Written by Professor Wan-Ying Lin of the Department of Accounting, National Chengchi University

Table of Contents

Financial institutions are major providers of corporate debt financing. Lending conditions affect not only banks’ own interests, but also companies’ funding costs and operations. The World Economic Forum (WEF) notes that green finance supports both environmental protection and sustainable development. Driven by the growing momentum of ESG, banks have actively implemented green finance initiatives by incorporating corporate ESG performance into their lending decisions. The Bankers Association of the Republic of China has also incorporated elements of the Equator Principles 4.0, introduced in 2020, into its credit guidelines for member banks. Through financial mechanisms, banks encourage borrowers to place greater emphasis on environmental, social, and corporate governance issues, promote sustainable industrial development, and work toward carbon reduction targets.

If banks only lend to companies with strong ESG performance, the limited number of eligible firms may affect banks’ economic returns. Therefore, while pursuing sustainability goals, banks should consider not only companies’ financial conditions, but also how their ESG performance aligns with credit risk and lending decisions.This raises an important question: when banks promote green finance, do they truly include ESG factors in loan approval decisions, and how do they measure the connection between corporate financial performance and ESG outcomes?

¹ According to an initial analysis by Hsiao et al. (2025), among Taiwanese listed and OTC companies from 2015 to 2020, the average share of companies compiling and providing standalone CSR/ESG reports was 29.42%, or nearly 30%.

Recent domestic academic research on CSR/ESG includes the study by Hsieh, An-Xuan , Lin Wan-ying, and Cheng Kuei-hui (2025). Using TEJ’s TESG Sustainable Development Ratings, the study measures corporate ESG performance and incorporates variables such as credit rating, risk, corporate governance, and firm characteristics to examine the relationship between ESG performance and bank lending conditions, including loan spreads, loan size, loan maturity, and whether collateral is provided. The study received awards including the Best Paper Award at the 2023 Taiwan Accounting Association Annual Conference and the 14th Yuanta Golden Diamond Award. If you are interested in reading the full study,👉please click the reference link.

Hsieh et al. (2025) find that better ESG performance helps companies obtain more favorable lending conditions. The economic effect of ESG performance is most significant on loan amounts, followed by the likelihood of providing collateral, loan maturity, and loan spreads. In addition, companies with stronger financial performance show a clearer relationship between ESG performance and bank lending terms. Abnormally high or low ESG performance does not bring additional benefits in securing better loan conditions; instead, lending conditions tend to be weaker. The additional tests are broadly consistent with the main results.

This study provides preliminary empirical evidence on the relationship between corporate ESG performance and bank lending costs in Taiwan, helping clarify the economic consequences of ESG performance. Due to space limitations, this article briefly summarizes the research motivation and key findings of Hsieh et al. (2025).

For banks, ESG-related lending decisions must still balance returns and risks. A company’s profitability supports its ability to repay principal and interest. Therefore, as long as credit risk is acceptable and repayment ability is sound, banks may provide financing regardless of the borrower’s ESG performance. However, to comply with regulations and fulfill their broader mission, banks must also consider the impact of environmental, social, and governance factors.

Hsiao et al. (2025) argue that, amid the institutional push for green finance, it is important to examine whether banks’ lending decisions have shifted from focusing mainly on borrowers’ financial performance to also considering ESG performance. The study therefore explores three key questions:

Prior research suggests that companies with higher CSR/ESG disclosure tend to show more stable long-term financial performance(Friede, Busch and Bassen 2015) , obtain funding from third parties under better terms(Goss and Roberts 2011) , and enjoy lower debt financing costs(Raimo, Caragnano, Zito, Vitolla and Mariani 2021; Eliwa et al. 2021) . ESG and financial information are therefore both important determinants of debt financing costs.

Companies that better address stakeholder needs can lower financing costs(Preston and O’Bannon1997) , improve transparency, reduce information asymmetry(Garcia-Sánchez, Raimo, Marrone and Vitolla 2020) and credit risk( Atif and Ali 2021) , and ease customer constraints(Cheng, Ioannou, and Serafeim 2014; Hamrouni et al. 2019) . These factors may help firms obtain external financing under more favorable conditions(Raimo et al. 2021; He, Liu, and Chen, 2023) .

