The International Energy Agency (IEA) released the “Net Zero by 2050: A Roadmap for the Global Energy Sector” report in 2021. More than 130 countries around the world have responded. The same year, my government revised its long-term carbon reduction target to net zero carbon emissions in 2050. And continue to amend the law to improve the climate legal environment, expecting to be in line with international standards and continue to promote sustainable development plans.

Responses to relevant carbon reduction policies must be based on a greenhouse gas inventory. The first essential action is establishing greenhouse gas emission data of suppliers, also known as “carbon inventory.” This article will guide readers to understand Taiwan’s carbon inventory regulations and observe the carbon emission disclosure of Taiwanese companies and the status of verification by third-party organizations.

Table of Contents

The predecessor of the current “Climate Change Response Act” is the “GHGs Emission Reduction and Management Act” (GERMA), announced and implemented in July 2015.

By 2016, the announcement required the power generation, steel, petroleum refining, cement, semiconductor, and thin film transistor liquid crystal display industry, which is energy-consuming heavily or other industries with an annual emission of more than 25,000 metric tons of carbon dioxide equivalent (metric tons CO2e), must complete the previous year’s emissions by the end of August each year. And the verification of greenhouse gas inventory should be completed every three years.

The inspection agency for greenhouse gas inventory must be internationally recognized or its domestic branch and should obtain a certification certificate issued by a qualified certification agency. Only one competent certification body in my country (Taiwan Accreditation Foundation, TAF) handles the certification and tracing of inspection bodies. There are nine other qualified inspection bodies.

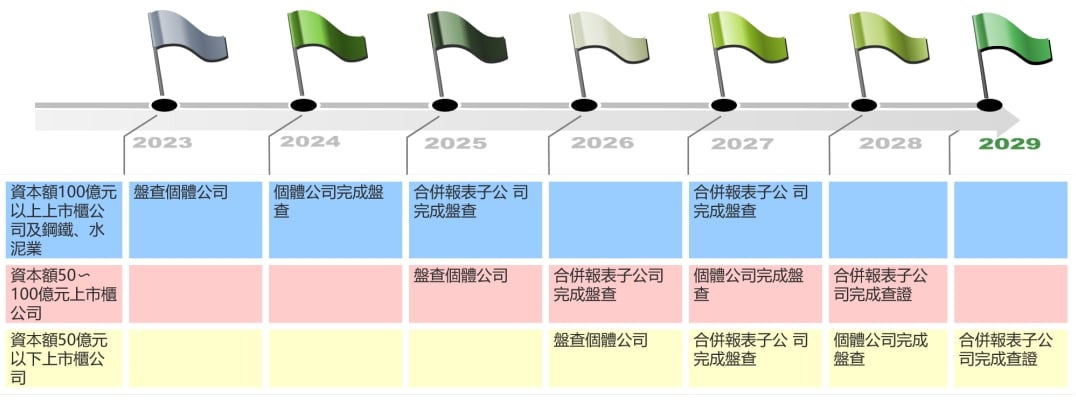

In March this year, the Financial Supervisory Commission officially promoted the “Sustainable Development Roadmap” and set a schedule to disclose listed overseas companies’ greenhouse gas inventory information, as shown in the figure below.

According to TEJ’s statistics, 165 listed companies matched CFV in 2013 (119 listed companies with a capital of more than 10 billion NTD and 46 companies in the steel and cement industries), of which 24 companies still need to conduct CFV. Thirty-seven companies have been checked but still need to complete the verification.

In addition to listed counter companies, according to statistics from the Ministry of Economic Affairs, there are about 100,000 small and medium-sized enterprises engaged in manufacturing in Taiwan, which will also face the requirements of domestic and foreign supply chains for CFV. For this, the Environmental Protection Administration (EPA) released the “Greenhouse Gases Guide” to encourage small and medium-sized enterprises to refer to the guidelines and calculate their greenhouse gas emissions every year according to their situation and carbon emissions and the effectiveness of reduction plans. There is no particular mandatory for verification or otherwise.

Greenhouse gas emissions can get from the EPA’s “Mandatory Greenhouse Gas Reporting System” and the sustainability report issued by the company, which can also be found in the annual report of the shareholders’ meeting, the Market Observation Post Station (MOPS), etc.

