On August 23, 2023, Nvidia reported robust Q2 2024 financials, with revenue hitting $13.507 billion and an EPS of $2.48 — showcasing an impressive 854% YoY surge. These financial figures not only outshine expectations but also significantly surpass them. Furthermore, Nvidia is bullish about the potential Q3 2024 revenue, projecting it to reach $16 billion with a gross profit margin of around 71.5%. In the midst of the global AI boom, Nvidia undeniably stands as the company benefitting the most, with its stock price soaring by 256% since the beginning of the year. In May, its market value surpassed $1 trillion, making it the first semiconductor company to achieve this milestone. Nvidia brilliantly executes the concept of the “Davis Double Play” (Note). However, if we shift our focus to AI server supply chain companies like Wistron and Quanta, are they starting to see profits from AI products? In this article, we will thoroughly examine the production and sales structures of these companies, exploring whether Taiwanese manufacturers in this domain are beginning to reap tangible benefits from the AI wave, helping you grasp the impact of the advent of AI on companies operating within the supply chain!

Note: The Davis Double Play theory in the investment market suggests that as a company experiences consistent profit growth and an increase in its EPS, the market assigns it a higher valuation. This elevated valuation, in turn, triggers a compounded increase in the company’s stock prices.

Generative AI Drives the Brilliance of Nvidia

In November 2022, OpenAI made ChatGPT available to the general public, and in less than two months, the user base surpassed 100 million. Since then, ChatGPT has set ablaze the global craze for generative AI.

In a recent statement, Nvidia CEO Jensen Huang mentioned that global enterprises are moving from general-purpose computing towards the era of accelerated computing and generative artificial intelligence. Before delving into large-scale AI training models, GPUs are deemed the most essential weaponry. Nvidia’s A100 chip and the next-gen H100 chip have consequently become the most coveted chips in the industry. For ChatGPT to continue learning and generating new content, the computational capability of chips becomes pivotal. Consequently, servers equipped with GPUs, FGPU, and ASIC chips are progressively being adopted by major tech giants. These servers are what we commonly refer to as “AI servers.”

