Table of Contents

LazyBear 是在國際知名交易平台 TradingView上極具影響力的指標開發者。他創作了大量廣受歡迎的客製化技術指標,其開源的程式碼啟發了全球無數量化交易員與技術分析愛好者。LazyBear 的指標通常專注於改善傳統指標的延遲性,並結合獨特的市場觀察來捕捉趨勢與動能。本次採用的「Impulse MACD」即為他的代表作之一。此指標並非傳統的指數平滑異同移動平均線(MACD),而是進行了顯著的改良:它使用零延遲的雙指數移動平均線(DEMA)來更快速地響應價格變化,並結合平滑化(SMMA)的高低價通道來判斷市場的「衝量」(Impulse)。其核心思想是,只有當價格動能與趨勢方向一致時,產生的交易信號才更具價值,藉此過濾掉部分盤整行情中的雜訊。

本研究以台灣指數期貨(台指期, TX)作為唯一的交易標的,並使用每日的最高價、最低價與收盤價資料進行指標計算與回測。由於策略中的指標(如DEMA、SMMA)需要一段時間的歷史數據進行預熱(warm-up),最長的計算週期為 30 天,且為了確保回測開始時有足夠穩定的歷史數據,實際回測期間訂為2019年1月1日至2025年9月12日,以確保所有交易信號的嚴謹性與有效性

md (快線)。md 進行簡單移動平均,得到信號線 sb (慢線)。md 由下往上穿越慢線 sb 時,產生買進信號。md 由上往下穿越慢線 sb 時,產生賣出信號。在期貨合約到期前,策略會自動將即將到期的合約平倉,並在新的近月合約上建立相同的部位,以確保回測的連續性。

首先,我們需要設定 TEJ API 的金鑰以存取資料庫。接著,透過環境變數指定回測所需的標的 (台指期貨 TX 與大盤 IR0001) 及資料期間。最後,使用 zipline ingest 指令將這些資料匯入 Zipline 的本地資料庫中,以提供回測使用。

import os

import yaml

''' ------------------- 不使用 config.yaml 管理 API KEY 的使用者可以忽略以下程式碼 -------------------'''

notebook_dir = os.path.dirname(os.path.abspath(__file__)) if '__file__' in globals() else os.getcwd()

yaml_path = os.path.join(notebook_dir, '..', 'config.yaml')

yaml_path = os.path.abspath(os.path.join(notebook_dir, '..', 'config.yaml'))

with open(yaml_path, 'r') as tejapi_settings: config = yaml.safe_load(tejapi_settings)

''' ------------------- 不使用 config.yaml 管理 API KEY 的使用者可以忽略以上程式碼 -------------------'''

# --------------------------------------------------------------------------------------------------

os.environ['TEJAPI_BASE'] = config['TEJAPI_BASE'] # = "https://api.tej.com.tw"

os.environ['TEJAPI_KEY'] = config['TEJAPI_KEY'] # = "YOUR_API_KEY"

# --------------------------------------------------------------------------------------------------

os.environ['future'] = 'TX'

os.environ['ticker'] = 'IR0001'

os.environ['mdate'] = '20100101 20250925'

!zipline ingest -b tquant_future導入本次策略時作所需的 Python 套件,包含 pandas、 numpy 、 talib 以及 Zipline 框架中的各項核心功能。

import numpy as np

import pandas as pd

import talib

import pyfolio as pf # 使用 pyfolio 進行回測

from zipline.api import (

order_target, # 持倉的目標口數

order, # 下單加減多少口數

cancel_order, # 取消訂單

get_open_orders, # 拿到所有掛單

get_order, # 用訂單ID查詢訂單狀態

record, # 把指標或任何想記錄的數值記錄到回測結果

continuous_future, # zipline 自動換月

schedule_function, # 安排排程,在指定日期 / 時間呼叫 func

date_rules, # 搭配 schedule_function 的日期 / 時間規則

time_rules,

set_commission, # 設定手續費模型

set_slippage, # 設定滑價模型

set_benchmark, # 設定績效比較基準

symbol # 取得一個可交易 / 引用的資產物件

)

