Table of Contents

Seasoned equity offerings are a common way for listed companies to raise capital. When companies need funding, they may issue new shares to the market instead of relying only on bank loans or corporate bonds. The proceeds can be used for capacity expansion, new business investments, debt repayment, financial restructuring, or future growth needs.

For investors, seasoned equity offerings are more than a financing tool; they are also important corporate events to monitor. The announcement timing, fundraising purpose, issuance terms, and subsequent stock price reaction often reflect how the market reassesses the company’s funding needs, potential equity dilution, and management’s capital allocation ability.

This raises a key question: does a seasoned equity offering signal future growth, or does it create short-term pressure on share prices? This article first introduces the basic concepts and process of seasoned equity offerings in Taiwan, and then uses an event study approach to examine the stock price reactions of Taiwanese listed companies before and after such announcements.

The empirical results show that, one to two trading days after the announcement, the average abnormal returns of Taiwanese listed companies are significantly negative. This suggests that the market tends to interpret seasoned equity offerings as a signal of equity dilution, higher funding needs, or valuation pressure in the short term. However, the negative reaction does not persist over the long run, indicating that the stock price impact is more likely a short-term announcement effect rather than clear evidence of deteriorating fundamentals.

A seasoned equity offering refers to a company issuing new shares to raise cash from existing shareholders or market investors. Unlike a stock dividend or bonus issue, the main purpose of a seasoned equity offering is to obtain external capital, which is usually related to business growth plans or financial structure adjustments.

Common purposes of seasoned equity offerings include:

| Purpose | Description |

|---|---|

| Expanding business scale | For example, building new plants, increasing capacity, or investing in new business units |

| Repaying debt | Reducing the debt ratio and improving the financial structure |

| Strengthening working capital | Supporting daily operations, raw material purchases, or cash flow needs |

| Funding capital expenditures | Investing in equipment, R&D, or long-term projects |

| Improving financial quality | Raising the equity ratio and reducing financial risk |

However, seasoned equity offerings do not necessarily have a positive impact on stock prices. If a company issues new shares but fails to convert the raised capital into higher revenue and earnings growth, existing shareholders may face equity dilution pressure. The market may also interpret the offering as a sign of cash flow stress, which could lead to a short-term negative reaction in the stock price after the announcement.

Seasoned equity offerings in Taiwan are usually conducted according to regulations and company rules, with new shares allocated to different subscription groups. Common methods include subscription by existing shareholders, employee subscription, and public offering.

| Subscription Method | Description | Meaning for Investors |

|---|---|---|

| Existing shareholder subscription | The company allocates subscription rights based on each shareholder’s existing ownership percentage | Existing shareholders can subscribe to maintain their ownership ratio and reduce dilution |

| Employee subscription | The company reserves part of the new shares for employees to subscribe | May help strengthen employee incentives |

| Public offering | Part of the new shares are sold publicly, allowing investors to participate through subscription or lottery | General investors may have the opportunity to subscribe at the offering price |

| Specific person subscription | If existing shareholders or employees do not fully subscribe, the remaining shares may be subscribed by specific persons | May affect how the market interprets the company’s funding demand and subscription demand |

The subscription price of seasoned equity offerings is usually lower than the market price to improve investors’ willingness to participate. Therefore, investors may pay attention to the “subscription discount” as a potential short-term opportunity. However, if the discount is too large, the market may become concerned about post-offering dilution pressure, and the stock price may still come under pressure.