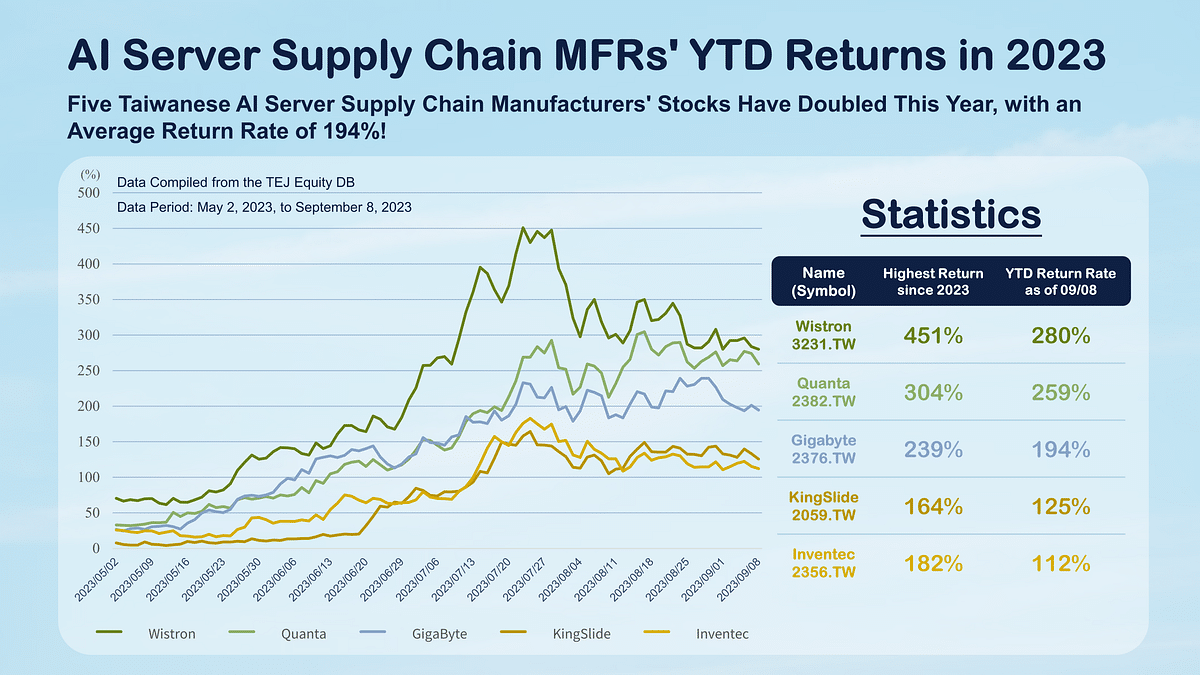

Stock Price of AI Server Supply Chain Companies

Even more notably, the robust sales of AI server products have propelled significant increases in the stock prices of five Taiwanese server manufacturers: Wistron, Quanta, Gigabyte, Inventec, and Mitac. This has triggered investment institutions to consistently elevate the price-to-earnings ratios of companies associated with these concepts, indicating optimism about future growth.

AI Server Supply Chain MFRs. YTD Returns in 2023. Source: TEJ Market Dataset

How Hot is the AI? Let the Export Figures Speak

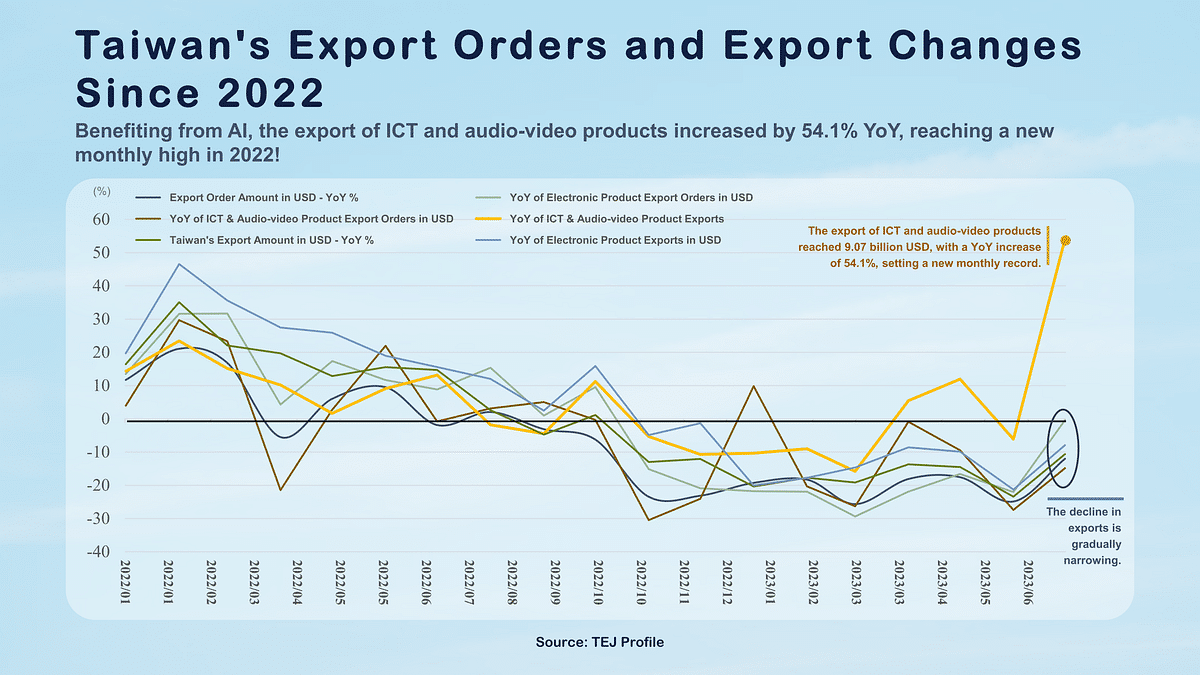

As per the latest forecast by the Department-General of Budget, Accounting, and Statistics (DGBAS) on August 18, 2023, Taiwan’s economic growth for the year is anticipated to be a modest 1.16%. This projection is influenced by four key factors: global inflation and pressure for interest rate hikes, subdued terminal demand, sustained destocking by enterprises, and a high base period. The annual export forecast for 2023 is expected to be -9.51%, with the export contribution to economic growth in the second quarter predicted to be -4.72%. Additionally, on August 21, 2023, the Ministry of Economic Affairs’ statistics revealed that Taiwan’s export order value for July 2023 was $47.73 billion, marking a 12% decrease compared to the same period last year, indicating an ongoing economic downturn.

