Table of Contents

Printed Circuit Board (PCB), the indispensable core component of all electronic products, has cemented Taiwan as the hub of the global PCB industry. However, in the face of changing supply chain dynamics due to the US-China trade tensions and recent economic sanctions, the issue of whether PCB manufacturers will move their production capacities from China to other countries has resurfaced. Has Taiwan’s PCB industry shifted its production to Southeast Asia to mitigate geopolitical risks? In this article, we’ll delve into the development of the PCB industry, Taiwan’s PCB export trends, and analyze the impact of geopolitical factors on the migration of Taiwan’s PCB manufacturers in the past five years.

In 1925, Charles Ducas printed circuit diagrams on an insulating substrate using electroplating as a conductor for wiring. The term “Printed Circuit Board” was officially coined, but it couldn’t be commercialized due to immature technology at the time. It wasn’t until 1947 to 1950, with the advent of the transistor, that the PCB industry rapidly developed, and advanced countries such as Europe, the United States, and Japan entered the mass production stage. However, the manufacturing process produced many complex pollutants, and the added value was low, resulting in low profits. To reduce production costs, foreign electronic manufacturers chose to set up factories in developing countries with low labor costs and looser environmental regulations, creating a new international division of labor. Therefore, Taiwan has begun to sprout at that time.

Taiwan’s printed circuit board (PCB) industry began to take root in 1969 with the establishment of a plant by Ampex. At the time, Taiwan was in a period of export expansion, with the government actively promoting policies and incentives to attract foreign investment and offering advantages such as a stable social environment, low-cost labor, and lenient environmental policies — all of which created an attractive emerging market for development and investment. As foreign investment poured in, a chain of supply gradually developed and formed a thriving industry chain. Moreover, in 1980, HP moved its PCB manufacturing to Taiwan and invited Nan Ya Plastics to become a partner, planting the seeds for Taiwan’s current position in the tech industry.

Following the dot-com bubble and the 9/11 attacks, the global economy experienced a severe downturn, with European and American businesses suffering the most significant losses. This had a severe impact on Taiwan’s economy, resulting in a dramatic drop in growth rate from 5.8% in 2000 to 1.7% in 2001, and the PCB industry entered a period of decline for the first time. Moreover, the 2003 SARS outbreak led to a sharp decline in demand for electronic devices, and the semiconductor industry was hit hard. In 2004, Typhoon severely damaged northern Taiwan, causing a water shortage that lasted for three weeks, and PCB manufacturers have been affected once again, with many small and medium-sized enterprises going bankrupt.

After facing cutthroat competition and natural disasters, European and American corporations withdrew from the PCB market and required suppliers to establish overseas branches. China’s advantages in low labor costs, a huge domestic market, and easy access to land made it highly sought-after. Taiwanese PCB factories gradually moved their production lines to China, laying the foundation for China’s future as a PCB production hub.

