Table of Contents

The Zipline engine, integrated within TQuant Lab, offers a high-quality and realistic backtesting framework. It leverages four core functions—initialize、handle_data、analyze、run_algorithm——to construct a comprehensive simulation environment. These components enable trading strategies to dynamically adjust to market conditions, incorporating elements such as slippage and transaction costs to ensure that backtest results closely reflect real-world performance.

This article begins with a brief overview of the four key components and their applications. It then focuses in detail on the initialize function, exploring its specific configurations and role within the backtesting process.

The initialize function serves as the starting point of any trading strategy within Zipline and plays a critical role in configuring the backtesting environment. Common settings defined here include slippage models, commission fees, the target security, and the benchmark index. This function is executed once at the beginning of the backtest.

The initialize function takes a single parameter, context, which acts as a persistent storage object for custom variables. These variables can be accessed and updated on each trading day during the simulation. For example, one might define context.day = 0 to count the number of trading days elapsed, and context.has_ordered = False to track whether a position in TSMC stock has been initiated.

In addition, the functions set_slippage() and set_commission() can be used within initialize to define slippage behavior and commission cost models, respectively. These configurations will be briefly discussed later in this article.

from zipline.api import set_slippage, set_commission

from zipline.finance import slippage, commission

def initialize(context):

context.day = 0

context.has_ordered = False

set_slippage(slippage.FixedSlippage())

set_commission(commission.PerShare(cost=0.00285))

The handle_data function is responsible for defining the trading logic, executing orders, and recording relevant trading information. It is called once per day throughout the backtesting period after the simulation begins.

This function takes two parameters: context and data. The context parameter serves the same purpose as in initialize—it stores custom variables that persist across trading days and can be updated or referenced during the backtest. The data parameter provides access to daily price and volume information for each asset. For example, data.current() can be used to retrieve the current day’s open, high, low, and close prices, while data.history() allows access to historical price and volume data.

In addition, the record function can be used within handle_data to track specific values across trading days. These recorded values will appear as columns in the final output DataFrame generated by run_algorithm.

Below is an example of how this function can be implemented:

record( ‘column_name’ = value)

As an example, consider a simple strategy in which we place an order to buy 1,000 shares of TSMC (ticker: 2330) and hold the position until the end of the backtest. In this case, we record three key elements during each trading day: the number of trading days elapsed (context.day), whether the position has already been initiated (context.has_ordered), and the current closing price retrieved via data.current(symbol(“2330”), “close”).

Within the handle_data function, Zipline supports six different order functions to place trades. A detailed explanation of the first four methods will be provided in the next section of this series.

from zipline.api import order, record, symbol

def handle_data(context, data):

context.day += 1

if not context.has_ordered:

order(symbol("2330"), 1000)

context.has_ordered = True

record(

trade_days = context.day,

has_ordered = context.has_ordered,

TSMC = data.current(symbol("2330"), "close")

)

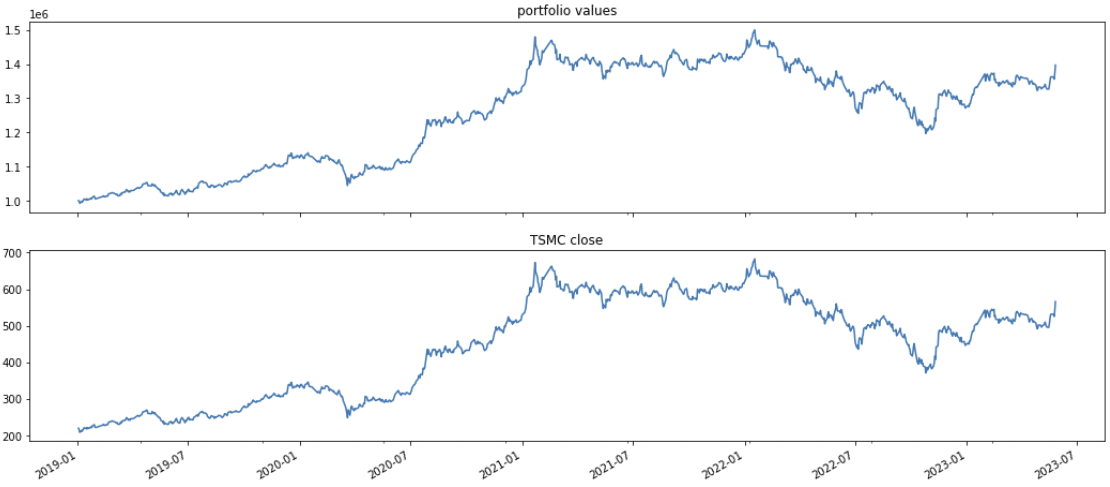

The analyze function is primarily used for visualizing backtest results, helping users evaluate strategy performance and risk management outcomes. It is called once at the end of the backtest process.

This function takes two parameters: context and perf. The context object serves the same role as described in the initialize section, while perf refers to the output DataFrame generated by run_algorithm. This DataFrame contains a variety of recorded performance metrics and can be used to extract specific columns for plotting and analysis.

As an example, we can use Matplotlib to visualize the portfolio value over time and compare it with the price trend of TSMC (2330). A more detailed discussion of how to use the analyze function will be covered in a later section of this series.

import matplotlib.pyplot as plt

def analyze(context, perf):

ax1 = plt.subplot(211)

perf.portfolio_value.plot(ax=ax1,title='portfolio values')

ax2 = plt.subplot(212, sharex=ax1)

perf['TSMC'].plot(ax=ax2,title='TSMC close')

plt.gcf().set_size_inches(18, 8)

plt.show()The run_algorithm function is the core entry point for executing a backtest and serves as the primary trigger for running a trading strategy.