However, examining electronic product categories, recent demand has been restrained due to the AI boom. Nevertheless, orders for chips, memory, IC design, and related sectors remain relatively stable. In July 2023, orders amounted to $17.71 billion, representing only a marginal 0.4% decrease from the same period last year. Furthermore, in the information and communication product category, including laptops and network communication products, though there is a performance downturn, the negative growth in orders has started to taper off. The Ministry of Finance also emphasized that, benefiting from the demand in the AI industry, the export growth rate of information and communication products turned positive in July at 54.1%, reaching a 13-year monthly high, as illustrated in the table below.

Taiwan’s Export Orders and Export Changes Since 2022. Source: TEJ Economic Dataset

Relying solely on the sales of AI products may not be enough to uplift the overall annual export growth. However, when considering individual industries’ export orders or exports, what can be asserted is that the long-term outlook for the AI industry is promising and forward-looking. The prospects for Taiwan’s related supply chain orders remain favorable, with optimistic expectations that companies may start reaping substantial benefits from the AI industry as early as the fourth quarter of this year.

The presented data indicates that AI products stand out as one of the few categories this year unyielding to economic headwinds, with a definite increase in overall sales. However, as investors, how can we pinpoint Taiwanese supply chain companies that are likely to benefit more from the AI industry amid the vast landscape of enterprises? The key to this answer is actually concealed within the company’s “production and sales mix.”

Why is the Company’s Production and Sales Mix Important?

While a company’s revenue and earnings performance is a point of interest for investors, delving further into a company’s prospects, the more crucial information is often hidden in the changes within the company’s production and sales mix. To achieve long-term sustainable operations, companies need to diminish reliance on a single product and pivot towards diversified development or entry into specific industries and product domains. Vigilantly monitoring the development of new business and the transformation of existing business is a key concern. Through the examination of annual reports and financial statements of publicly listed and over-the-counter companies, we can obtain detailed information about the company’s production and sales, including output value, sales volume, product structure, and the proportion of business departments.

A deep understanding of production and sales mix data allows us to explicitly identify which products or departments serve as the sources of the company’s profitability. The following sections will individually scrutinize the changes in the production and sales mix of Nvidia, King Slide, and Wistron, exploring whether AI products have initiated operational shifts within these companies.

