Table of Contents

The event study is one of the important tools for quantitative investment and is often used to study the impact of events on the stock price. It explores whether stock prices regularly rise or fall after an event is announced or occurs. The efficiency of the Taiwan stock market is lower than that of the European and American markets, and stock prices often underreact to events. Quantitative strategy developers can use the event study method to verify the information of various corporate events and explore potential investment opportunities.

This article adopts the TEJ Corporate Event Database and applies the event study to explore the impact of the announcement of different corporate events, such as seasoned equity offerings, private placements, insider declared transfers, etc., on the stock price and to test whether the announcement of the event has connotations.

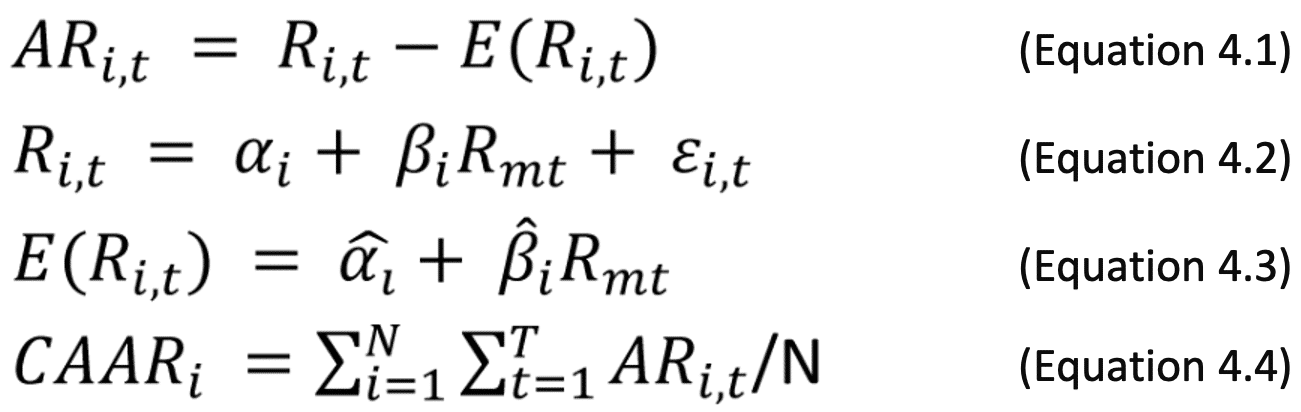

The event study aims to test whether the stock will produce abnormal returns during the period after the event occurs, and the general event period is 20 days. The abnormal rate of return is calculated by subtracting the expected rate of return on individual stocks from the rate of return on individual stocks (such as Equation 4.1), where the expected return E(Ri,t) of the stock is estimated by using the single-factor model (such as Equations 4.2, 4.3), and the estimation period is generally 200 days. Finally, the cumulative average abnormal return rate during the event period (as in Equation 4.4) was calculated and tested for significance with the t-test.

Ri,t is the individual stock return, E(Ri,t) is the individual stock expected return, ARi,t is the abnormal return, Rmt is the market portfolio return, CAARi is the cumulative average abnormal return, N is the number of samples, and T is the event period.

Under the information asymmetry, the announcement of the company’s activities and events implies the management’s views on future operations, and market investors will use this as the basis for buying and selling decisions. For instance, the company uses seasoned equity offering (SEO) to increase capital to repay debt or improve its capital structure. Investors will take this signal as the current stock price being overvalued, so when the event is announced, investors will tend to sell the stock and the stock price will react negatively. Alternatively, the company invests a positive net present value (NPV) project through private placement, which can increase the company’s future earnings. At this time, when the event is announced, investors will tend to buy stocks and the stock price will react positively.

The announcement effect of the event will also be affected by different factors. For example, the declaration and transfer of shares held by insiders may convey negative information within the company, but it will also be affected by the different purposes of the declaration and transfer, which will affect the announcement effect.Based on the above, this article will take SEO, private placement and insider declared transfer as examples to test the connotation of event announcements and explore whether stock prices will have abnormal returns when events are announced.