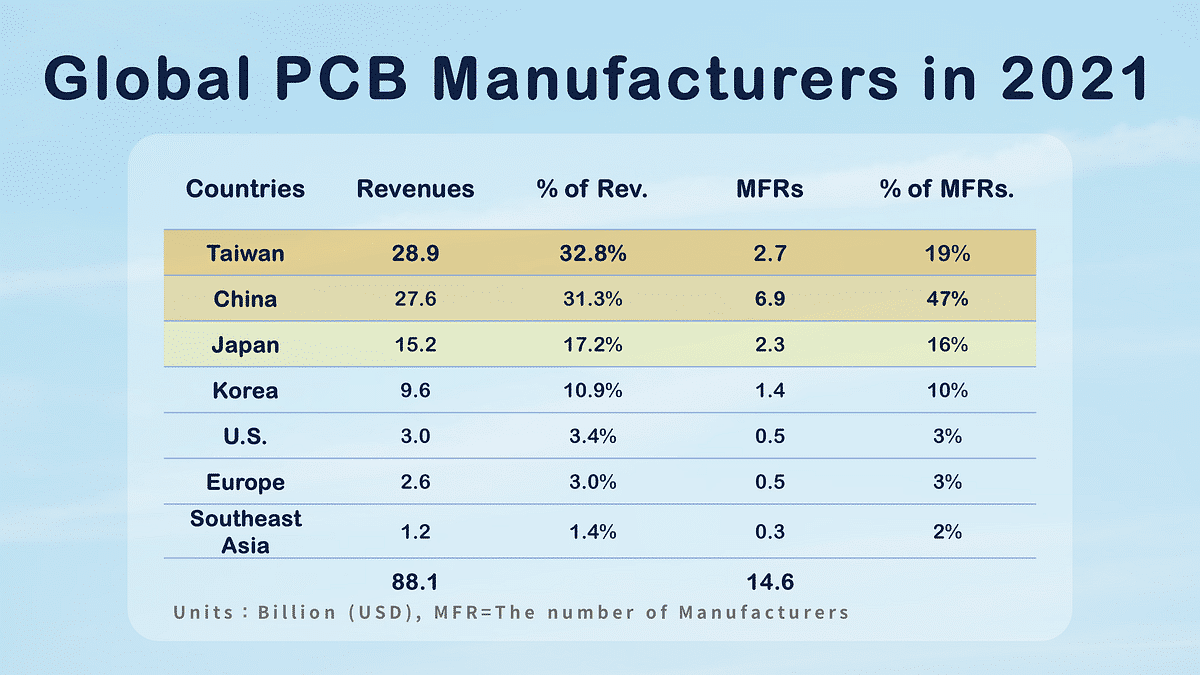

According to a survey from N.T. Information, the global PCB production value reached $87 billion in 2021. There are 146 PCB manufacturers with revenue exceeding $100 million, of which China has the most with 69 companies, followed by Taiwan with 27, and Japan with 23 respectively. Regarding revenue, Taiwan’s PCB industry holds the highest global market share of 32.8%, ranking first, followed by China with 31.3% and Japan with 17.2%.

Taiwan’s PCB industry has been deeply rooted for nearly 50 years, establishing the world’s most powerful PCB cluster. However, in recent years, the Chinese government has actively supported Chinese manufacturers to expand production capacity, narrowing the gap in production value with Taiwan, which was only 1.5% in 2021.

But how can Taiwan’s 27 PCB manufacturers create the world’s highest revenue market share? It’s due to their successful efforts in developing high-end PCB products and their strong technological advantage in PCB fabrication. The industry chain is still robust!

