Corporate Sustainability Reports (CSR), also known as Corporate Social Responsibility (CSR), is a general term for corporate disclosure of non-financial information, which aims to reveal the strategies, actions, and performance of companies in various economic, environmental, and social issues. CSR is a helpful tool for communicating with stakeholders and examining the effectiveness of corporate policy initiatives and internal management.

In the past decade, the competent authorities in Taiwan have been gradually promoting ESG information disclosure. Many vital industries or large corporations have been asked to disclose, and many have volunteered to do so. This article analyzes the status of our recent annual sustainability report disclosures.

Table of Contents

On February 6, 2010, the FSC issued the “Sustainable Development Best Practice Principles for TWSE/TPEx Listed Companies” and began to require companies to disclose their social responsibility information. Still, at that time, disclosure was only encouraged but not mandatory.

On November 26, 2014, the Taiwan Stock Exchange (TWSE) and the Taipei Exchange (TPEx) established the “Taiwan Stock Exchange Corporation Rules Governing the Preparation and Filing of Sustainability Reports” and the “Taipei Exchange Rules Governing the Preparation and Filing of Sustainability Reports” (after this referred to as the “TWSE/TPEx Sustainability Report Practice”), respectively. Corporations in specific industries (food industry, chemical industry, financial insurance industry, and catering revenues accounting for 50% or more of their total operating revenues) and companies with paid-in capital of $10 billion or more are required to file CSR compulsorily.

The “TWSE/TPEx Sustainability Reporting Practice” was revised on December 7, 2021, to require mandatory disclosure for companies with a capital of $2 billion, and will be applicable from 2023. In addition, the food, chemical, and financial insurance industries are required to obtain an opinion issued by an accountant under the standards published by the Accounting Research and Development Foundation of the Republic of China (ARDF).

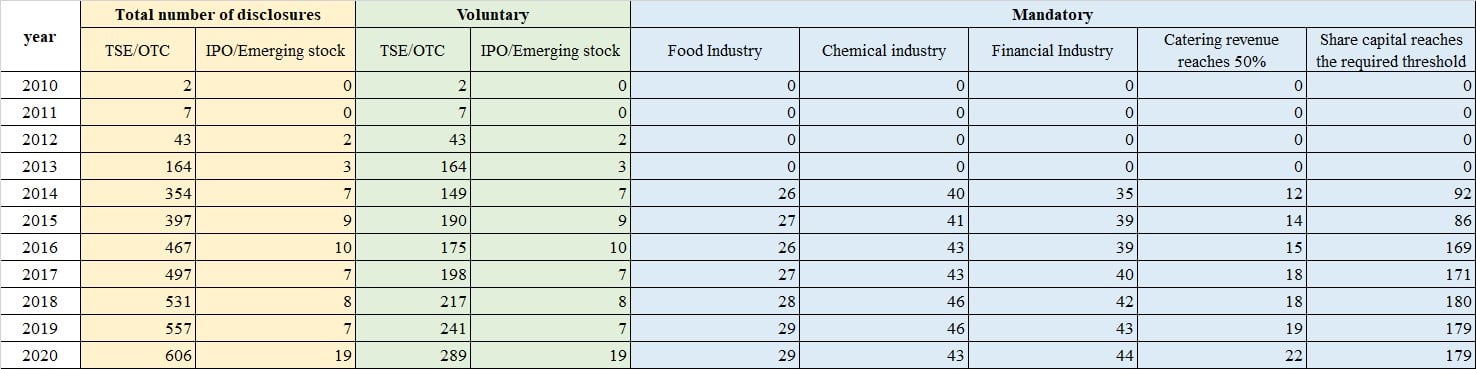

From 2010 to 2013, all sustainability reports were voluntarily disclosed by companies, with limited initial growth until 2013, when there was a significant increase. In 2014, the number of disclosures made by TSE/OTC companies increased from 164 in 2013 to 354 due to mandatory disclosure requirements, of which 205 were compulsory disclosures.

As a result of the regulatory revision, the number of companies whose share capital reached the required threshold increased from 86 in 2015 to 169 in 2016. In 2021, the regulations will be revised again, and it is expected that 550 companies will be required to disclose sustainability reports in 2022, more than twice as many as the 179 companies in 2020.

Table 1: Disclosure Status of Sustainability Report Recently (2010~2020)

〔Disclosure of Willingness and Company Market Capitalization Analysis〕

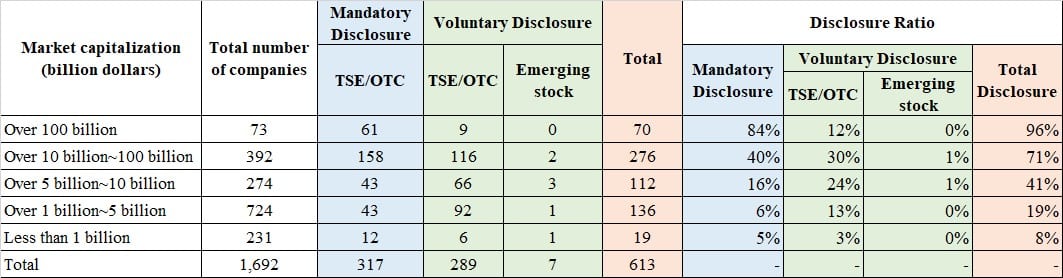

Cross-analysis of market value and nature of disclosure (voluntary or mandatory) in 2020, as shown in Table 2, of the 73 companies with a market capitalization of over NT$100 billion, 70 disclosed their sustainability reports, with a disclosure rate of 96%, while only three companies – Silergy-KY (6,415), Asmedia (5,269), and Giant (9921) – did not disclose their market capitalization. On the contrary, only 8% of the companies with a market capitalization of less than NT$1 billion were disclosed, indicating that the higher the market capitalization, the higher the proportion of disclosure.