Analyzing Nvidia & Taiwan’s Supply Chain through Production and Sales Mix

Nvidia — The King of Generative AI

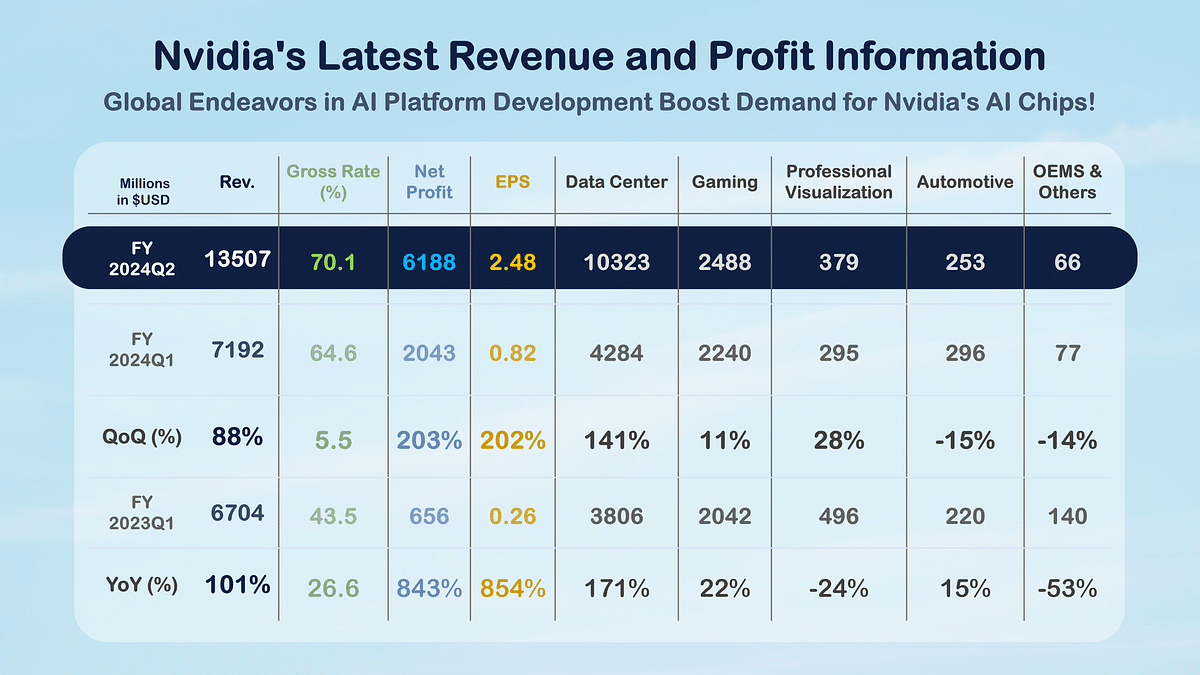

Nvidia’s performance in the second quarter financial report is exceptionally outstanding. The table below illustrates the operating data for Nvidia in the recent three quarters, categorized by company and various departments. Nvidia classifies its revenue by department, encompassing Data Center, Gaming, Professional Visualization, Automotive, and Other (OEM).

Nvidia’s Latest Revenue and Profit Information. Source: Nvidia

As shown in the table, Nvidia achieved a remarkable revenue of $13.507 billion in the second quarter of the FYQ2 2024, surpassing Intel’s $12.9 billion. The significant increase in Q2 revenue is largely attributed to the Data Center department, contributing $10.323 billion. The primary reason for this high performance is the considerable surge in sales of new products under the Data Center, namely the A100/H100 and A800/H800 GPU chips. In comparison, the performance of other departments is less notable, with segments like OEM or the Automotive department exhibiting a decline, reflecting poor terminal demand. Moreover, based on Nvidia’s Q2 financial report and forecasts for Q3 revenue, it is evident that major global companies or institutions are actively establishing their AI computing platforms. The current market has witnessed a substantial increase in demand for Nvidia’s AI series chips, indicating a promising outlook for Nvidia in the upcoming quarters.

King Slide — Servers Can’t Be Without Rails

King Slide’s primary products include rails, slides, and hinges, with the main source of revenue coming from King Slide Works and its subsidiary, King Slide Technology. As depicted in the table below, during the period from 2018 to 2022, the company’s flagship product remained glide rails, constituting over 95% of the company’s annual sales, with server rails contributing to 76% of the revenue proportion in 2022.

In essence, server drawer rails are devices that enable servers to be pulled out like drawers during maintenance. It’s noteworthy that the weight of AI servers can exceed a hundred kilograms, necessitating special drawer rails for support, and the gross profit margin of such rails is generally favorable. King Slide’s subsidiary, King Slide, specializes in the production of server drawer rails. In 2022, King Slide’s market share in server rails globally was approximately 30%.

For 2022, King Slide’s total revenue reached 7.798 billion NTD, with a YoY growth rate of 22.97%. The primary contribution came from the King Slide department, with its revenue growing by 35.93%. The profitability of this department also saw an improvement, with the profit margin increasing from 48.6% to 54.49%. Furthermore, the unit gross profit margin of rails increased from 54.15% in 2018 to 61.58% in 2022. The EPS in 2022 reached 42.56 NTD, as illustrated in the table below.

KingSlide Latest Production and Sales Mix and Departmental Revenue. Source: TEJ Financial Dataset

Even though the company explained during the corporate briefing on August 7, 2023, that the substantial demand for AI servers, driven by generative AI, has led to significant orders for new types of rails, estimating a market share of 50%. However, as indicated in the table above, the revenue growth of various departments at King Slide in the first half of this year has shown a decline. The subsequent impact of AI servers on the operation still needs to be observed after the fourth quarter of 2023.

