Table of Contents

In the previous article, we introduced the China Evergrande’s bond default case. This case started a series of explosions in China’s real estate company’s debt default. According to statistics, in the first three quarters of 2021, the cumulative number of defaulted bonds of Chinese real estate companies reached 39, an increase of 25 over the same period in 2020, and the cumulative defaulted amount reached 46.75 billion, an increase of 159% over 2020.

In addition to expansion and financial operations, the reasons for the default of real estate companies can also be discussed from the perspective of minority interest (the equity held by the joint venture party): In order to reduce their own development costs and the initial capital pressure, Chinese real estate companies will often look for other shareholders to establish joint venture project companies and cooperate to obtain land. When the development is over, the real estate companies will repurchase their equity from the joint venture shareholders. If the joint venture shareholders do not want to bear the sales risk of the subsequent construction project, they usually require the real estate company to repurchase the equity before the construction project is sold.

Although cooperative development allows Chinese real estate companies to save early development costs, they still need to repurchase the equity as agreed, which is equivalent to delaying payment for the saved costs. After all, there is no cost saving effect, and this action also increases a lot of financial burdens. When the money that Chinese real estate companies receive from joint venture shareholders is not enough to cover the repurchase funds, the flow of funds may have problems.

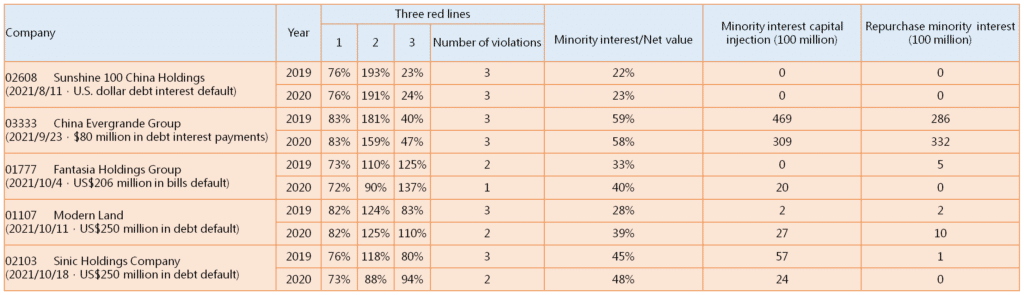

As of October 2021, 5 Hong Kong listed real estate companies have defaulted. Except for Fantasia Holdings Group, the remaining 4 companies have violated 2 or 3 red lines. In terms of minority interest proportion , with the exception of Sunshine 100 China Holdings, the remaining minority interest proportion accounts for more than 40% of the net value. Table 1 shows that the defaulting company has either violated three red lines or has a high minority interest ratio.

