Taiwan Economic Journal (TEJ), one of the biggest and most detailed financial databases, held “TCRI 2024 Industry Prospective Seminar” in Taipei on March 27 2024, attracting many market analysts and researchers in financial firms. The seminar invites Professor Chen Sung Xsing from Chinese Culture University and TCRI researchers from TEJ to discuss both global and geopolitical risks Taiwan companies face.

Table of Contents

Since 2018, the US-China trade war has escalated, leading to a continuous deterioration in relationships between the two countries. Professor Chen believes that a new Cold War pattern has already taken shape. As we approach 2024, the global economic situation remains volatile and unpredictable. With several factors intertwining together, including Russo-Ukrainian War, Mid-East Regional Conflict, the rising of Nationalism and Protectionism, etc., global economy would suffer a sluggish recovery.

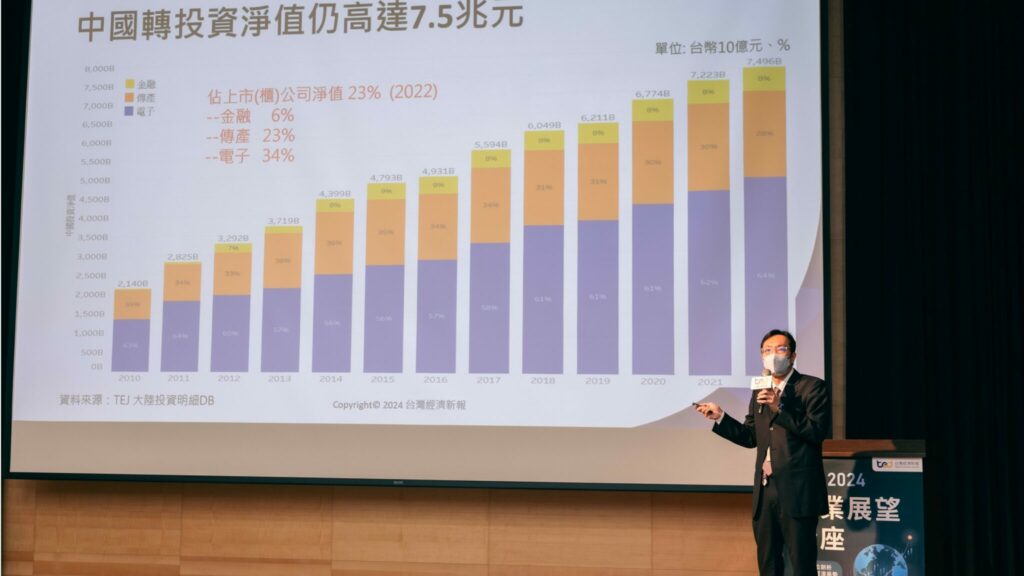

Under the new cold war pattern, global supply chain has been forced to reconfigure to enhance supply chain resilience, while Taiwanese businesses also reduce their dependence on China to lower their risk exposure. According to data from the Ministry of Economic Affairs, Taiwanese investment in China hit a new low in 2023. However, when we look at the reinvestment figures for Taiwan public-listed companies, based on the calculation of TEJ, as of the end of 2022, these companies still had reinvested a substantial amount of NT$7.5 trillion in China, accounting for 23% of their net worth. This accumulation of investment over the past years underscores the significant financial ties that Taiwanese businesses still maintain with China. While the overall reliance of public-listed companies on China has been gradually decreasing, a closer examination reveals variations in the degree of decline. Some group corporations continue to exhibit high dependence on the Chinese market, and a few have even increased their investments in China. Hence, it’s essential to closely monitor these developments and consider the implications for future growth and risk management.

Traditional industry in Taiwan’s domestic market has seen a gradual recovery in post-pandemic consumer spending, benefiting industries such as food, tourism, and restaurants. However, the export sector faces challenges due to China’s excess production capacity, leading to deflationary pressures in global exports. Industries closely linked to China, such as plastics, steel, and cement, have unfavorable operating prospects. Additionally, recent extreme weather events and geopolitical influences have impacted container shipping, resulting in short-term benefits from rising freight rates but a bearish long-term outlook due to excess capacity.

Electronics industry has benefited from the surge of investment in generative AI. AI cloud computing is experiencing rapid growth, while AI edge computing is still in its early stages. By 2024, supply chains highly influenced by AI are expected to demonstrate robust growth. Additionally, areas with lower AI impact will experience a moderate recovery due to resurgence in demand and the low base effect.

Since the establishment of TEJ in 1990, we have focused on providing Asia financial markets with data for performing analysis, and gradually become one of the biggest and most detailed financial databases. One of our greatest accomplishments is the construction of TCRI, which has become an indispensable source for investment and credit reference information in Taiwan’s financial industry. TEJ will continue to monitor the economic trends in Taiwan, striving to provide clients with professional information and analysis to address various challenges related to corporate and financial development.