from zipline.finance.execution import StopOrder # 停損市價單

from zipline.finance import commission, slippage # 費用模型 / 滑價模型命名空間

from zipline import run_algorithm # 回測主入口

from zipline.utils.run_algo import get_transaction_detail # 把 results 拆成positions / transaction / orders三張表

from zipline.utils.calendar_utils import get_calendar # 取得交易所行事曆

import matplotlib.pyplot as plt

為了實現 Impluse MACD 策略,我們需要定義兩個關鍵的輔助函數:

_smma : 計算平滑移動平均線 (Smoothed Moving Average),這是後續指標的基礎。calculate_indicators : 此函數整合了所有指標的計算邏輯,包含 HLC/3、ATR、高低價通道的 SMMA,以及最終的快線 md 與慢線 sb。這是策略信號的核心。import talib

import pandas as pd

def _smma(series, period):

"""計算平滑移動平均線(smoothing moving average)"""

smma_output = pd.Series(np.nan, index=series.index)

sma_val = talib.SMA(series, timeperiod=period)

first_valid_index = sma_val.first_valid_index()

if first_valid_index is None:

return smma_output

try:

start_loc = series.index.get_loc(first_valid_index)

except KeyError:

return smma_output

smma_output.loc[first_valid_index] = sma_val.loc[first_valid_index]

for i in range(start_loc + 1, len(series)):

prev_smma = smma_output.iloc[i - 1]

current_val = series.iloc[i]

if pd.notna(prev_smma) and pd.notna(current_val):

smma_output.iloc[i] = (prev_smma * (period - 1) + current_val) / period

else:

smma_output.iloc[i] = np.nan

return smma_output

def calculate_indicators(data, ma_len, sig_len, atr_len):

"""計算完整的 Impluse macd 指標和 ATR"""

data['hlc3'] = (data['high'] + data['low'] + data['close']) / 3

data['atr'] = talib.ATR(data['high'], data['low'], data['close'], timeperiod=atr_len)

data['High_smma'] = _smma(data['high'], period=ma_len)

data['Low_smma'] = _smma(data['low'], period=ma_len)

data['hlc3_zlema'] = talib.DEMA(data['hlc3'], timeperiod=ma_len)

data['md'] = np.where(data['hlc3_zlema'] > data['High_smma'],

data['hlc3_zlema'] - data['High_smma'],

np.where(data['hlc3_zlema'] < data['Low_smma'], data['hlc3_zlema'] - data['Low_smma'], 0))

data['sb'] = talib.SMA(data['md'], timeperiod=sig_len)

return datainitialize 函數:策略初始化在 initialized 函數中,我們進行回測開始前的一次性設定。這包括:

ma_len, sig_len) 以及 ATR 停損的乘數 (atr_multiplier)。continous_future 連續合約物件。commisson) 與滑價 (slippage) 模型,讓回測結果更貼近真實。IR001) 作為策略績效的比較基準。schedule_function 安排每日要執行的交易邏輯 (daily_tarde) 與收盤後執行的轉倉檢查 (roll_futures)def initialize(context):

'''

策略初始化函數, 用來設定全域參數、資產、手續費/滑價、與排程

context是一個物件, 像一個可寫入的「工具箱、命名空間」

'''

context.ma_len = 30

context.sig_len = 8

context.atr_len = 20

context.atr_multiplier = 3.25

context.future = continuous_future('TX', offset = 0, roll = 'calendar', adjustment = 'add') # 建立台指期連續合約資產,之後用他下單與取價

set_commission(futures = commission.PerContract(cost = 200, exchange_fee = 0))

set_slippage(futures = slippage.FixedSlippage(spread = 10.0))

set_benchmark(symbol('IR0001')) # 設定大盤為比較基準

context.stop_loss_price = None # 目前生效的止損價格

context.stop_order_id = None # 已送出的stop單,方便之後修改、取消

# 每天執行交易策略

schedule_function(func = daily_trade, date_rule = date_rules.every_day(), time_rule = time_rules.market_open(minutes = 30))