This function accepts multiple parameters and includes several built-in fields that allow users to configure the backtest environment in detail. A comprehensive explanation of these parameters and their applications will be provided in a later section of this series.

Example Code:

from zipline import run_algorithm

import pandas as pd

start_date = pd.Timestamp('2018-12-30',tz='utc')

end_date = pd.Timestamp('2023-05-26',tz='utc')

results = run_algorithm(start= start_date,

end=end_date,

initialize=initialize,

capital_base=1e6,

analyze=analyze,

handle_data=handle_data,

data_frequency='daily',

bundle='tquant'

)

After introducing the four core components of the backtesting framework, we now turn to a detailed explanation of the initialize() function—its parameters and practical usage.

One of its most common applications is to set slippage and commission models, which help ensure that backtest results better reflect real-world market conditions. Additionally, custom variables and parameters can be defined within initialize() to store and manage trading-related information throughout the simulation.

The set_slippage() function is used to define the slippage model. Zipline supports the following four types of slippage models:

| Slippage Models | Explanation |

| FixedSlippage | Simulates transaction costs by applying a constant bid-ask spread. This model does not account for volume constraints. |

| VolumeShareSlippage | Calculates slippage based on the proportion of the trade volume relative to the asset’s total daily volume, incorporating market impact. |

| FixedBasisPointsSlippage | Applies a fixed number of basis points to each trade, with the option to set volume limits to reflect liquidity constraints. |

| NoSlippage | Assumes trades are executed at market prices without any slippage applied. |

The set_commission() function is used to define the commission model. Zipline provides several methods for calculating transaction costs, including:

| Commission Models | Explanation |

| NoCommission | No transaction fees are charged. This setting is typically used in simulation environments or promotional programs. |

| PerDollar | Commission is calculated as a fixed rate applied to the total trade value. For example, a fee of 0.0015 is charged for every NT$1 traded. This is Zipline’s default setting. |

| PerTrade | A fixed fee is charged per transaction, regardless of the trade size or value. The default is NT$0. |

| Custom_TW_Commission | Taiwan Equity Market Commission Model (Tailored for local regulations): This model includes two direct costs: brokerage commission (0.1425%) and securities transaction tax (0.3%) and allows for setting a minimum fee (default: NT$20). 1. transaction fee • Applies to both buy and sell orders. • Formula: Trade Price × Number of Shares × 0.1425% × Discount (Discount defaults to 1, meaning no discount applied) • A minimum commission (default NT$20) is enforced. 2. Securities Transaction Tax • This only applies to sell transactions. • Formula: Trade Price × Number of Shares × Tax Rate (Default tax rate: 0.3%) |

Example Code:

from zipline.api import set_commission

from zipline.finance import commission

def initialize(context):

set_slippage(slippage.<slippage models>)

set_commission(commission.<commission models>)

context is a namespace object used to store user-defined variables and parameters. These variables persist throughout the backtest and can be accessed or updated on each trading day.

For example, we may define a variable to track the number of trading days elapsed and another to record whether the strategy has already placed an order for the target stock:

Example Code:

from zipline.api import set_slippage, set_commission

from zipline.finance import slippage, commission

def initialize(context):

context.day = 0

context.has_ordered = False

set_slippage(slippage.FixedSlippage())

set_commission(commission.PerShare(cost=0.00285))

You can also define a list of stock tickers to be traded and convert them into Zipline-recognizable Asset objects, which simplifies subsequent order placement. In addition, you can specify a custom benchmark for performance comparison.

Example Code:

from zipline.api import set_slippage, set_commission

from zipline.finance import slippage, commission

def initialize(context):

context.tickers = ['1101', '2330']

context.asset = [symbol(ticker) for ticker in context.tickers]

set_slippage(slippage.FixedSlippage(spread=0.00))

set_commission(commission.PerDollar(cost=commission_cost))

set_benchmark(symbol('IR0001'))

Important Reminder: This analysis is for reference only and does not constitute any product or investment advice.

We welcome readers interested in various trading strategies to consider purchasing relevant solutions from Quantitative Finance Solution. With our high-quality databases, you can construct a trading strategy that suits your needs.

“Taiwan stock market data, TEJ collect it all.”

The characteristics of the Taiwan stock market differ from those of other European and American markets. Especially in the first quarter of 2024, with the Taiwan Stock Exchange reaching a new high of 20,000 points due to the rise in TSMC’s stock price, global institutional investors are paying more attention to the performance of the Taiwan stock market.

Taiwan Economical Journal (TEJ), a financial database established in Taiwan for over 30 years, serves local financial institutions and academic institutions, and has long-term cooperation with internationally renowned data providers, providing high-quality financial data for five financial markets in Asia.

With TEJ’s assistance, you can access relevant information about major stock markets in Asia, such as securities market, financials data, enterprise operations, board of directors, sustainability data, etc., providing investors with timely and high-quality content. Additionally, TEJ offers advisory services to help solve problems in theoretical practice and financial management!

Within the initialize() function, we can configure key components such as slippage, commission model, tradable assets, and the benchmark index. Additionally, the context object serves as a central storage for tracking the trading state, ensuring that the backtest executes smoothly and systematically.