TEJ’s “TESG Sustainability Solution” has completed the collection of carbon emissions data of 1,099 companies in 2021. According to the above, data sources are diverse, and the rules are inconsistent. TEJ tries its best to analyze the scope of investigation and disclosure of information from various sources and verify to determine the completeness of the final data set.

Taking 2021 as an example, we found multiple data issues:

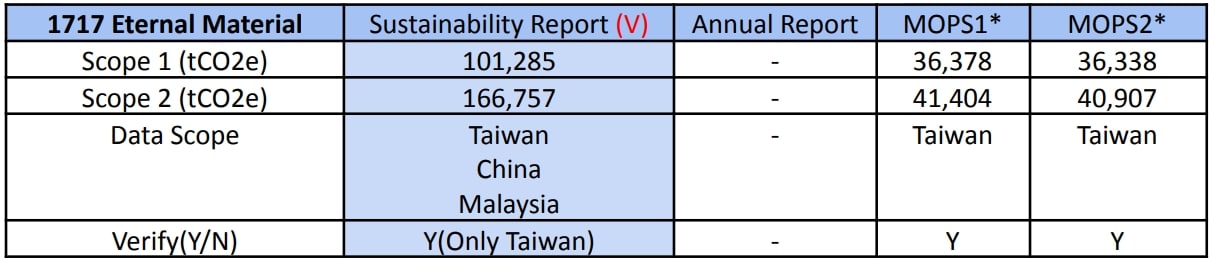

1717 Eternal Material’s 2021 annual report did not disclose carbon emission information, so compared with other data sources, it was found that the carbon emission amounts of the three references were inconsistent because the scope of disclosure was inconsistent. After TEJ comparison, the complete range of the sustainable report, together with MOPS head office data, sorts out the entire range of carbon emission data.

Table 1. Eternal Material’s 2021 Greenhouse Gas Disclosure Status

Source: TEJ database.

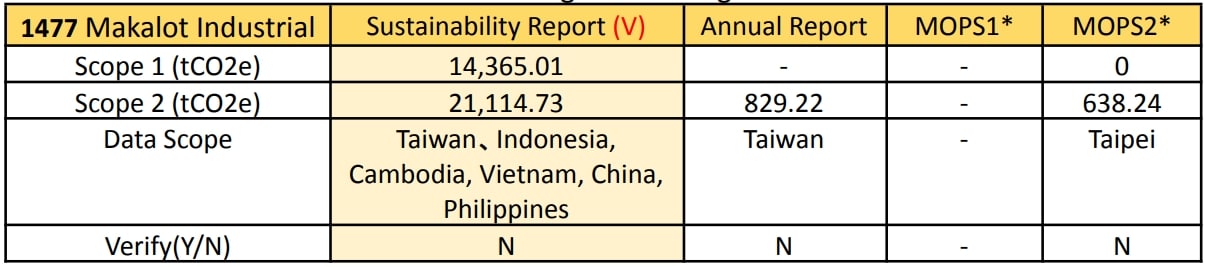

1477 Makalot Industrial’s 2021 Sustainability Report fully disclosed Scope 1 and Scope 2 greenhouse gas emissions, and the scope of the disclosure includes Taiwan and overseas subsidiaries. TEJ uses the sustainability report as the last included information compared to other sources.

Table 2. 1477 Makalot Industrial’s 2021 greenhouse gas disclosure status

Source: TEJ database.

2634 Aerospace Industrial Development Corporation (AIDC)’s 2021 carbon emission data has different figures from different sources. After comparison, it is confirmed that the MOPS2 data has been verified by a third-party verification agency SGS, which is more credible than other data sources.

Table 3. AIDC’s 2021 disclosure status of various greenhouse gas data sources

Source: TEJ database.