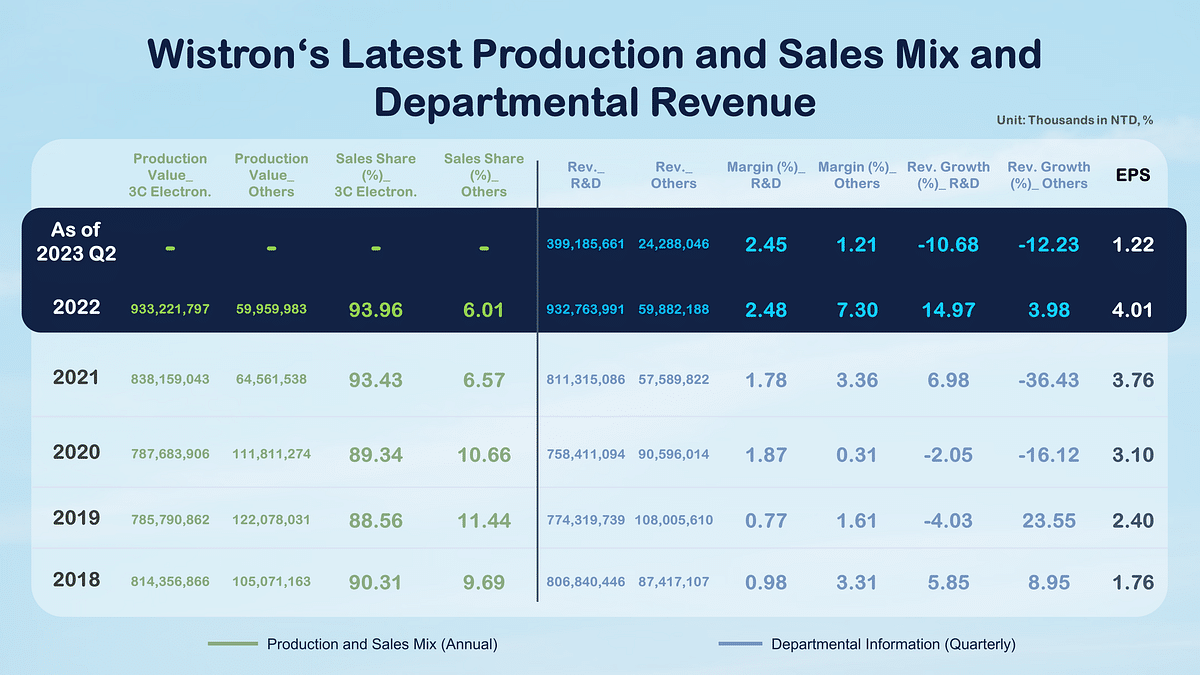

Wistron — One of the Key Indicators in AI Server

Wistron is the third-largest notebook computer manufacturer globally, focusing on offering ODM services to brand customers covering various products such as notebooks, desktop computers, servers, and smartphones. Since 2017, Wistron has actively engaged in the research and development of AI hardware, including GPU servers and GPU acceleration cards. This strategic move places Wistron at the forefront of the flourishing AI industry. In 2022, Wistron’s consolidated revenue reached 984.619 billion NTD, with a YoY growth rate of 14.2%, a gross profit margin of 7.1%, and an EPS of 4.01 NTD. Server revenue reached 15 billion USD, contributing to 36% of the total, with an 8% YoY increase. As illustrated in the figure below:

Wistron’s Revenue Share by Product for 2021–2022. Source: TEJ Financial Dataset

As observed in the above figure, among the revenue contributions of various products, servers exhibit notable performance, largely attributed to its key subsidiary, Wiwynn. Wiwynn is primarily involved in the data center product business, with major clients such as Meta and Microsoft, accounting for up to 90% of Wiwynn’s revenue. In 2022, Wiwynn initiated the shipment of AI-related servers, significantly contributing to Wistron’s overall revenue. Considering Wistron’s existing partnership as a collaborator for Nvidia DGX and HGX servers, all these factors have propelled Wistron to receive such high market attention in this current wave of AI trends.

Wistron’s Latest Production and Sales Mix and Departmental Revenue. Source: TEJ Financial Dataset

Tracking Wistron’s recent status, the consolidated revenue for the first half of 2023 amounted to 419.477 billion NTD. Judging from the revenue of the company’s departments, they are currently in a declining phase. However, according to Wistron’s presentation in this year’s corporate briefing, the company remains optimistic about the demand for AI servers driven by ChatGPT. It estimates that the revenue proportion of servers in 2023 will increase from 36% in 2022 to 38%. The future contribution to Wistron’s operations awaits further observation.

Through the examples mentioned above, it’s clear that a company’s product mix and departmental structure significantly impact its growth and profitability. Every industry encounters growth stagnation, and industry evolution is not an overnight or yearly transformation. Investors can glean insights from the historical trajectory of changes in the company’s product mix to understand the management’s decision-making direction and its sensitivity to the industry. Furthermore, by examining the company’s new business ventures, we can discover the next mainstream industry.

Organizing the Revenue Share of AI Servers

Moreover, TEJ has assisted in organizing the expectations of research institutions and institutional entities regarding future AI products and supply chain companies. The data is as follows.