# 每天檢查是否要轉倉

schedule_function(func = roll_futures, date_rule = date_rules.every_day(), time_rule = time_rules.market_close())daily_trade 函數: 每日交易與風險控制此函數會在每個交易日被調用,是策略的核心。主要步驟如下:

calculate_indicators 計算出 md、sb、atr。md、sb 的黃金交叉或死亡交叉來產生 buy_siganl 或 sell_signal。_get_tx_chain_state 的作用:

context.portfolio.positions 中是否有當前的連續合約(context.future)。因為在轉倉期間,我們的實際部位可能還留在即將到期的舊合約上,而 context.future 已經指向了新合約。_get_tx_chain_state 這個輔助函數會遍歷所有持倉,檢查資產的 root_symbol 是否為 ‘TX’,從而準確地判斷我們在整個台指期或產品鏈上總共持有的口數 (root_aty),避免了轉倉重複下單問題。StopOrder 實現。如果停損點需要更新,會先取消就訂單再掛上新訂單。def _get_tx_chain_state(context, root = 'tx'):

'''掃描所有部位,找出台指期的口數'''

active_asset = None

root_qty = 0

for a, p in context.portfolio.positions.items():

if getattr(a, 'root_symbol', None) == root and p and p.amount != 0:

root_qty += p.amount

if active_asset is None:

active_asset = a

return active_asset, root_qty

def daily_trade(context, data):

'''每日執行的交易邏輯'''

try:

# 跟zipline要250根日線的歷史資料

hist = data.history(context.future, ['high', 'low', 'close'], bar_count = 250, frequency = '1d')

indicators = calculate_indicators(data = hist, ma_len = context.ma_len, sig_len = context.sig_len, atr_len = context.atr_len)

md = indicators['md']

sb = indicators['sb']

atr = indicators['atr'].iloc[-1]

current_price = data.current(context.future, 'price') # 取當前價格

except Exception as e:

print(f'指標計算錯誤: {e}')

return

# 產生買賣訊號

buy_signal = (md.iloc[-2] < sb.iloc[-2]) and (md.iloc[-1] > sb.iloc[-1])

sell_signal = (md.iloc[-2] > sb.iloc[-2]) and (md.iloc[-1] < sb.iloc[-1])

# 取當月合約與目前持倉, 連續合約會在某一天切換到新月但持倉可能還在舊月

current_contract = data.current(context.future, 'contract')

held_asset, root_qty = _get_tx_chain_state(context, 'TX')

if root_qty != 0:

pos_asset = held_asset

pos = context.portfolio.positions[pos_asset]

px = data.current(context.future, 'price')

if context.stop_loss_price is None:

# 初始建立止損單

if pos.amount > 0:

context.stop_loss_price = current_price - context.atr_multiplier * atr

elif pos.amount < 0:

context.stop_loss_price = current_price + context.atr_multiplier * atr

amount = -pos.amount

# 送出一張市價止損單

context.stop_order_id = order(pos_asset, amount, style = StopOrder(context.stop_loss_price))

else:

# 已有止損, 止損價只往有利方向前進

if pos.amount > 0:

new_stop_price = current_price - context.atr_multiplier * atr

context.stop_loss_price = max(new_stop_price, context.stop_loss_price)

elif pos.amount < 0:

new_stop_price = current_price + context.atr_multiplier * atr

context.stop_loss_price = min(new_stop_price, context.stop_loss_price)

# 原本有掛止損單

if context.stop_order_id:

stop_order_object = get_order(context.stop_order_id)

if stop_order_object and stop_order_object.status == 0: # status == 0, 訂單處於open狀態

if stop_order_object.stop != context.stop_loss_price:

cancel_order(context.stop_order_id)

amount = -pos.amount

context.stop_order_id = order(pos_asset, amount, style = StopOrder(context.stop_loss_price))

else:

context.stop_order_id = None

else:

# 無倉位卻有殘留停損單, 取消並清空紀錄

if context.stop_order_id:

stop_order_object = get_order(context.stop_order_id)

if stop_order_object and stop_order_object.status == 0:

cancel_order(context.stop_order_id)

context.stop_order_id = None

context.stop_loss_price = None

if buy_signal:

order_target(current_contract, 1)

elif sell_signal:

order_target(current_contract, -1)

record(

price = current_price,

md = md.iloc[-1],

sb = sb.iloc[-1],

stop_loss = context.stop_loss_price

)roll_futures函數: 期貨轉倉此函數會在每日收盤後檢查持有的期貨合約是否即將到期(5天內)。如過是,則會自動將舊合約的倉位平倉,並在新月份的合約上建立相同數量的倉位,同時為新倉位掛上初始的移動止損單。

def roll_futures(context, data):

'''處理期貨轉倉, initialize會在每日收盤前呼叫'''

for asset, pos in context.portfolio.positions.items():

if not pos or pos.amount == 0:

continue

acd = getattr(asset, 'auto_close_date', None)

if not acd:

continue # 只選期貨資產(有到期日的)

days_to_auto_close = (acd.date() - data.current_session.date()).days

if days_to_auto_close > 5:

continue # 到到期日還剩五天以上不轉倉

new_contract = data.current(context.future, "contract")

if new_contract == asset:

continue # 已經是當前月份不需轉倉

for o in get_open_orders(asset):

cancel_order(o.id) # 取消所有掛單

context.stop_loss_price = None

context.stop_order_id = None

# 重新讀一次口數

qty = context.portfolio.positions[asset].amount

if qty != 0:

print(f"執行轉倉: 從 {asset.symbol} 到 {new_contract.symbol}, 口數 {qty}")

order_target(asset, 0) # 關掉舊倉

order_target(new_contract, qty) # 開新合約倉

try:

hist = data.history(context.future, ['high', 'low', 'close'], bar_count = 250, frequency = '1d')

atr = talib.ATR(hist['high'], hist['low'], hist['close'], timeperiod = context.atr_len).iloc[-1]

px = data.current(context.future, 'price')

# 掛新止損單

if qty > 0:

new_stop = px - context.atr_multiplier * atr

elif qty < 0:

new_stop = px + context.atr_multiplier * atr

context.stop_loss_price = new_stop

context.stop_order_id = order(new_contract, -qty, style = StopOrder(context.stop_loss_price))

except Exception as e:

print(f"[roll future] 新合約掛單失敗: {e}")

break設定回測的起迄時間、初始資金等參數,並呼叫 run_algorithm 來啟動整個回測流程。回測結果會儲存在 results 物件中。

start_date = pd.Timestamp('2019-01-01', tz = 'utc')

end_date = pd.Timestamp('2025-09-19', tz = 'utc')

# 呼叫zipline主入口

results = run_algorithm(

start = start_date,

end = end_date,

initialize = initialize,

capital_base = 1000000,

data_frequency = 'daily',

bundle = 'tquant_future',

trading_calendar = get_calendar('TEJ')

)

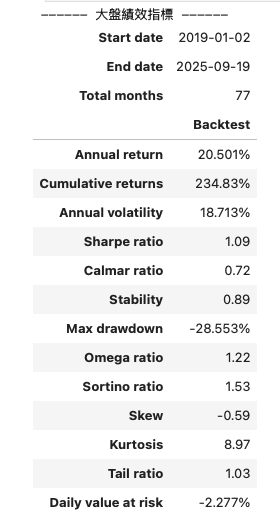

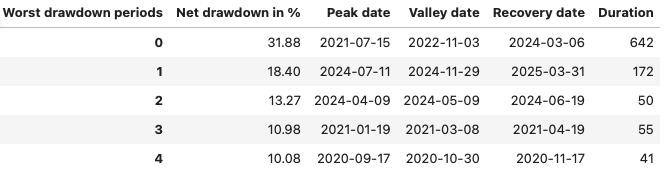

print("回測完成")回測結束後,我們從 results 物件中提取數據,計算策略本身以及大盤的各項關鍵績效指標,例如累積報酬、年化報酬、夏普比率、最大回撤等,並將結果打印出來以便比較。

