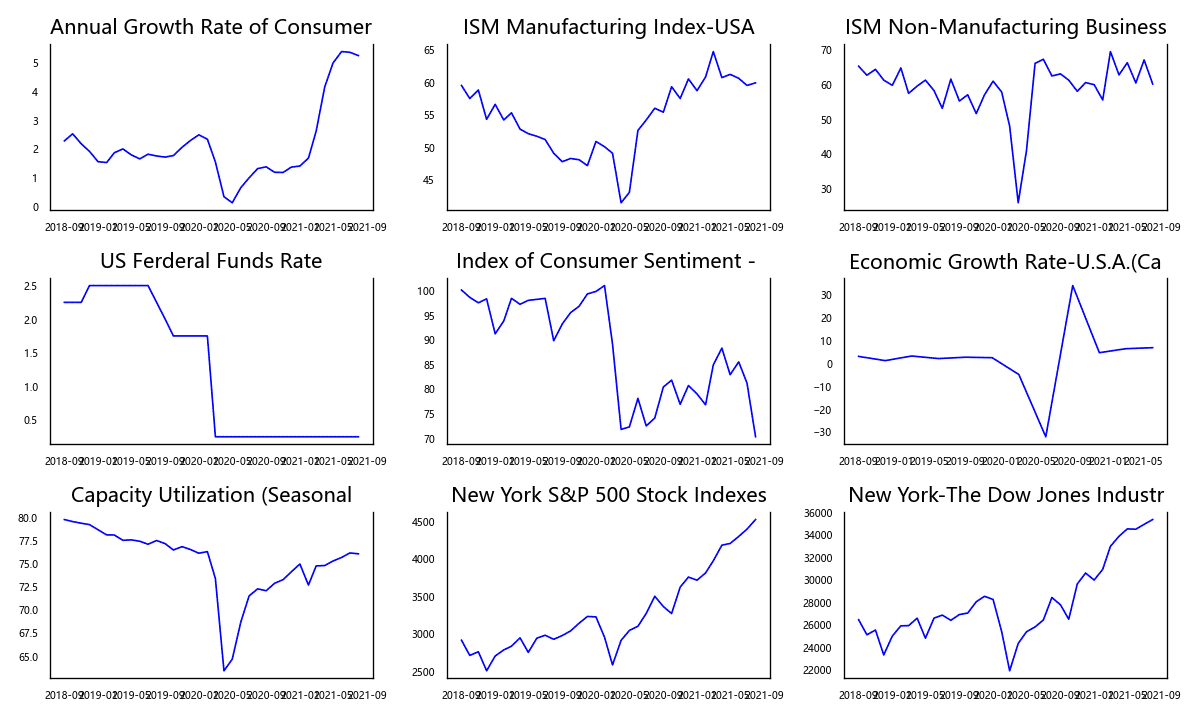

we have the time so we can input the time into Tejapi to get the macroecnomic data