According to the estimates from TrendForce, the total shipments of AI servers in 2023 are expected to be around 1.2 million units, with a YoY growth rate of 38.4%. Among them, servers equipped with GPUs will become mainstream, accounting for approximately 60% to 70% of the shipments. Currently, the shipment proportion of AI servers this year has not yet reached 10% of the overall server market. However, it is expected to reach 15% by 2026, and from 2022 to 2026, the shipment volume of AI servers is projected to continue growing at a compound annual growth rate of 22%. Additionally, considering the trend of AI applications, foreign analysts predict that the average compound annual growth rate of AI opportunities from 2023 to 2030 will reach 37%.

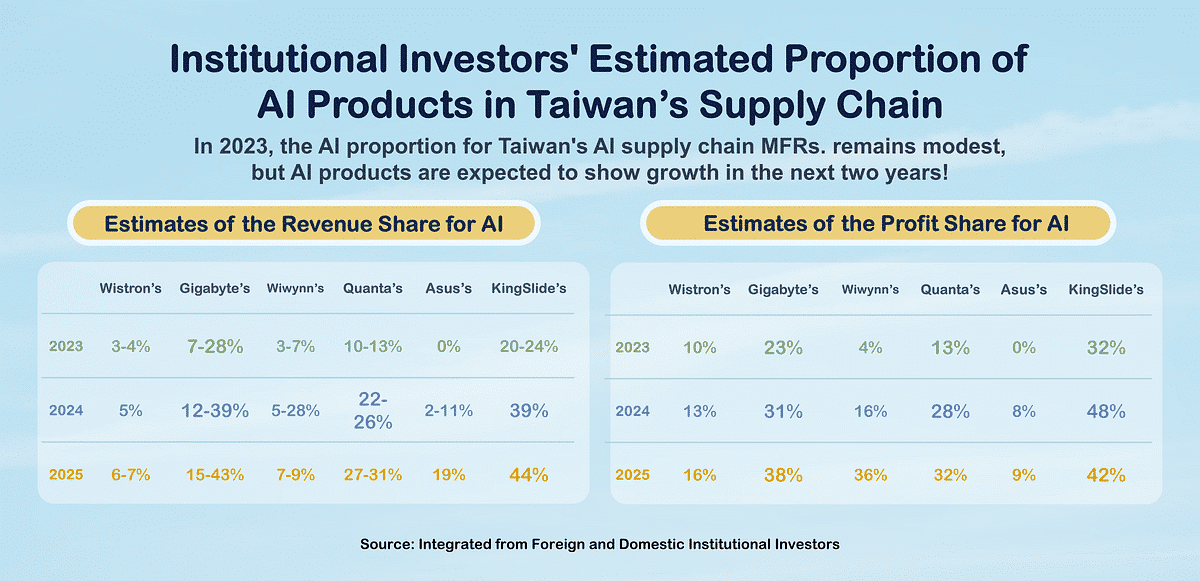

The table below presents the predictions of the future three-year AI revenue and profit proportions for some AI server manufacturers’ supply chains from foreign and domestic institutional entities. From the information in the table, it is evident that, except for King Slide, although the contribution of AI products to the revenue and profit of other companies has not yet significantly materialized this year, AI products are still expected to exhibit growth in the next two years. It is also anticipated that by 2025, the proportion of AI products in revenue and profit will rise to a certain level.

Institutional Investors Estimated Proportion of AI Products in Taiwan’s Supply Chain. Source: Integrated from Foreign and Domestic Institutional Investors

Conclusion

From the company’s product mix and overall economic data, it is evident that generative AI is an emerging industry entering a period of rapid growth. The market holds an optimistic view of the prospects of generative AI over the next decade, and this sentiment is reflected in the stock prices of related supply chain companies. Looking ahead, there is a general expectation in the market that the trend of destocking in the fourth quarter of this year will bottom out, and AI-related supply chain companies will be able to sequentially increase the shipment volume of AI products, making substantial contributions to their revenue. In conclusion, through the brief introduction in this article, we hope to provide readers with a preliminary understanding of the company’s product mix and insights, enabling them to identify potential investment opportunities in the changing product mix.

TEJ TAIWAN DB → TEJ Company DB→ Sales Break Down & Department Information… Access the latest company production and sales mix data through the TEJ Company DB, keeping you up-to-date with companies’ changes!

If you have any questions about this article or want to obtain further access to the TEJ database, please feel free to leave a comment, call, or mail us.

Your encouragement drives us to continue sharing more on TEJ Dictionary! If you think this article is helpful, click the clap button until it hits 50. You can also leave a comment and share any ideas with us.