# 從 Zipline 的 results 物件中提取 Pyfolio 所需的數據格式

returns, positions, transactions = pf.utils.extract_rets_pos_txn_from_zipline(results)

# 提取基準報酬(benchmark returns)

benchmark_rets = results.benchmark_return

# 基準報酬指標

print("------ 大盤績效指標 ------")

pf.show_perf_stats(benchmark_rets)

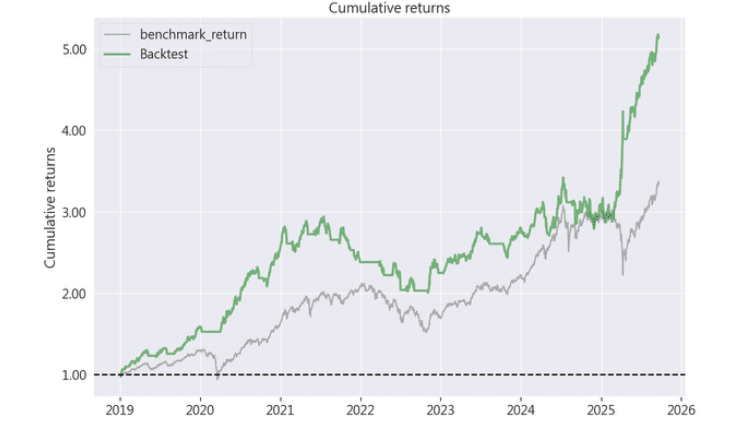

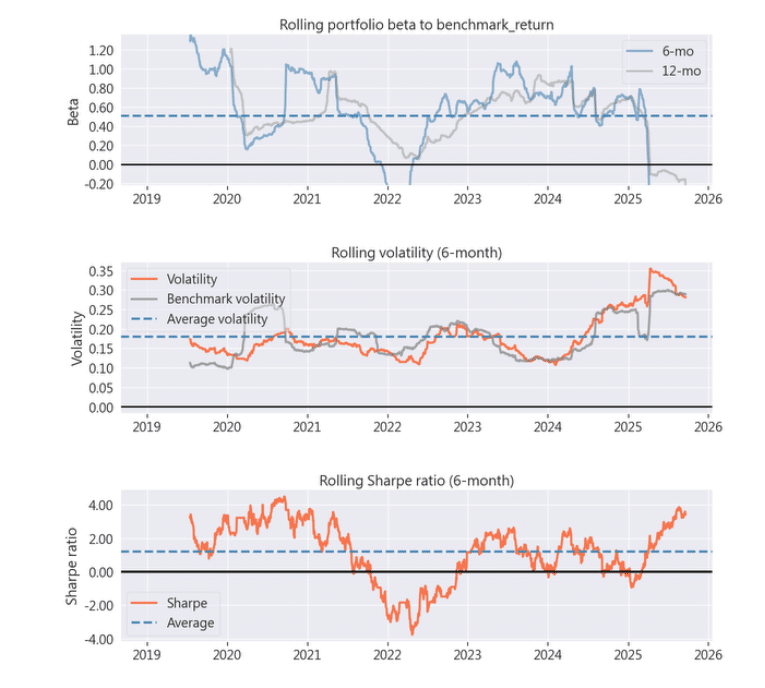

# 產生完整的 Pyfolio 績效分析報告

print("------ 策略績效指標 ------")

pf.create_returns_tear_sheet(

returns = returns,

positions = positions,

transactions = transactions,

benchmark_rets = benchmark_rets,

)