⏱️Read time: 4 minutes

Table of Contents

This article will introduce you to the SASB Standards. In August 2020, the Financial Supervisory Commission (FSC) launched the Corporate Governance 3.0 -Sustainable Development Roadmap to strengthen the sustainable competitiveness of enterprises. The Roadmap referred to disclosure requirements recommended by the Task Force on Climate-related Financial Disclosures (TCFD) and standards issued by the Sustainability Accounting Standards Board (SASB) to enhance sustainability reporting. It also required that listed and OTC companies with a paid-in capital of over 2 billion NTD prepare a CSR report starting from 2023 and a wider scope of third-party audits for the current CSR reports. In response, domestic listed and OTC companies must understand and respond to TCFD disclosure and SASB standards.

Established in San Francisco, USA in 2011, SASB is a global non-profit organization. SASB Standards, sustainable disclosure standards that combine both qualitative and quantitative attributes, help companies and investors worldwide reach a consensus on sustainability communication. Its purpose is to meet investors’ information needs and simultaneously help companies to demonstrate long-term performance and evaluate more comprehensively.

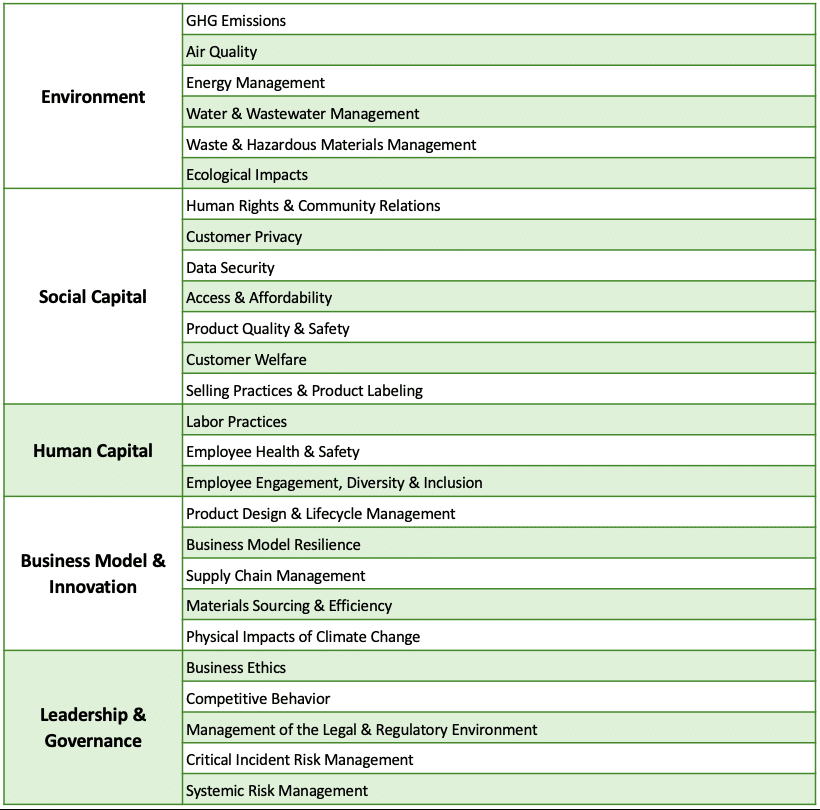

In November 2018, SASB announced the “Materiality Map” covering five major dimensions, 11 main industries (including 77 sub-industries), and 26 general ESG issues. The Materiality Map listed out ESG issues that may affect a company’s financial health and operating performance. The five dimensions include Environment, Social Capital, Human Capital, Business Model & Innovation, and Leadership & Governance.