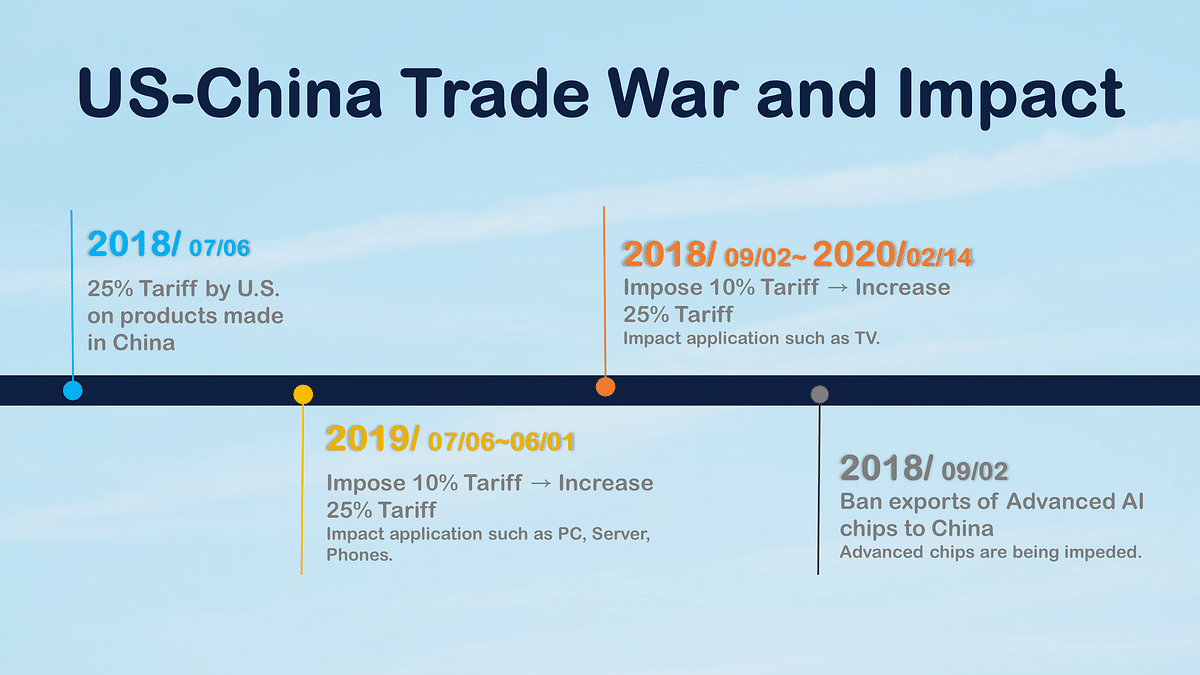

The above history has an important point that has not been mentioned yet. In August 2017, the Office of the United States Trade Representative initiated an investigation against China for allegedly violating U.S. intellectual property rights and launched a series of trade conflicts. As the U.S.-China trade tensions intensified, the U.S. imposed tariffs on goods imported from China and placed Chinese companies on an export control list, causing changes in the global supply chain. The timeline of the U.S.-China trade war and its impact on end applications are summarized in the following chart:

Stay ahead of the curve with TEJ Industry Analysis!

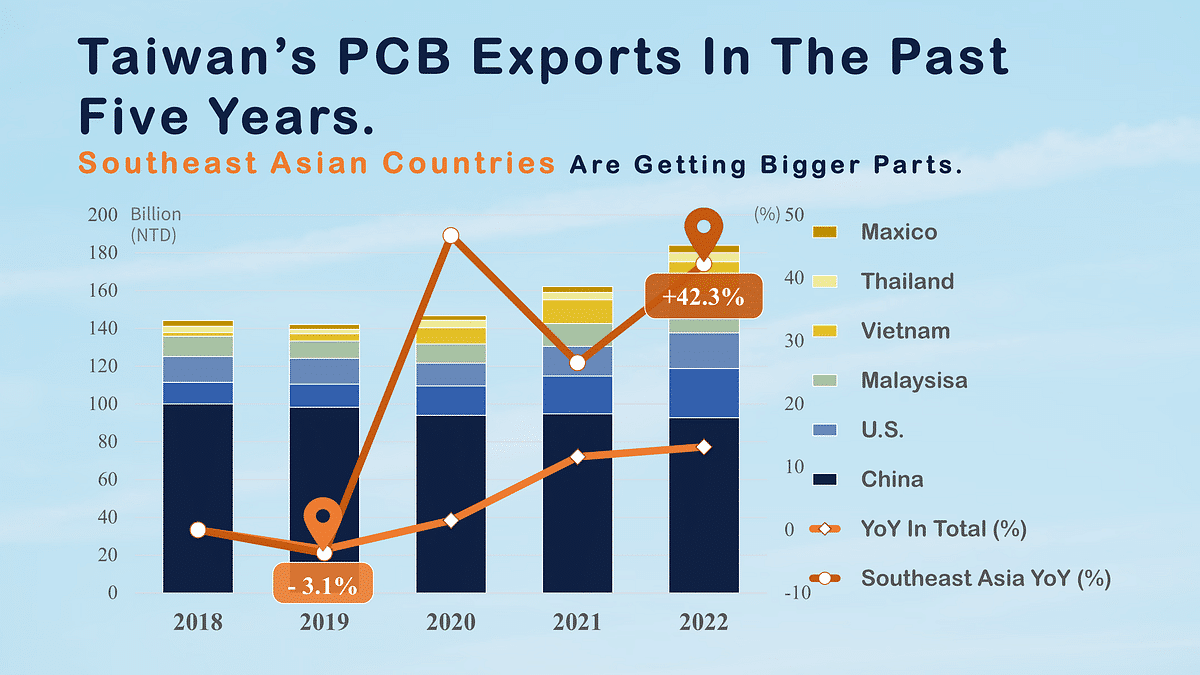

Taiwan’s PCB industry mainly relies on an export-oriented production model, and changes in export markets are crucial for the industry as a whole. According to Taiwan Trade Statistics, there was a 3.1% decrease in 2019, the only negative growth in the past five years. However, from 2020 to 2022, the industry benefited from the pandemic-induced surge in remote working, as well as incentives from applications such as automotive electronics, 5G communications, and AI cloud services, resulting in a shift from negative to positive growth rates.