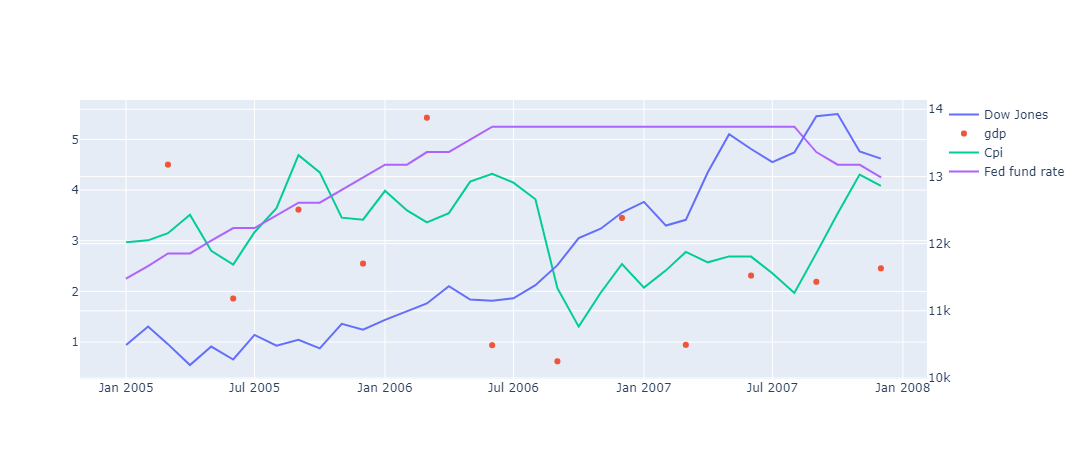

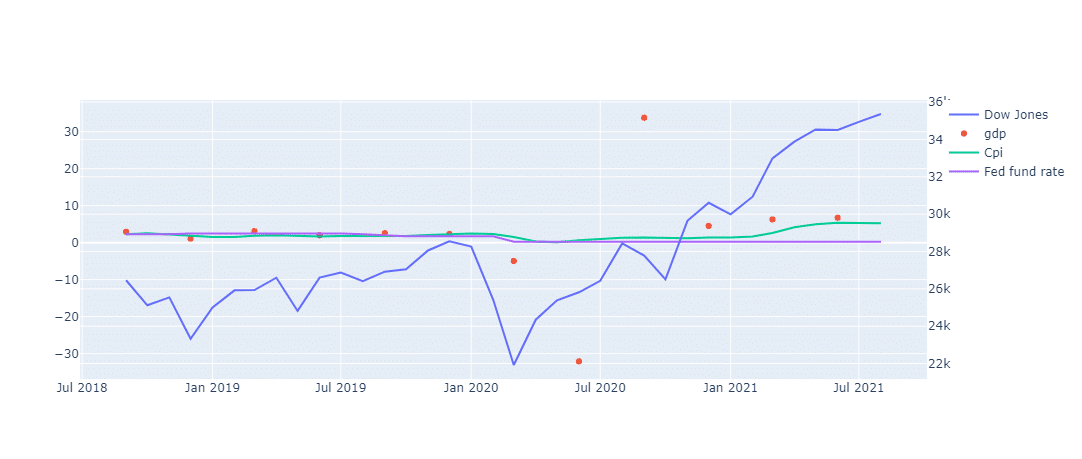

From the perspective of various economic data, it may represent that the prosperity has passed its peak, so there are doubts about the future prosperity, selling short-term bonds and preferring longer-term bonds, which leads to the inversion of yield curves

Although every time an inversion occurs, it will be accompanied by an recession, but in these five expreience ,there was two times that the U.S. economy has not experienced a recession within two years

In 2019, the recesion happen because of the COVID-19 , yield curve can’t forecast it !

