In the past, Principles for Responsible Investment (PRI), Principles for Sustainable Insurance (PSI), Principles for Responsible Banking (PRB) and Equator Principles (EP) promoted by the United Nations for the financial industry emphasized that ESG-related factors should be considered in investment and financing positions.To be in line with the promotion of international sustainable finance, the Financial Supervisory Commission released the “Green Finance Action Plan 3.0” in September 2022. It proposed five major promotion directions and emphasized that financial institutions should understand carbon emission conditions related to not only themselves but their investment/ financing portfolios. Evaluating and identifying the possible impact of climate change on individual financial companies and the overall market to promote the development of sustainable finance.

From the above mentioned, how to measure the greenhouse gas emissions of financial institutions’ investment and financing portfolios or individual targets is regarding whether there exists consistency and comparability of the information that will be disclosed by various financial companies in the future. Therefore, the Partnership for Carbon Accounting and Financials (PCAF) released the “Global Greenhouse Gas Inventory and Reporting Guidelines for the Financial Industry” in November 2020 as a measurement guide. The introduction of PCAF’s carbon accounting methodology is helpful for financial companies to measure and disclose their own greenhouse gas emissions related to investment and financing activities, which can be consistent and comparable. As of September 2022, a total of 309 financial institutions around the world have joined and introduced the PCAF methodology, with a total asset value of 80 trillion US dollars. Financial institutions in Taiwan, such as CITIC / Yushan / O-Bank / KGI / Fubon / Cathay Pacific / First Bank have successively joined.

Table of Contents

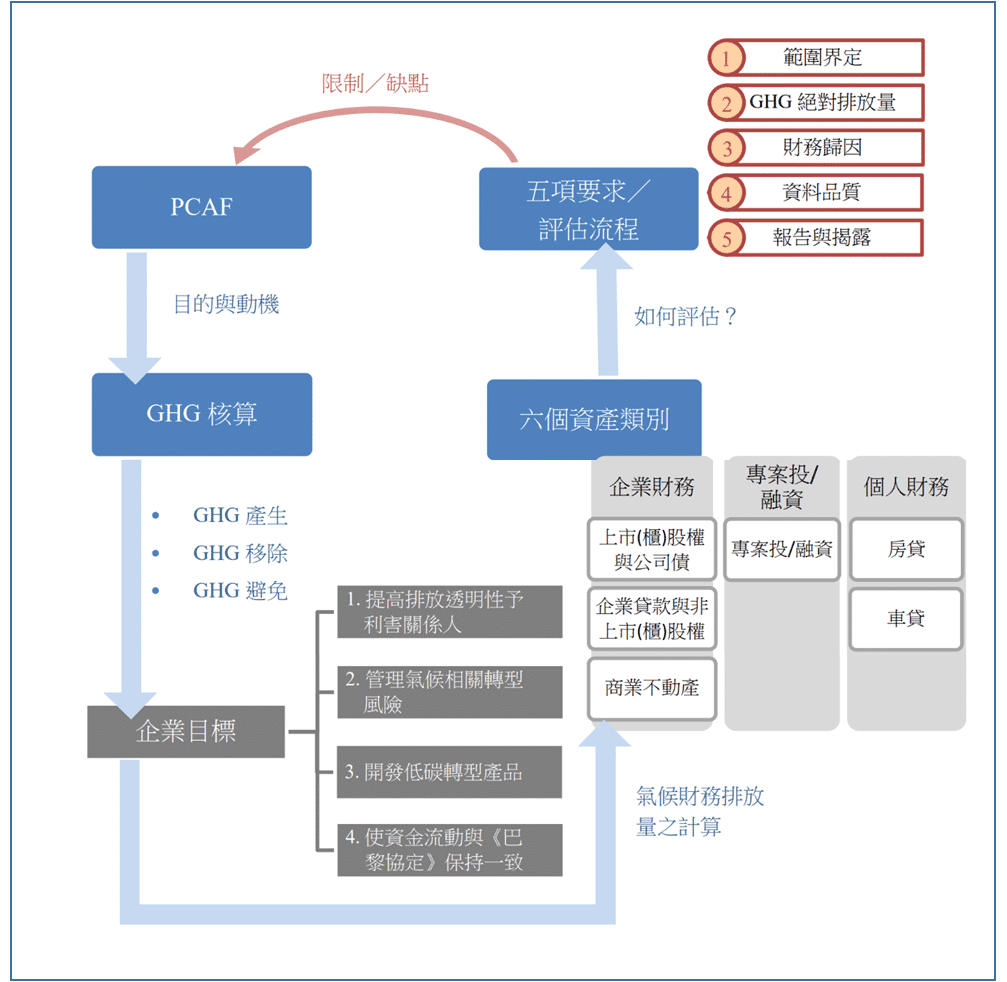

From the illustration of PCAF’s assessment framework, the main purpose of PCAF is to calculate the greenhouse gas emissions of investment and financing positions. It is necessary to understand the agreed standards for greenhouse gas inventory, and combine the disclosure of these standards to achieve constitutable goals for enterprises. Then, the point of view can be transferred from the whole enterprise to the financial industry, and be concluded in the main operation of financial institutions ─ Investment and financing business, which can be divided into asset classes. Finally, making an explanation for the differences in the calculation of GHG emissions for each asset class and the variables required for its methodology (five requirements and assessment process).