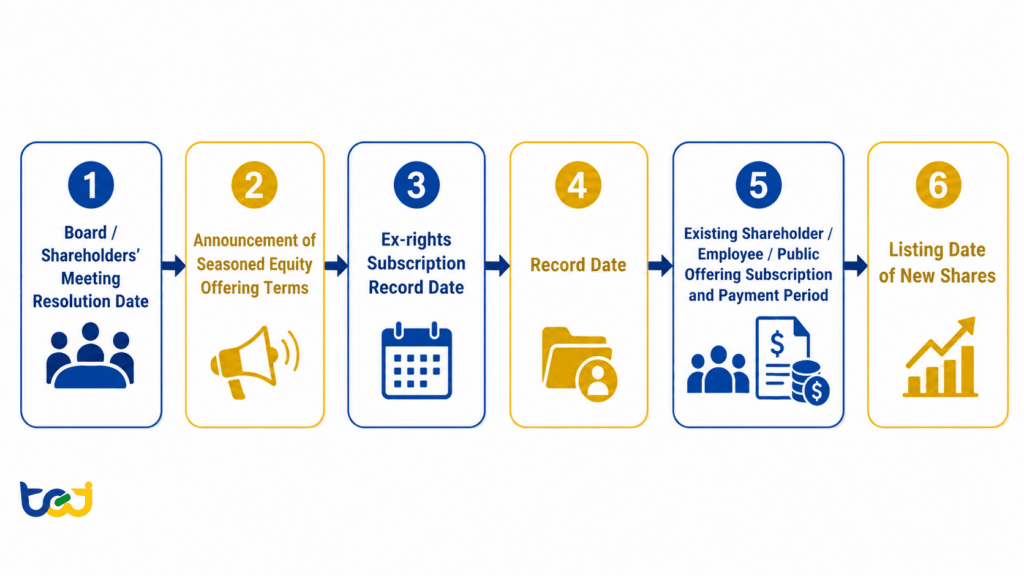

For investors, a seasoned equity offering should not be viewed only from the announcement date. From the board or shareholders’ meeting resolution, offering terms announcement, ex-rights subscription record date, to the listing of new shares, each stage may have different implications for stock prices, liquidity, and short-term supply-demand conditions. Therefore, understanding the event timeline helps investors better assess the market reaction and the potential meaning behind price movements before and after the offering.

The seasoned equity offering process in Taiwan’s stock market is as follows:

Figure 1: Seasoned Equity Offering Process and Key Dates

| Key Date | Description | Possible Impact |

|---|---|---|

| Board / Shareholders’ Meeting Resolution Date | An important date when the company decides to conduct a seasoned equity offering, and when the market receives the offering information | The market may begin to reassess the company’s valuation |

| Ex-rights Subscription Record Date | Determines which shareholders are eligible to subscribe for the new shares | Affects whether existing shareholders can participate in the subscription |

| Record Date | Investors must complete share transfer registration by this date to be eligible for subscription | May affect short-term trading behavior |

| Payment Period | Existing shareholders, employees, or public offering investors pay for the subscribed shares | Reflects investors’ willingness to participate |

| Listing Date of New Shares | The newly issued shares are officially listed and become tradable | If investor interest is low, selling pressure may emerge |

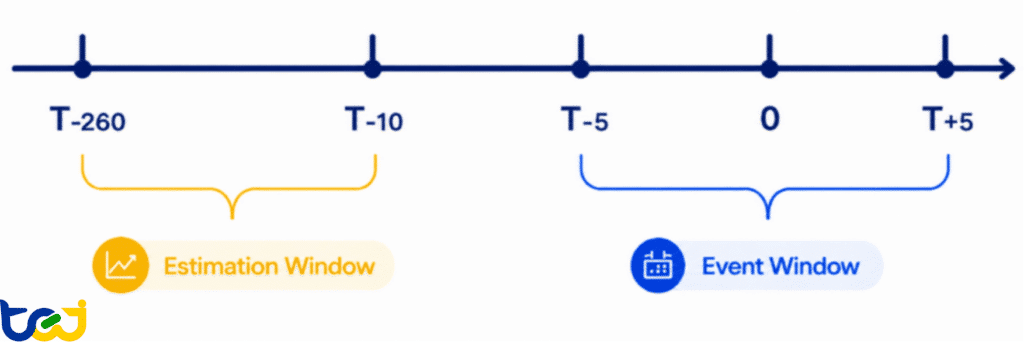

In this event study, the “shareholders’ meeting resolution date” is used as the event date to examine whether stock prices show abnormal reactions after the market receives information about the seasoned equity offering. This date is selected because it is usually one of the earliest key points at which the market becomes aware of the seasoned equity offering, and can therefore be regarded as the critical date when the event is formally transmitted to the market.

To examine whether seasoned equity offering announcements affect stock prices, this study adopts an event study approach. The core idea of an event study is to first estimate a stock’s expected return under normal market conditions, and then compare it with the actual return after the event. If the actual return is significantly higher or lower than the expected return, it can be regarded as an abnormal return, which helps assess whether the market reacted to the event announcement.

This study uses Taiwan-listed companies with seasoned equity offering events as the research sample, and defines the “shareholders’ meeting date” as the event date. The reason for using the shareholders’ meeting date is that the market usually receives key information related to the seasoned equity offering around this period, making it an important date when the event is formally incorporated into market prices.

Figure 2: Event Study Timeline

This study uses the Fama-French five-factor model to estimate expected returns. The model includes the market risk premium, size factor, book-to-market factor, profitability factor, and investment factor, which helps control for systematic factors that may affect individual stock returns. If the actual return during the event window is lower than the model-estimated expected return, it results in a negative abnormal return. Conversely, if the actual return is higher than the expected return, it results in a positive abnormal return.

Compared with simply observing raw returns before and after the event, the event study method further controls for systematic factors such as market, size, value, profitability, and investment style. This allows the study to focus more directly on the excess price reaction caused by the seasoned equity offering announcement itself.

