After the robust growth of the economy last year, under the pressure of increasing inflation, the exit of QE and the hike in interest rates have led to a rapid reversal of the global market condition from loose to tight this year. In particular, the economic outlook of the United States and China this year has deteriorated significantly, and the technology sector has also undergone major changes. The test for Taiwan’s economy this year should not be underestimated.

Table of Contents

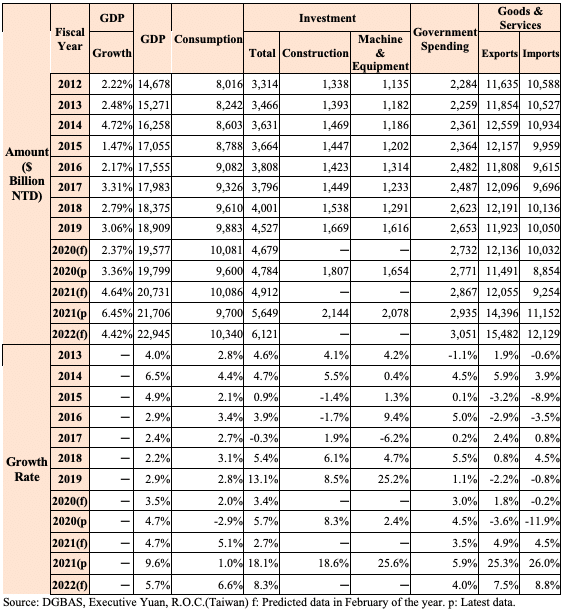

In the past two years, under the raging pandemic, the global economy has been smashed hard, but Taiwan’s economic performance exceeded expectations and was quite outstanding. In 2020, the growth rate of Taiwan economy was 3.36%, which was the best result since 2015. In 2021, it reached a high of 6.45%, and it was the best economic performance in the past 11 years.

Table 1. Comparison of the main components of Taiwan’s GDP in the past ten years

The main reasons for the outstanding performance of the economy last year are:

Overall, exports and investment were the main drivers of Taiwan’s strong economic growth last year. Affected by COVID-19, consumption performance was weak. Even though the Quintuple Stimulus Vouchers were issued to stimulate consumption last year, the annual consumption growth was only 1%, which was still much lower than the 5.1% estimated in February last year. With the excellent economic performance of the previous two years, can Taiwan’s economy continue to achieve good results this year?

The biggest changes are in the global financial environment this year. Due to the impact of the pandemic, major countries have endorsed a loose monetary policy in the past two years. The flood of fund has accelerated the pace of inflation although impact of the pandemic on the economy were alleviated. In particular, the unsmooth production and sales caused by the pandemic led to repeated orders and disruption of the supply chain, which aggravated the pressure of inflation. In addition, the excess demand caused by expansionary monetary policy further accelerated the rise in inflation.

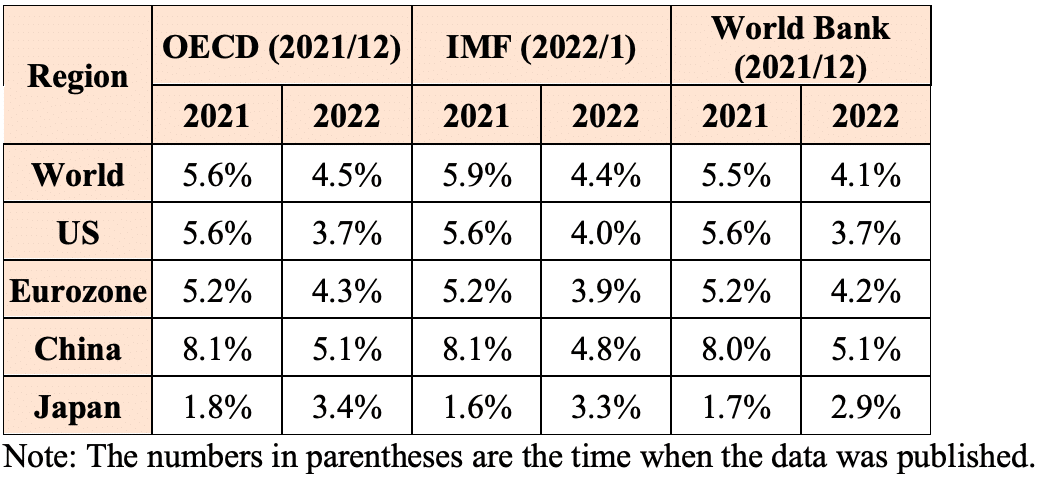

Therefore, the economic forecasts of various institutions this year may not be optimistic. And in the situation when the global economy has deteriorated, it is also quite unfavorable for Taiwan’s economic growth this year.