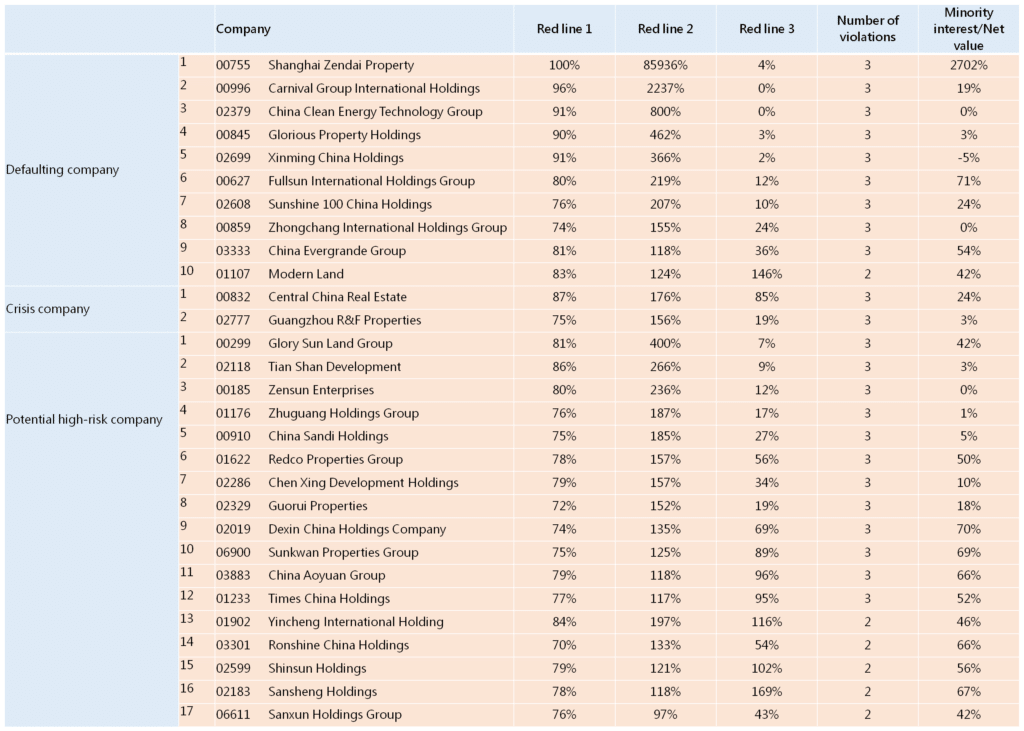

Table 2 summarizes the list of companies that have volated two or three red lines in the 2021 semi-annual report and have a minority interest ratio of more than 40% of their net value. According to the search criteria, a total of 29 companies were found, of which 10 companies have defaulted. Central China Real Estate and R&F Properties have respectively sought assistance from the Henan government and the controlling shareholder Country Garden Holdings. Another 17 companies have potential default risks, many companies’ bond yields have increased sharply, or bond prices have plummeted.

In the short term, the Chinese government will still use three red lines to monitor the risks of real estate companies. Therefore, we try to identify companies with potential crises in the future by evaluating the three red lines and the proportion of minority interest information. This reminds readers to pay attention to the future debt repayment status of these companies.

How can this series of conditions be warned before 2020 or even earlier? TEJ’s CCRQM provides a differentiated credit risk quantitative model, reasonably assesses the credit risk of Chinese enterprises, and assists in managing the overall credit default risk of lending or investment!

CCRQM have been modeled since 2009. This pure quantitative model of credit risk indicators has undergone more than 10 years of market testing, and the average credit rating ROC (Receiver Operating Characteristic) indicator is close to 90%. Especially in this wave of landmine lists of Chinese real estate companies, most companies were included in the high-risk list at least a year ago to warn the market in advance.

Looking back since 2020, in the face of severe epidemics, rising debt risks, and the continued impact of the China–United States trade war, the high-risk grades in CCRQM accounted for the proportion of companies rated in the current year, down from 35.27% to 32.70% in the previous year, but still remained at a high-end, reflecting the high credit risk of China’s overall enterprises.

In 2020, there are 32 listed companies in China that have a crisis as defined by CCRQM. Compared with 37 companies in the previous year, the number of crisis cases has dropped by 5. Among them, there is a crisis company Guangdong Mingzhu (600382) failed to be classified as a high-risk level in a year before the crisis. Compared with the two mistakes made in the previous year, the ROC (Receiver Operating Characteristic) indicator rose slightly to 93.36%, which is highly recognized.

After the completion of the CCRQM model in 2008, ROC was only 85.38% affected by the financial tsunami in 2009, and only 88.76% affected by false financial reports and controlling shareholders in 2014. The rest of the year is higher than that during the modeling period. (2005-2008).