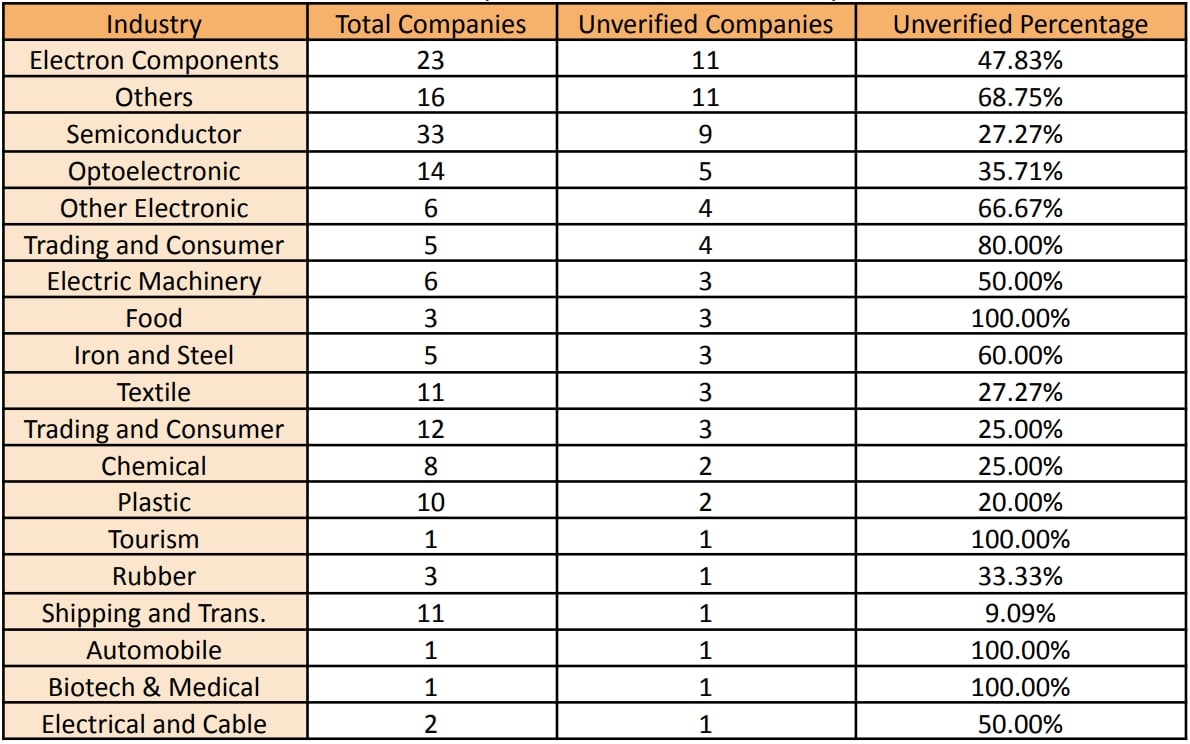

Among the top 200 listed companies with carbon emissions, there are a total of 69 unverified companies. The top five industries with the most significant number of unverified companies are electronic components, others, semiconductors, optoelectronics, and other electronics industries.

Table 4. Unverified status of the top 200 carbon emission companies in TWSE 2021

The current relevant laws and regulations are still in the promotion stage, and the methods of checking and disclosing the greenhouse gas emissions of each enterprise are different. Therefore, TEJ believes that whether a third-party organization verifies the greenhouse gas inventory data is more critical. In addition to ensuring the greenhouse gas emission data of enterprises, In addition to quality and correctness of the data, it is also the basis for the company’s carbon reduction goals.

TESG sustainability solution, with TEJ’s powerful information collection capabilities, sorts out ESG information from multiple sources, removes the superfluous and preserves the essence.

Introduces the rating framework officially authorized by the international ESG standard SASB, establishes more than 40 ESG databases, and solves the implementation of responsible finance ESG collection pain points at work.

TEJ also regularly reviews the scope of ESG information and the accuracy of the ESG indicator model following the requirements of Taiwan and international ESG standards, allowing you to save time and effort and test ESG more accurately.

TEJ also provides data solutions for TCFD reports, assisting the financial industry in using the PCAF calculation method to organize and calculate the carbon emission data of the six categories of assets, set carbon reduction goals and scenario analysis, and complete the policy formulation of transformation risks and opportunities. In terms of physical risks, assist in inspecting and assessing disaster risks and then completing the TCFD report.

From Green Finance 1.0 to Green Finance 3.0, Taiwan is in line with international standards, gradually expanding the scope and in-depth details to strengthen enterprises’ ESG implementation and disclosure scope. From the perspective of capital providers, the financial industry can better communicate with investment and financing enterprises. Communicate and collaborate on ESG implementation.