Figure: showing the PCAF assessment framework diagram

Among them, the assessment framework is worth focusing on the assessment and calculation of the six major assets; the calculation process used by financial institutions to calculate the GHG emissions of each asset category for investment and financing.

Firstly, financial institutions have to identify their own organizational boundaries and calculate the absolute greenhouse gas (GHG) emissions of the investment and financing target company. Then, obtaining the holding ratio (financial attribution) for the investment and financing positions to get the GHG emissions of them. Finally, conduct a data quality score evaluation based on the obtained data, identify the quality of the difference between the actual value and the estimated value, and announce the matters and explanations that need to be disclosed and reported. Finally, conduct a data quality score evaluation based on the obtained data, identify the quality difference between the actual value and the estimated value, and make announcement and explanation of the matters that need to be disclosed and reported.

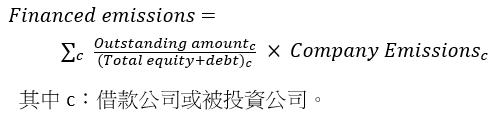

1. Financial attribution factor: Indicates the proportion of the debt or investment amount of their asset types to the overall equity and debt of the underlying asset.

2. GHG emissions calculation formula for investment and financing

3. The absolute amount of GHG carbon emissions of the company

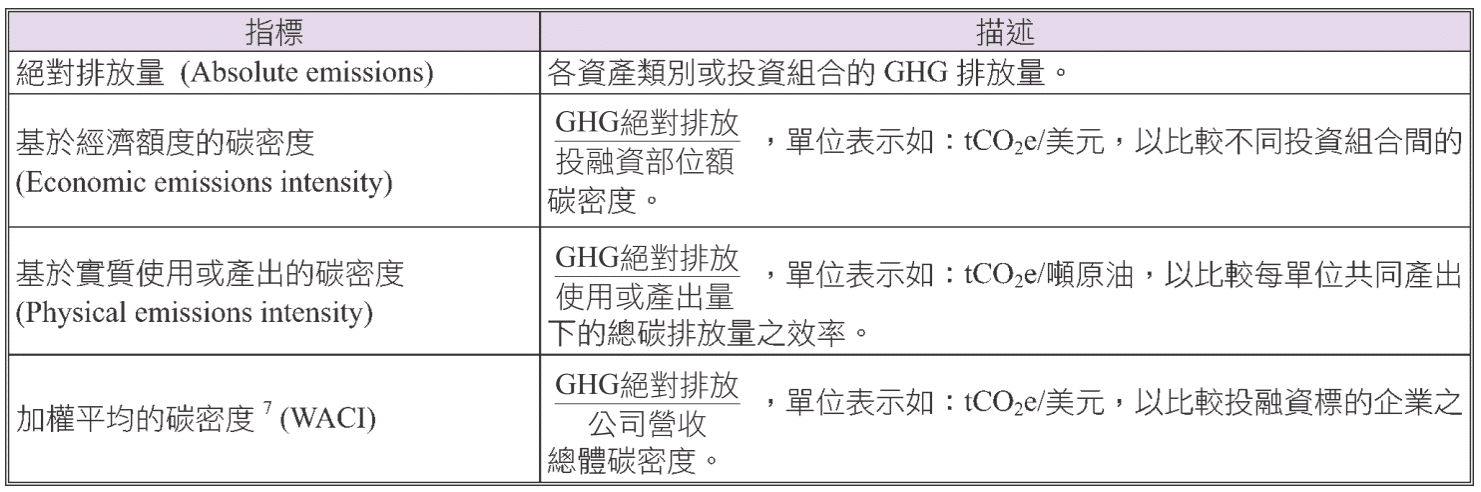

Some companies do not disclose their GHG emissions, and financial institutions can use GHG emission indicators for investment and financing.

4. Data quality

Not all investment and financing positions disclosed the required information to calculate GHG, because PCAF marks the data sources of each asset according to their data quality scores.If the obtained data is more accurate, its data quality score is lower (that is, the best data quality is 1 point; the worst data quality is 5 points).