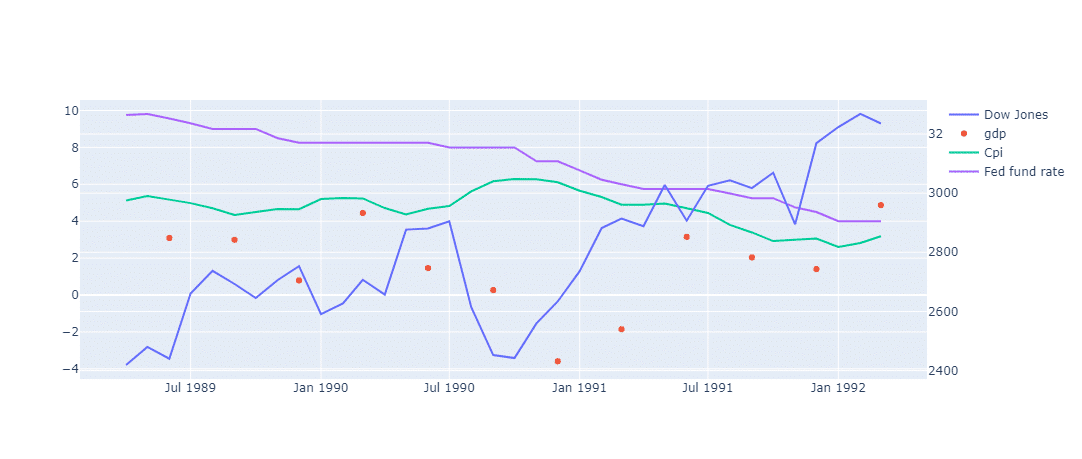

1, In the past 5 inversion ,stocks go up 4 time

2, When three recessions occurred, they were all in a rate-cut cycle, and when two recessions did not occur, the U.S. was in a rate-raising cycle

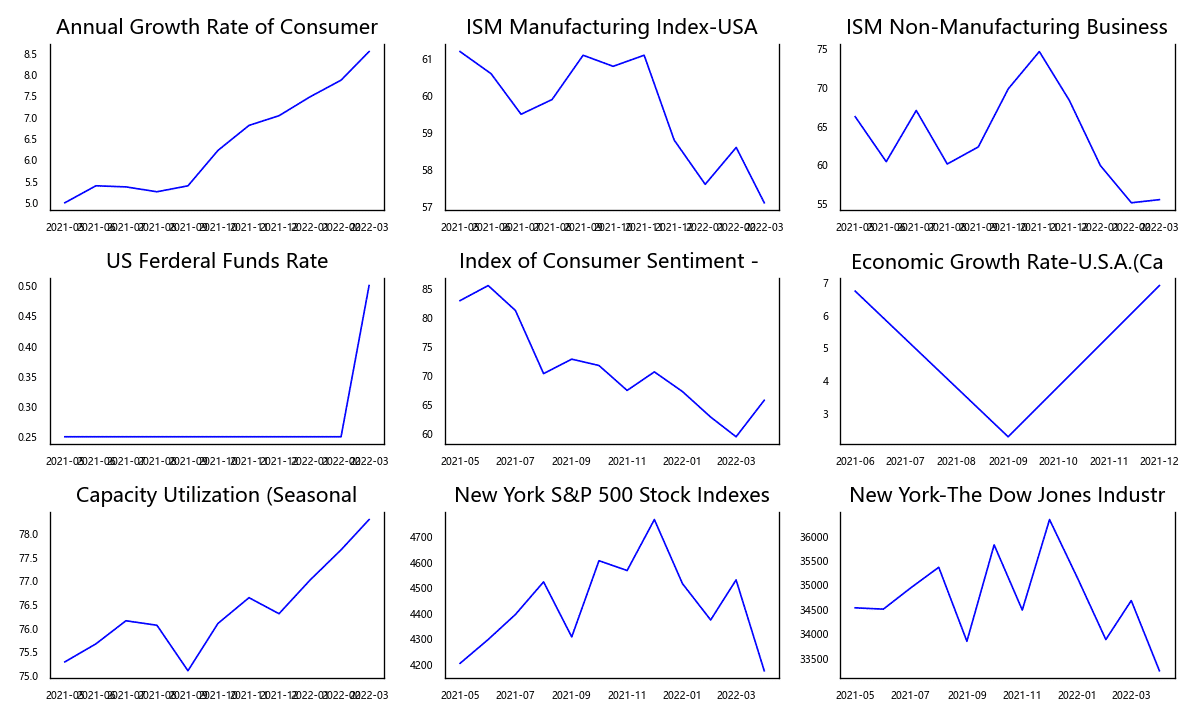

What about now ?

At present, although the peak of the US economic data has passed, it is still maintain at a very high level. Because of the strong economic performance, the US Federal Reserve has entered a cycle of raising interest rates. Although each inversion will be followed by a recession, this indicator It is a very leading indicator. The past five inversions between the 2 Y and the 10Y have taken an average of 18 months before a recession occurs. Perhaps the inversion is trying to tell us

Hey ! it’s time to be aware of the risks