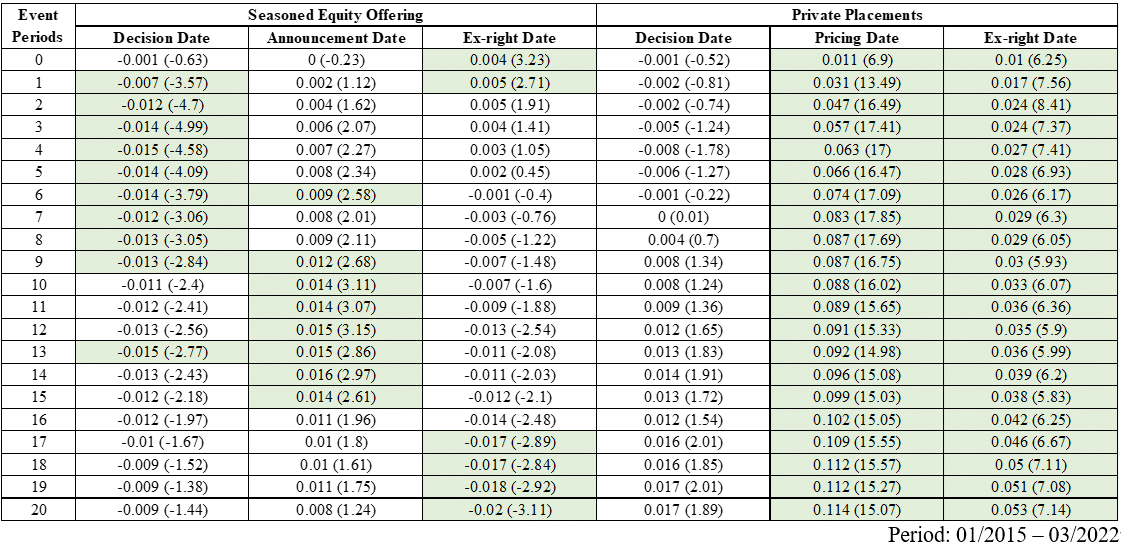

The analysis was conducted in the period of January 1, 2015, to March 30, 2022, with the public companies that used SEO or private placement to raise capital as samples. The overall number of companies that raised capital by SEO was 368, and the number of samples was 521; the number of firms that participated in the private placement was 244, and the number of samples was 528. The source of the information is the TEJ Corporate Events Database. Therefore, this article will examine the announcement date of different events and the impact of their announcement on the stock price.

Table 1 summarizes the cumulative mean abnormal returns for stocks and corresponding t-values in the 20 days after the dates SEO was decided at the shareholders meeting, the declaration date of SEO, the ex-rights date of SEO, the date private placement was decided, the private placement pricing date, and the private placement ex-rights date. The time horizon is January 2015 to March 2022.

Table 1. Cumulative abnormal return 20 days after the announcement of SEO and private placement

The results of the announcement of SEO show that there will be a short-term negative abnormal return rate in the future after SEO is decided in the shareholders’ meeting, and the cumulative 9-day average abnormal return rate is -1.3% (t statistic = -2.84). The cumulative average abnormal return 15 days after the announcement is 1.4% (t statistic = 2.61), and the cumulative average abnormal return 20 days after the ex-rights date is -2% (t statistic = -3.11). The announcement of the SEO in the shareholders’ meeting implies that the current stock price is overvalued, and the issuance of new shares after the SEO and ex-rights may damage the original shareholders’ rights and cause investors to sell the stock, which will have a significant negative impact on the stock price.

The results of the announcement of private placement show that the cumulative abnormal return 20 days after the board of directors made the decision is 1.7% (t statistic = 1.89). The cumulative average abnormal return on the private placement pricing date and 20 days after the ex-rights date was significantly positive, 11.4% (t statistic = 15.07) and 5.3% (t statistic = 7.14), respectively. It shows that private placement not only implies that the company has obtained a better investment plan but also restricted the liquidity of the stock and ensured that core shareholders hold shares so that the announcement of private placement has a positive impact on the stock price.

Stay up to date with the latest events and actions of companies.

Grasp the timely data and market insights today!