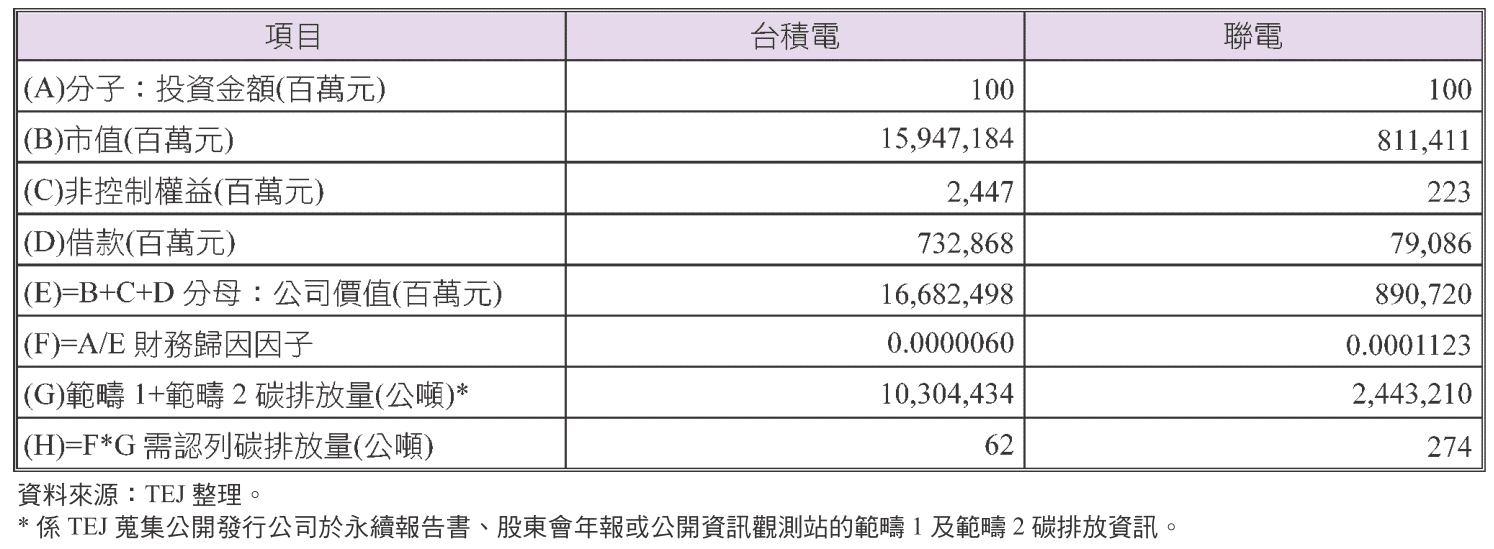

According to the above process, if financial institutions invest in companies with high carbon emissions, do they need to recognize higher carbon emissions? Let’s take TSMC and UMC as examples.

Assuming that financial institution A wants to invest NT$100 million in TSMC or UMC on December 31, 2021, it needs to calculate the difference in carbon emissions that will be recognized for investing in the two companies.First, compare the difference in carbon emissions of investing NT$100 million in TSMC and UMC. From the table below, TSMC’s carbon emissions are as high as 10.3 million metric tons, which is much higher than UMC’s 2.44 million metric tons. However, because TSMC’s company value is higher than UMC, with NT$16.7 trillion and NT$890.7 billion, TSMC’s financial attribution factor 0.0000060 is much lower than UMC with 0.0001123. Therefore, the carbon emissions recognized for investing NT$100 million in UMC are 274 metric tons, which is higher than TSMC’s 62 metric tons. It is evident that financial institutions should not only consider the carbon emissions of the investment targets, but also the company value of them.

Table: recognition of carbon emissions of investing NT$100 million in TSMC and UMC