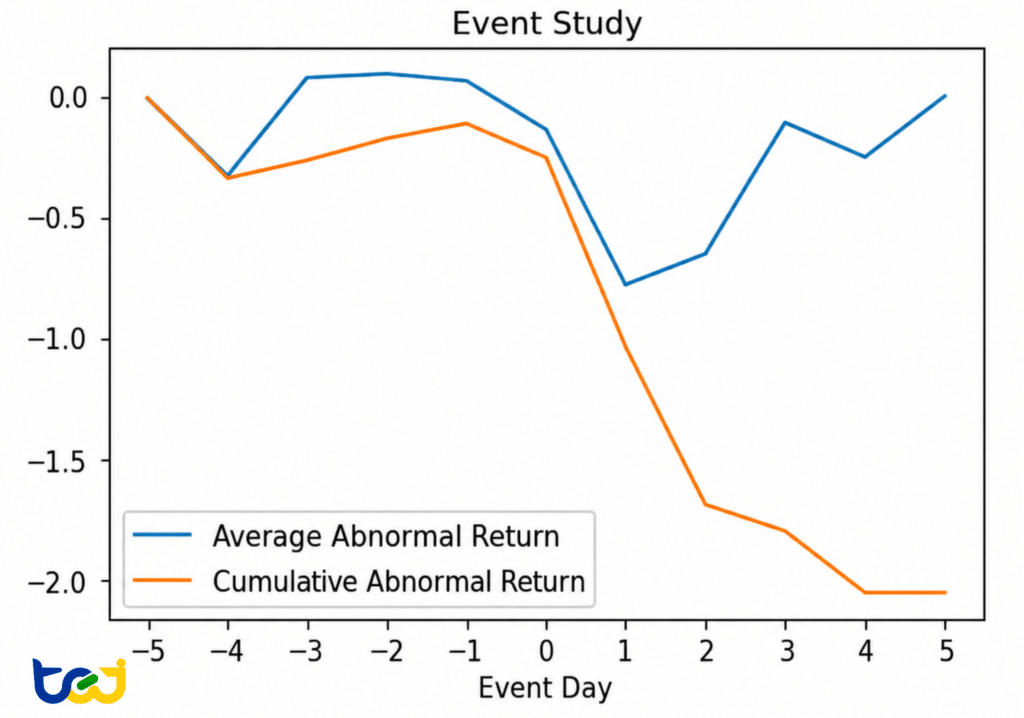

According to the event study results, the average abnormal return becomes clearly negative one to two trading days after the seasoned equity offering announcement. This indicates that, after receiving the seasoned equity offering information, the market shows a relatively negative pricing reaction in the short term.

Figure 3: Trends in Average Abnormal Returns and Cumulative Abnormal Returns

From the figure, the average abnormal return clearly weakens one to two trading days after the event date. This suggests that investors may reassess the impact of the seasoned equity offering on equity dilution, funding needs, and short-term supply-demand conditions after the announcement. This result is also consistent with the market’s common interpretation of seasoned equity offerings: when a company raises capital by issuing new shares, investors may first react to concerns over equity dilution, higher funding needs, or the possibility that the company’s current share price is overvalued.

However, abnormal returns gradually return to a level close to zero in the following trading days. This indicates that the negative impact of the seasoned equity offering announcement is more likely a short-term reaction, as the market may gradually digest the relevant information within a few days after the announcement.

It is worth noting that the market reaction may not be most obvious on the event date itself. One possible reason is that companies often release material information after the market closes, meaning investors’ actual reaction may be delayed until the next trading day. Therefore, when analyzing the impact of corporate events on stock prices, investors should not focus only on the announcement date, but should also include several trading days after the announcement in the analysis.

In addition to observing the trend of average abnormal returns, this study further tests whether daily abnormal returns are significantly different from zero. If abnormal returns are statistically significant, it indicates that the event has an identifiable impact on stock prices, rather than simply reflecting random market fluctuations.

Figure 4: t-test Results for Abnormal Returns

The test results show that seasoned equity offering announcements do trigger short-term stock price reactions. In particular, the market reaction is more evident one to two trading days after the announcement, suggesting that investors tend to make a short-term negative assessment of seasoned equity offerings.

This also reminds investors that when facing major corporate financing events, they should not only observe whether a company conducts a seasoned equity offering, but also further evaluate the use of proceeds, industry conditions, the company’s financial structure, and the market’s view of its valuation. The same type of seasoned equity offering may lead to different market reactions depending on the industry, business cycle, and company fundamentals.

This study uses an event study approach to examine stock price reactions before and after seasoned equity offering announcements by Taiwan-listed companies. The results show that, one to two trading days after the announcement, average abnormal returns are clearly negative. This indicates that the market tends to first price in concerns over equity dilution, higher funding needs, and valuation pressure in the short term.

However, this negative effect does not persist for a long period. Abnormal returns gradually return to a level close to zero in the following days, suggesting that the impact of seasoned equity offering announcements on stock prices is more likely a short-term announcement effect, rather than clear evidence of deteriorating long-term fundamentals.

For investors, seasoned equity offerings should not be simply viewed as either good news or bad news. Instead, they should be evaluated together with the use of proceeds, issuance terms, financial structure, industry conditions, and market expectations. If the proceeds are used for capacity expansion, R&D, or strengthening long-term competitiveness, the stock may return to fundamental-based valuation after the short-term negative reaction. However, if the offering size is too large, or if the proceeds are mainly used for debt repayment or working capital needs, market concerns over dilution and financial pressure may become more pronounced.