Furthermore, from 2020 to 2022, the proportion of exports to China decreased gradually from 60.1% to 51.2%, while the proportion of exports to other regions showed an increasing trend, including South Korea and Southeast Asian countries. China has had a strong development in the PCB field due to various policy incentives in recent years. However, affected by the restructuring of the supply chain due to the US-China trade dispute, Taiwan has gradually shifted its export focus from China to overseas regions, with Southeast Asia being the most active. The average growth rate in 2022 was 42.3%, while Mexico also grew by 39.0%.

In summary, influenced by the US-China trade war, the production distribution of PCBs in the past five years and Taiwan’s export situation have shown a trend of moving towards Southeast Asia, especially in 2022. Therefore, the next chapter will delve into the expansion and relocation of manufacturers in the past five years to explain this trend.

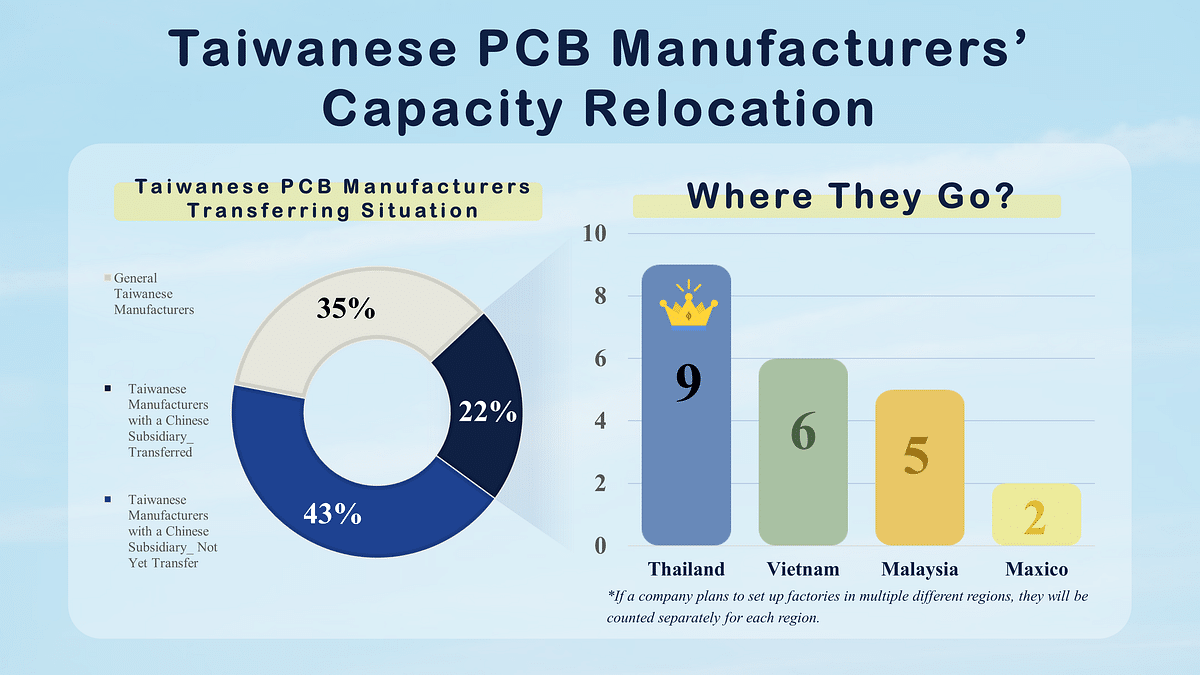

This study focuses on the number of companies whose revenues or non-current assets located in China account for more than 25% of their revenue (Taiwanese Manufacturers with Chinese Subsidiaries). The results show that there are up to 42 companies with high production capacity in China. Among them, it was found that 28 companies have not shown signs of production capacity migration, accounting for 43% of the total number of companies. The remaining 14 companies have shown signs of industry migration, accounting for 22% of the total number of companies.