Table 2. Economic forecast for this year

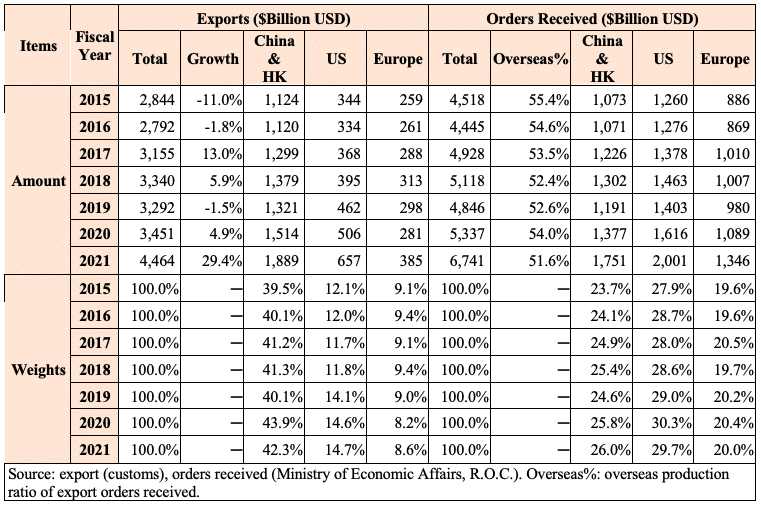

Taiwan’s economy is quite dependent on foreign countries, and the rise and fall of exports is often a key factor in determining the strength of economic growth. As for Taiwan’s main export markets, in terms of export value, China and Hong Kong accounted for about 42.3% of the total export last year and were the most important export markets. The market followed by was the United States at 14.7% (please refer to Table 4). However, due to the serious relocation of industries, overseas production reached more than 50% of the total production. If it is analyzed from the perspective of receiving orders, the US market accounted for 29.7% of the global market last year, making it the most important market. And the market size of China was about 26%, which was the second largest market. Overall, the United States and China can be regarded as Taiwan’s two most important export markets, and their economy exert a great impact on Taiwan’s exports.

Table 3. Statistics on Taiwan’s exports and orders received in the past seven years

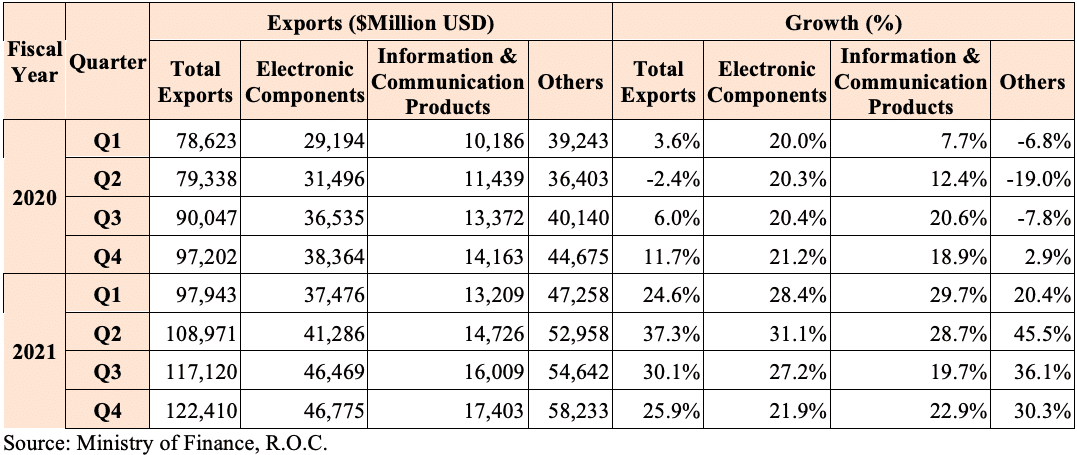

Whether the high demand for IC could be sustained will have a significant impact on Taiwan’s economy this year. The economic outlook is not optimistic of the two major export markets, the United States and China, which is bad news for Taiwan’s export this year. However, Taiwan’s export competitiveness lies in the technology sector. Will there be any optimism in the outlook for the technology industry this year?During the pandemic, the global economy has been hit a lot, especially the year of 2020. However, due to the rise of the stay-at-home economy and the effect of the transfer of orders brought about by the US-China trade war, the exports of electronic components (mainly IC, accounting for about 90%) and information and communication products maintained strong growth (please refer to Table 7). The impact of the decline of traditional industry exports has been mitigated. Therefore, exports could grow at a rate of 4.9% in 2020. Last year, the stay-at-home economy continued to boom, driving the export of electronic products to grow significantly. While traditional industries benefited from a low base period and demand returned to normal, exports also grew strongly. The combined growth of technology and traditional industries pushed exports to record at a strong growth of 29.4% last year.