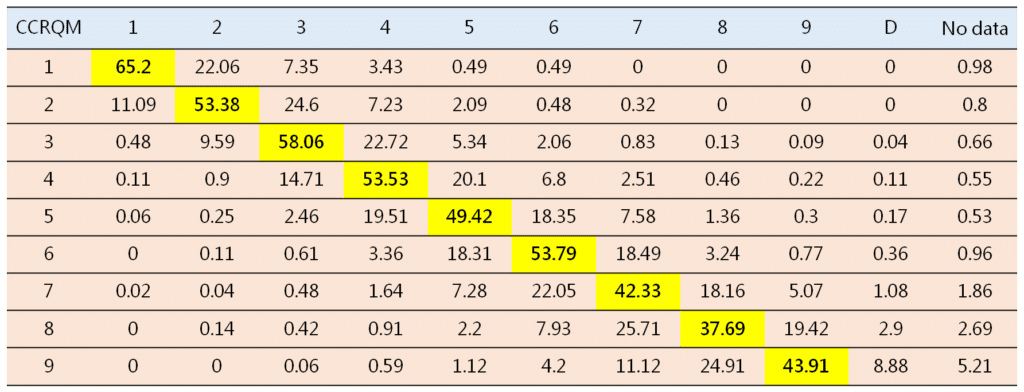

For users, they can examine the status of credit rating adjustments through the Transition Matrix. As shown in Table 4, the average one-year maintenance rate from 2005 to 2020 is about 40% to 60%, which is similar to the general statistical model of Taiwan listed companies. It shows that the basic level still has a considerable degree of stability. Among them, the volatility of low-level credit risk is smaller than that of high- level credit risk.

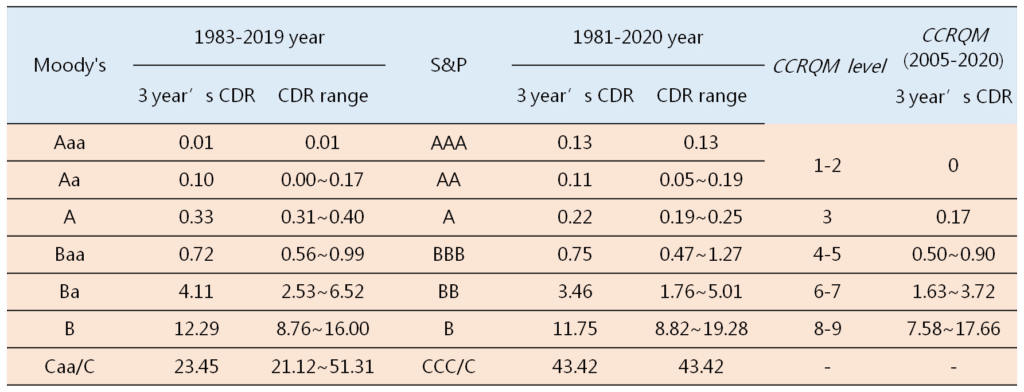

The common language of the credit rating market is the rating of large international credit rating agencies. CCRQM is compared with international large-scale credit rating agencies S&P and Moody’s, and requires the use of the 10-period average 3-year cumulative crisis probability and the benchmark external credit rating agency’s long-term average 3-year cumulative crisis probability as a reference CDR to control.

According to the CCRQM data from 2005 to 2020, there has been an average 3-year cumulative crisis probability of more than 10 periods, and the comparison results have certain reference value.

Overall, the validity verification of the CCRQM in 2020 has completed the test of the rating results, and the ROC is as high as 93.36%, which is a usable model. Crisis companies were classified as high-risk by CCRQM one year before the accident, which has early warning capabilities. In terms of stability, the grade maintenance rate is about 40-60%, which is similar to the general statistical model of Taiwan listed companies about 4-50%, showing that the CCRQM has a certain degree of stability.

TEJ provides CCRQM on the issue of Chinese corporate credit risk, daily Shanghai and Shenzhen market news, to help users face the tremendous Chinese market, effectively distinguish the degree of risk and track the latest information of the company. Unlisted Chinese companies can also be inquired through the CCRQM online rating system. By entering corporate capital data and financial report information, you can immediately require credit risk analysis results. It is the best tool for investment or credit evaluation!

For more complete solution to China’s corporate credit risk, please refer to TEJ CCRQM.