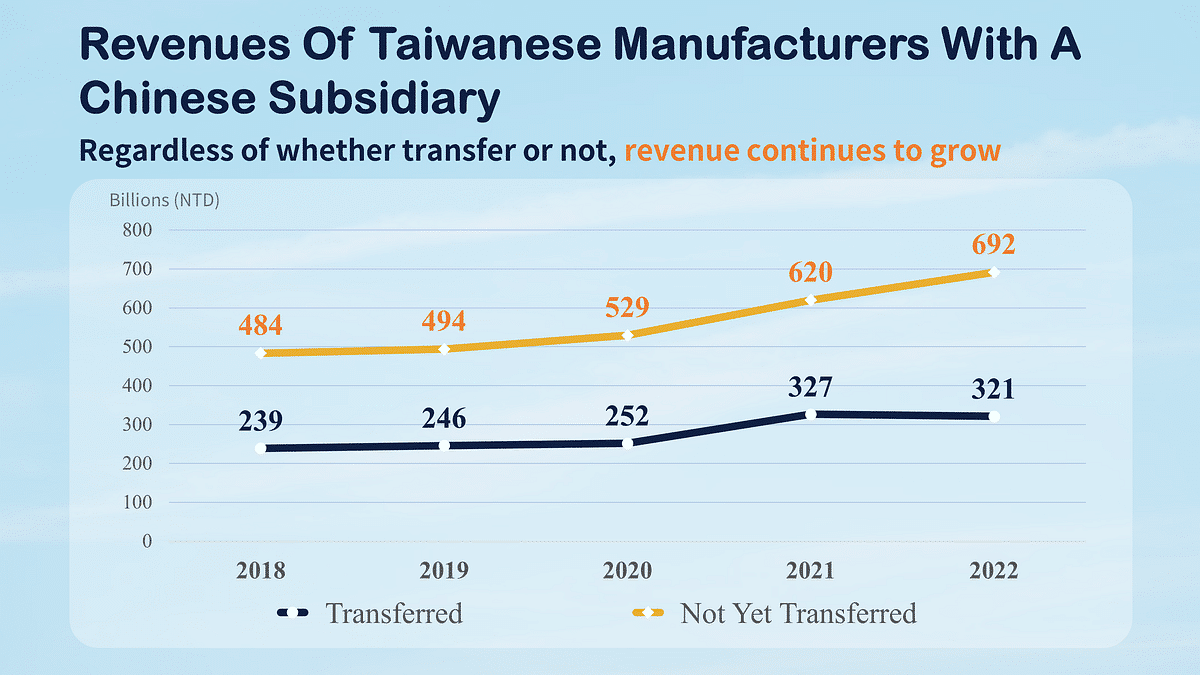

In addition, by observing the changes in revenue from 2018 to 2022, it was found that Taiwanese Manufacturers with Chinese Subsidiaries showed an upward trend in revenue growth, regardless of whether they had signs of transferring their China-based production capacity. This indicates that the impact of the 25% tariff imposed by the US had a relatively small effect on the printed circuit board industry.

Regarding transfer motivation, around 80% is due to meet customer demand, mostly after 2022. Even though the US-China trade war initially had little impact on Taiwanese PCB companies, recent geopolitical tensions have still led to a shift toward production relocation.

Taiwan’s export focus has shifted to countries such as Thailand, Vietnam, Malaysia, and Mexico. The reasons why each country attracts investment are:

As the ongoing trade war between the US and China continues, the latest US restrictions not only prohibit the export of advanced chips and equipment, but also forbid other countries from selling products with US-related technology to China. Downstream manufacturers are taking measures to resist “Made in China” in order to prevent the ban. For example, Dell plans to stop using chips produced in China by the end of 2024 and has informed its suppliers to significantly reduce their use of “Made in China” components. If the US ban on China continues to expand, it may lead to a repeat of the serious disruption of the global supply chain that occurred 30 years ago. In recent years, Taiwanese printed circuit board (PCB) manufacturers have gradually been required to expand globally. Depending on the strength of customer demand, the transfer of Chinese production capacity overseas will be affected.

In conclusion, the trend of relocation is already quite evident. However, we still need to pay attention to the trends in the relocation of production lines for Taiwan’s PCB manufacturers in the coming years!

About us

⭐️ LinkedIn

✉️ E-mail: tej@tej.com.tw

☎️ Phone:+886-2-87681088