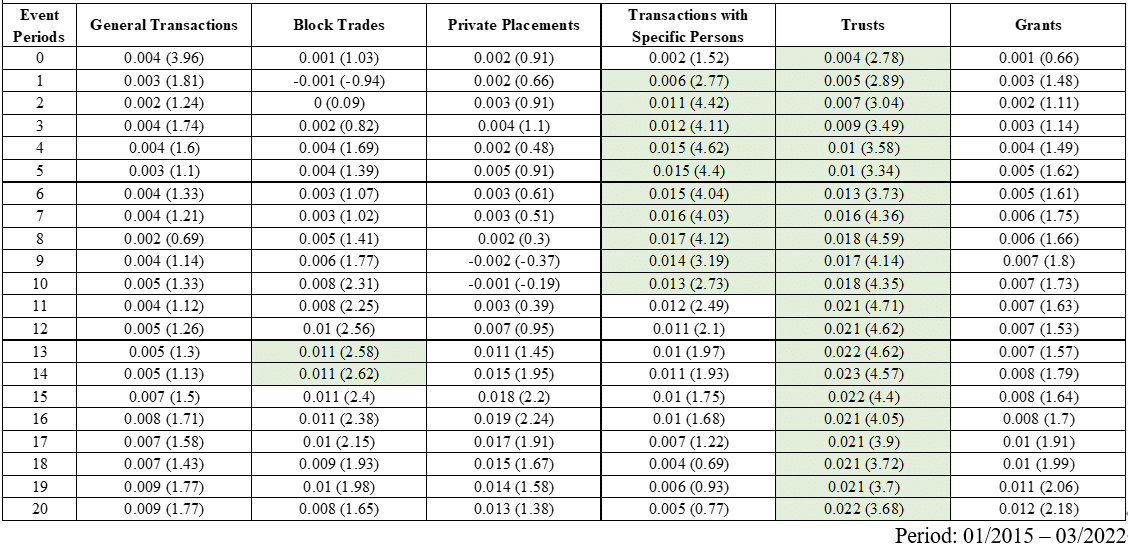

Next, we also take all listed companies from January 1, 2015, to March 30, 2022, as a sample to examine the effect of insiders’ declaration of shareholding transfer. The sample is classified according to the purpose of shareholding transfer. After classification, the number of households and the number of samples are arranged as shown in Table 2. Most of the purposes of transfer are to grant, and there are 3862 samples. This is followed by 2,781 in general transactions, 899 in transactions with specific persons, 817 in trusts, 595 in block trades, and 253 in private placements.

Insider declaration of transfer conveys internal information of the company, and depending on the purpose of declaring the transfer, the effects of the declaration are also different. Therefore, this section will be classified according to the purpose of the insider shareholding transfer and explore the impact on the abnormal return of stock when the purpose of the insider’s shareholding declaration and transfer are different.

Table 2. Summary of the Transfer of Shares by Insiders

| General Transactions | Block Trades | Private Placements | Transactions with Specific Persons | Trusts | Grants | |

|---|---|---|---|---|---|---|

| Number of Companies | 697 | 292 | 91 | 509 | 354 | 824 |

| Samples | 2781 | 595 | 253 | 899 | 817 | 3862 |

Table 3 below shows the cumulative average abnormal stock returns and corresponding t-values for the period from January 2015 to March 2022, categorized by the purpose of the reported transfers of insider holdings into six categories: general transaction, block trades, private placement, transactions with a specific person, trust, and grant.

Under 1% level of significance, the cumulative average abnormal return and t-statistics are general transactions of 0.9% (t-statistic = 1.77), block trades of 0.8% (t-statistic = 1.65), private placements of 1.3% (t-statistic = 1.38), gifts of 1.2% (t-statistic = 2.18), and the cumulative abnormal return rate is not significantly positive. However, in the short-term period of 10-day, the specific person shows a significantly positive abnormal return rate (1.3%, t-statistic = 2.73), indicating that the transfer of shares by an insider to a specific person may imply better investment opportunities or bringing in a new management team to improve performance. For the purpose of shareholding transfer, the announcement of trust has the most significant effect (2.2%, t-statistic = 3.68), which shows that when the company insiders undertake the trust based on tax planning, it indicates that the stock price is undervalued and the future surge is likely to be huge.

Table 3. Cumulative abnormal return of 20 days after the announcement of shareholding transfer by insiders

This article examines the announcement effects of seasoned equity offerings (SEOs), private placements, and insider declarations of shareholding transfer on stock returns; the following are three highlights:

Through event studies, we can explore the impact on stock price volatility after the announcements of events. In this article, we use announcements of corporate events, such as seasoned equity offerings, private placements, insider declared transfers, etc., to understand the impact of announcements on abnormal stock price returns. Quantitative analysts may examine effectively by utilizing a variety of corporate events. Accurate and effective quantitative results depend on reliable and comprehensive data, and TEJ Event-driven Data was established for this purpose.

TEJ Event-driven Data is a valuable resource that provides real-time market news, including market fluctuations and opportunities. This feature allows users to stay updated with the latest news and swiftly build investment strategies based on the most current information. The database contains the event announcement to the completion of the incident; with the spirit of point-in-time, TEJ retains the date and process of each event stage. We update timely corporate events such as shareholders’ meeting dates, related capital change events, ex-rights of dividends, etc. Investors can even utilize the consolidated data on the announcement date to avoid generating forward-looking bias in analysis!