Table 2: Status of Disclosure of Mandatory and Voluntary Market Value Categories in the 2020 Taiwan Sustainability Report

Source: Compiled by TEJ.

Note: The total number of 613 companies in 2020 is not the same as 625 in Table 1, mainly due to the lack of market capitalization of public companies.

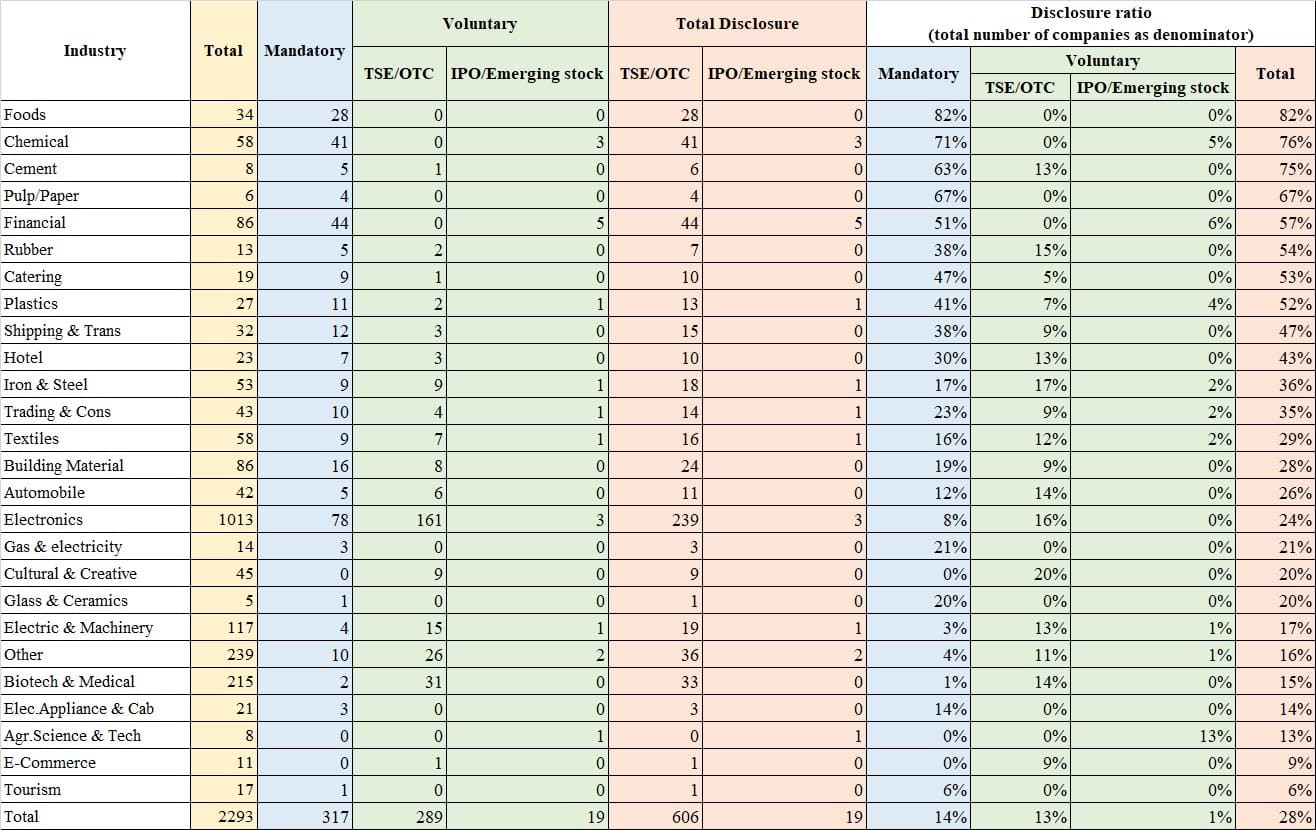

The chemical industry and the food and beverage industry, which have at least 50% of the revenue, are included in the biotechnology and medicine industry and the tourism industry, respectively, as the regulated industries in the law. Therefore, the biotechnology and medicine industry is divided into two types of industries: chemical industry and biotechnology and medical industry; the tourism industry is divided into three types of industries: hotel industry, catering industry, and other tourism industry. The top five industries in the 2020 Sustainability Report are the food industry, the chemical industry, the cement industry, the paper industry, and the financial industry. The food, financial, and chemical industries, which are subject to mandatory disclosure, rank in the top five as expected. In contrast, the cement and paper industries have a higher proportion of disclosure due to smaller samples and mandatory disclosure.

Table 3: Taiwan Sustainability Report Industry Classification Disclosure Status in 2020

Since 2010, the number of sustainability reports disclosed has been increasing yearly due to regulatory changes and the increased willingness of companies to disclose voluntarily. In addition, we can see that the higher the market capitalization, the higher the proportion of sustainability reports disclosed. For example, all listed food, chemical, and financial industries must disclose sustainability reports.

For companies that are not required by regulations but voluntarily disclose, that is good for the ESG of the company. However, as international market conditions and regulations are adjusted year by year, the scope and content standards for disclosure will be expected to become more comprehensive and consistent in the future.

TEJ has developed the TESG Rating with sustainability reports as the primary source of information, providing more complete and comparable data. For public companies that do not provide a report, we can also supplement the TESG metrics with other sources of information, such as the annual report of the shareholders’ meeting, the Public Information Observatory, or news collected daily.