Table of Contents

The opacity of Chinese corporate information and the inflated ratings in the bond market have always been the biggest pain in our cooperation with Chinese corporations. From the complexity of data collection to the credibility of data analysis, data limitations of all sizes affect our ability to assess the credit risk of corporations from publicly available information.

In 2013, TEJ published China Corporate Credit Quantitative Model, CCRQM, a credit risk rating system for evaluating China Corporate’s credit. CCRQM is based on quantitative models and data generated from financial reports. These ratings are updated every half-year.

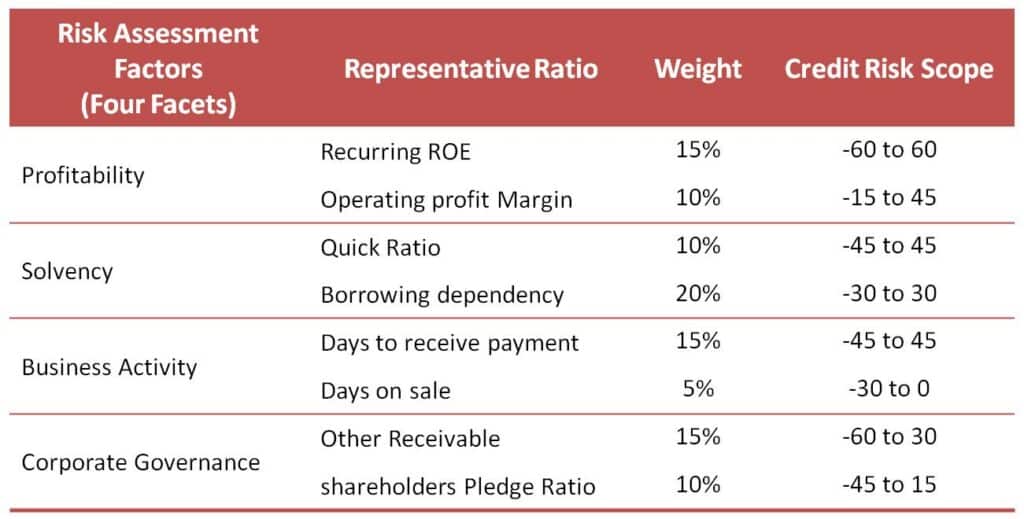

TEJ adopts the data from financial reports to create logistic regression and expert judgment to decide the best combination of variables and variable weights in models. In this way, the credit scoring model of Scorecard generates user-friendly credit scores.

The model primarily utilizes publicly available financial statement data, applying logistic stepwise regression combined with expert judgment to select the optimal variable combinations and their respective weights.

These are then converted into user-friendly credit scores using a scorecard credit scoring model.

Start Managing Corporate Credit Risk of Investment Portfolio

Evaluate Credit Risk More Efficiently Today!

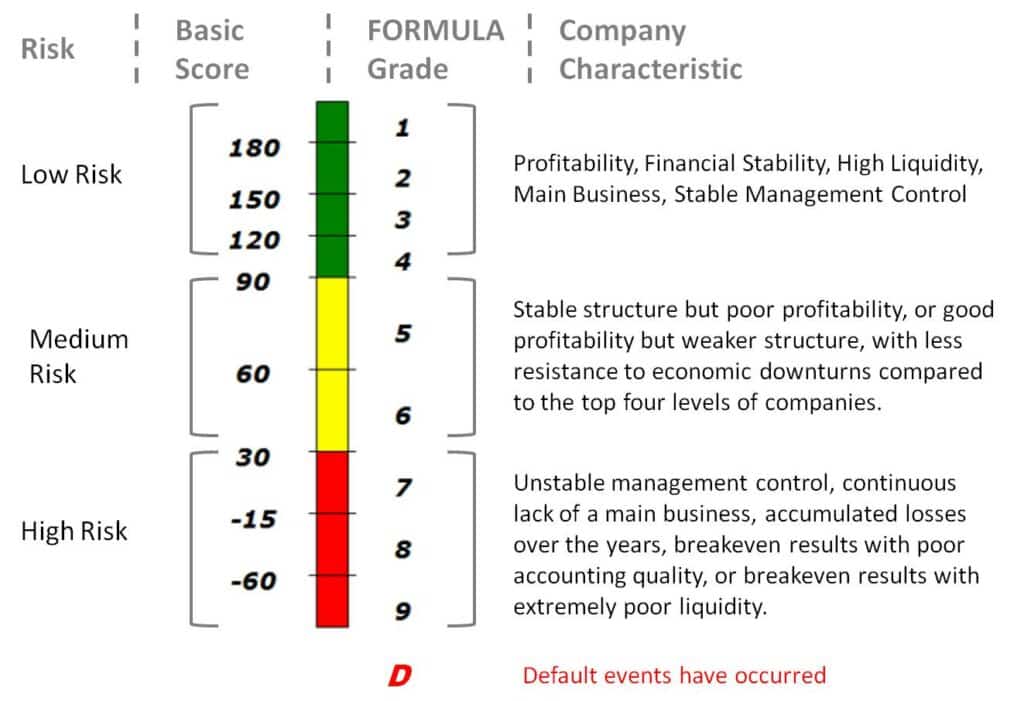

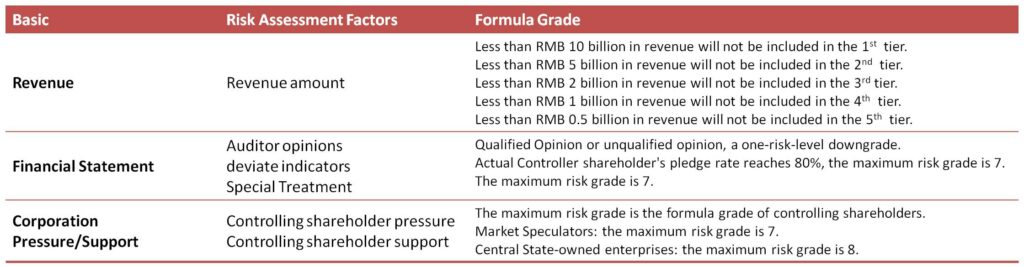

Adjustment of the formula grade to the basic grade by using financial disclosure and group as the threshold limit.

The average default risk differentiation ability of 90.24% over the last 10 years (2014~2023) indicates that the quantitative model (threshold level) has a high differentiation ability regardless of the modeling period.

Observing the status of quantitative model (basic grade) rating through the shift matrix, the average 1-year maintenance rate from 2005-2023 is about 40-60%, and the volatility of low risk is small compared to the high risk. Through the expert judgment rating, it can effectively improve the ability and stability of the long-term investment and credit index.

Facing the special characteristics of Chinese enterprises: asset restructuring, shell-listing, financial window-dressing, and the outbreak of cash fraud cases in recent years, TEJ have been reflecting on and revising CCRQM‘s methodology. We continue to provide solutions for you to enhance your early warning capability!