Table 4. Analysis of Taiwan’s export structure

Due to the need for distance teaching during the pandemic, Chromebooks, which mainly focus on education projects, have risen strongly, driving the overall PC sales in 2020 to a strong growth of 13.1%. On top of that, the increase in time at home and the large-scale subsidies in the United States drove the US TV market to double-digit growth for four consecutive quarters since the second quarter of the previous year. How to live with the virus has gradually become a new trend this year. With the restart of the economy, the stay-at-home economy is bound to decline. While the outlook of smart phone market is still gloomy. China is the world’s largest mobile phone market, but China’s smartphone sales in the first two months of this year were only 46.92 million, which was a sharp decline of 23% compared to the same period last year. Moreover, the recent outbreak of the Russian-Ukrainian war and the resurgence of the Covid cases in China also added fuel to the fire. Therefore, TrendForce has lowered its global smartphone sales prediction in mid-March.

In addition, the booming LCD industry has deteriorated rapidly as the display panel market fell sharply since the third quarter of last year, and almost all its gains have been wiped out.

In the retail market of electronic products, mobile phones and PCs are the two most important products. However, the outlook for the electronics industry this year is not optimistic, which is not conducive to the export of the electronics industry this year. In February this year, the Directorate-General of Budget, Accounting and Statistics (DGBAS) estimated that this year’s merchandise export target is US$489.64 billion, an annual growth rate of about 9.7%. In the first quarter, the export value of 120.93 billion USD also successfully exceeded the first-quarter export target of 115.81 billion USD, which was not bad. However, with the outbreak of the Russian-Ukrainian war, China’s lockdown and other uncertainty, not to mention the wave of cutting orders by the electronics industry, will the export situation change after the second quarter?

Taiwan’s semiconductor industry, however, has strong competitiveness. So far, the IC boom is still very hot, which is a considerable boost to Taiwan’s economic growth this year. Taking exports in March this year as an example, the export value of integrated circuits was as high as 16.79 billion USD, accounting for 92% of the total export value of electronic components and 38.6% of the total export value. Therefore, if the IC boom can continue, it will be of great help to the achievement of the export target. This year, IC factories will still invest heavily (for example, TSMC’s capital expenditure was about US$30 billion last year, and this year it will grow significantly to US$40-44 billion), which is also expected by DGBAS for the 8.3% growth in fixed capital investment this year. It is critical that whether the target of 8.3% growth could be achieved.

Therefore, this year’s IC demand has become the most critical factor in determining whether the economy outlook will be bullish or bearish. If the IC boom this year can keep on, then Taiwan’s economic growth this year will not be too bad, and there is hope for a 4% of growth in total GDP. On the contrary, if the IC demand changes, the export performance may be affected. If the investment of IC industry players shrinks, this year’s “investment” will be greatly affected.

The possible change in the construction market is another uncertainty this year. With the government continuing to crack down on the housing market, the outlook of the housing market has become more unfavorable:

Amid the unfavorable housing market, according to a survey by a housing magazine, this year’s Northern Taiwan Metropolitan Area was originally expected to have a caseload of nearly 340 billion NTD, but the final actual figure was only 250-280 billion NTD. In addition, builders are also becoming more conservative in purchasing land. This year’s housing market is very likely to deteriorate, which is not conducive to the growth of “fixed capital investment.”

In February this year, DGBAS estimated that consumption will grow by 6.6% this year, which seems to be the most difficult to achieve at this moment. After all, the growth of consumption was below 5% even back before the pandemic, and one of the big uncertainty this year is the recurring Covid cases. Under this circumstance, how could we achieve the high growth target of 6.6%? Perhaps, just like in the previous two years, a high growth target was set, but the actual achievement rate was extremely low.

The latest forecast released by Cathay and National Taiwan University’s team on March 23 has revised this year’s GDP growth target from 3.9% down to 3.7%. Overall, the GDP growth rate estimated by DGBAS this year is 4.42%, which is quite difficult to achieve.