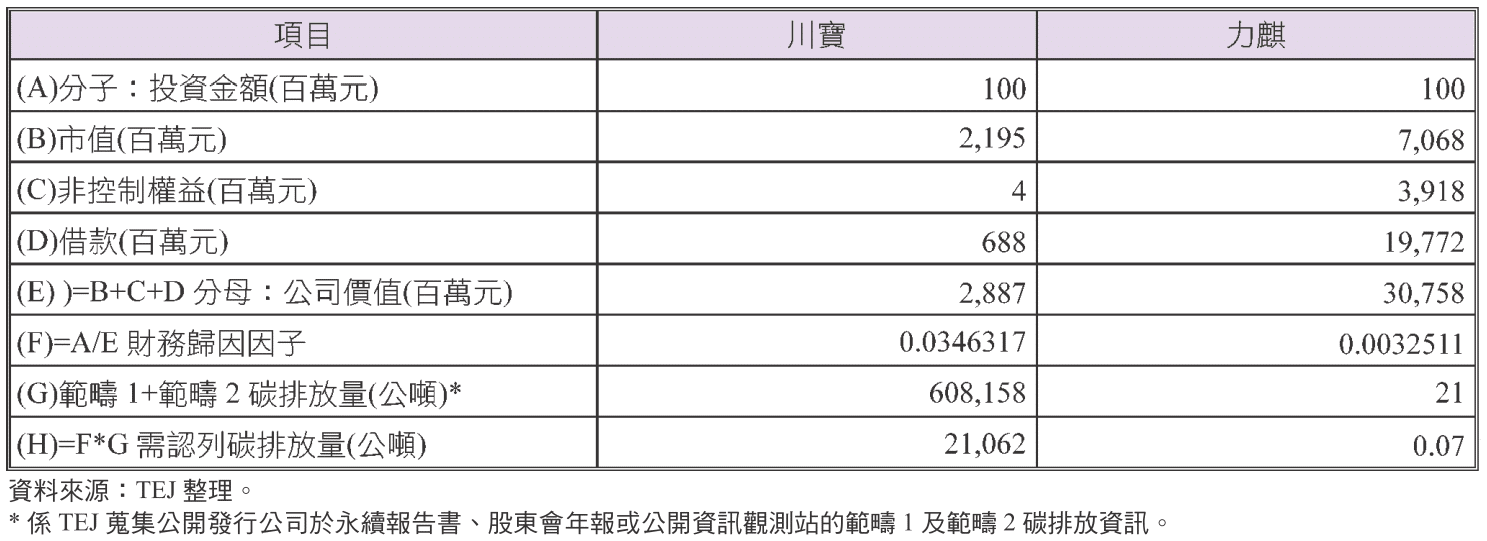

According to the statistics of listed and counter companies that have provided carbon emission data as of 2022/9/30, if a financial institution wants to invest NT$100 million in a listed and counter company in Taiwan, which ones are the companies with the highest and lowest carbon emissions recognized by financial institutions? Based on the preliminary statistics of this article, CHIME-BALL TECHNOLOGY CO., LTD has the highest carbon emission recognized by the financial institution, and the lowest one is RICH DEVELOPMENT CO.,LTD. As shown in the table, the value of CHIME-BALL TECHNOLOGY CO., LTD is relatively low. It needs to recognize ultra-high carbon emissions because its financial attribution factor is as high as 0.0346317. Conversely, RICH DEVELOPMENT CO.,LTD has the lowest carbon emissions recognized by financial institutions. Because the current data shows that its carbon emissions are extremely low, and its financial attribution factor is 0.0032511, so only 0.07 metric tons of carbon emissions need to be recognized.

According to the statistics of listed and counter companies that have provided carbon emission data as of 2022/9/30, if a financial institution wants to invest NT$100 million in a listed and counter company in Taiwan, which ones are the companies with the highest and lowest carbon emissions recognized by financial institutions? Based on the preliminary statistics of this article, CHIME-BALL TECHNOLOGY CO., LTD has the highest carbon emission recognized by the financial institution, and the lowest one is RICH DEVELOPMENT CO.,LTD. As shown in the table, the value of CHIME-BALL TECHNOLOGY CO., LTD is relatively low. It needs to recognize ultra-high carbon emissions because its financial attribution factor is as high as 0.0346317. Conversely, RICH DEVELOPMENT CO.,LTD has the lowest carbon emissions recognized by financial institutions. Because the current data shows that its carbon emissions are extremely low, and its financial attribution factor is 0.0032511, so only 0.07 metric tons of carbon emissions need to be recognized.

Table: Recognition of carbon emissions of Investing in CHIME-BALL TECHNOLOGY and RICH DEVELOPMENT .

This article explains the measurement method regarding greenhouse gas emissions in the investment and financing positions of financial institutions based on standards issued by the PCAF organization, and brings in case studies so that readers can understand and manage transition risks.

The objectives of the PCAF method are consistency and comparability. It is helpful for the financial industry to plan and manage the carbon reduction targets of investment and financing, and sort out climate-related transition risks and opportunities by calculating carbon emissions through a unified method. There are still some limitations in the current PCAF methodology, for example: there is no measurement method for derivative financial products; not all companies disclose Scope3 information, so there will be inconsistent emission standards in the calculation. In terms of commercial real estate, most countries that have not used energy labels for buildings will have no way of knowing how much energy consumption of a building. The PCAF committee will continue to improve and refine its measurement methodology.

TESG sustainable development solutions, one-stop solution to sustainable financial goals

TESG sustainable development solutions include TESG indicators and sustainable data sets, and also provide TCFD solutions: build PCAF methodology and internal investment and financing bid data in a systematic way. They enable the financial industry to the compilation and calculation of carbon emission data of the six major types of assets. Then, make the establishment of carbon reduction goals and scenario analysis to complete the policy formulation for transformation risks and opportunities.