Table 1. 5 Dimensions and 26 General ESG Issues of SASB

The current CSR reports of Taiwanese companies are almost all prepared under the GRI Standards regulated by the competent authorities. The GRI framework emphasizes the disclosure of complete stakeholders and material issues, as well as the corresponding management policy. Although there are industry-related standards in the GRI framework, the relevant indicators of the financial significance of the industry are not particularly emphasized. On the contrary, SASB standards provide consistent indicators and measurement methods to assess the financial impact of each industry based on the opportunities and risks of individual industries, which improves the comparability of information.

The biggest difference between SASB Standards and the GRI Standards is that SASB features:

Although SASB and GRI seem to be two different sets of standards, they both aim to disclose the sustainability of a company’s operations. GRI standards pay more attention to all-rounded disclosure, while the SASB standard focuses on financial-related disclosure. Both standards are of high importance. Therefore, CSR reports in Taiwan are currently prepared in a compatible way. Companies can disclose the two standards separately or can use a table to cross-reference the two standards. In July 2020, GRI and SASB jointly published “A Practical Guide to Sustainability Reporting Using GRI and SASB Standards.” This guide describes the method of jointly disclosing the GRI and SASB standards and can be summarized into four key points:

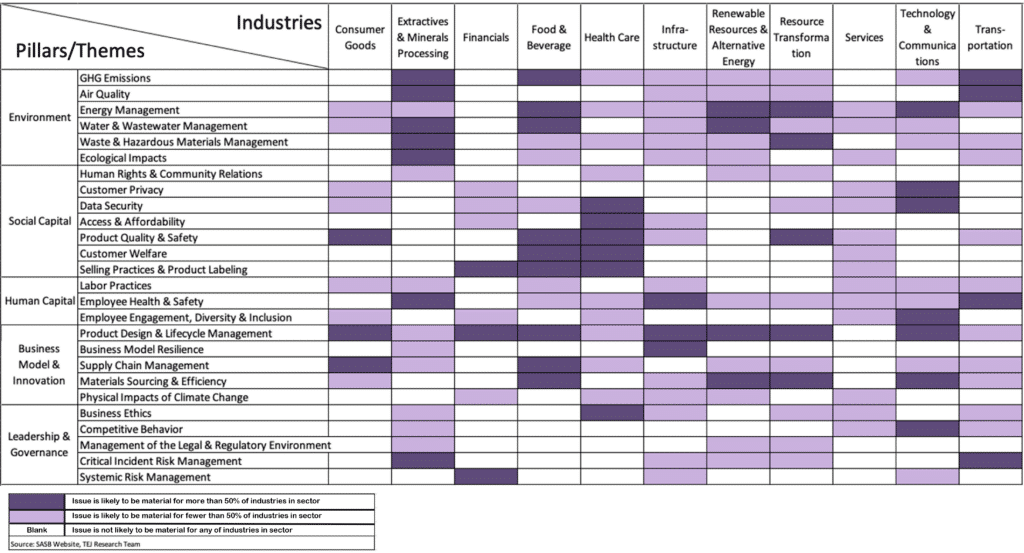

Table 2. Materiality Map

Currently, companies in Taiwan are still in the stage of introducing SASB Standards disclosure. There were only a minority of CSR reports adopting the standard in 2020, and the disclosure of each company was different. The nature of the industry in which companies operate is different, and the important issues they face in terms of operations and risks are also different. In addition to the fact that SASB’s industry classification may not be directly applicable to industries in Taiwan, the competent authority has not yet set practical guidelines for the application. If companies are allowed to determine their own applicable industry, it will further cause chaos in this matter.

Given the fact that the listed and OTC companies must provide CSR reports with reference to TCFD and SASB standards from 2023 onwards under Corporate Governance 3.0 -Sustainable Development Roadmap, the competent authorities, and relevant authorities must not only consider the revision of relevant regulations but also the issues raised in this article. More importantly, companies (not only listed) must recognize the importance of ESG management and complete disclosure and to be more actively and effectively collecting and disclosing relevant information for stakeholders. The sustainable development of the global economy, environment, and society must rely on active participation and cooperation between both private and public sectors.