Therefore, ESG information can complement risk-related information and help reduce debt financing costs. Companies with stronger ESG performance are expected to receive more favorable bank lending conditions, including lower loan spreads, larger loan amounts, longer maturities, and no collateral requirement.

Banks follow the 5P principle in credit decisions to ensure credit rights and asset safety. In addition to requiring collateral, banks also consider borrowers’ risk, repayment ability, financial information, and profitability. ESG information provides additional risk insights. Ideally, banks should consider both ESG and financial performance. However,ESG initiatives often require substantial and long-term investment, making short-term benefits less visible. Companies may face limited resources and trade-offs, meaning that improving ESG performance may come at the expense of short-term profitability.(Cheng et al., 2023)

Both ESG information and financial information are important determinants of debt financing costs. However, previous studies have paid less attention to whether the relationship between ESG performance and lending conditions is influenced by corporate financial performance, especially as ESG disclosure becomes more common and banks are required to meet sustainability and green finance targets.

Hsieh et al. (2025) argue that when companies are unable to balance ESG and financial performance, lending banks may place greater weight on credit protection, profitability, and public-interest considerations. As a result, they may make trade-offs between non-financial ESG performance and financial performance when evaluating borrowers. Therefore, the study examines whether the relationship between ESG performance and bank lending conditions is affected by corporate financial performance.

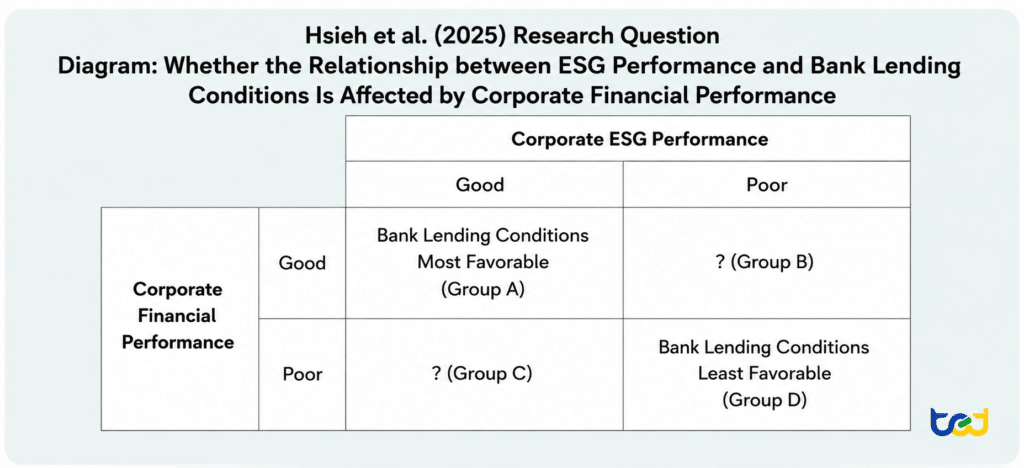

Figure 1. Research Framework for Research Question 2 in Hsieh et al. (2025)

According to Figure 1, a reasonable expectation is that companies with both strong ESG and financial performance Group A should receive the most favorable lending conditions. By contrast, companies with both weak ESG and financial performance Group D should receive the least favorable lending conditions. The more interesting question is whether banks treat companies differently when ESG and financial performance are inconsistent, as in Group B and Group C.

Normal CSR investment is part of corporate strategy and may help improve future operating performance. However, abnormal ESG investment may serve more as a reputation-building tool(Lys et al. 2015) . While it can enhance market recognition, it may not necessarily improve firm value or future financial performance, and may even create agency issues.

Although ESG investment can bring companies a positive image, excessive ESG investment may cause costs to exceed benefits, leading to resource waste, higher financial burden, weaker financial performance, and conflicts with shareholder interests.Conversely, insufficient ESG investment may increase corporate risk, thereby raising banks’ credit and reputational risks.

Therefore, abnormal ESG performance, whether higher or lower than expected, may be related to lending conditions, and this relationship may also be affected by corporate financial performance.

The following summarizes the findings of Hsieh et al. (2025) based on the research questions above.

Hsieh et al. (2025) find that bank lending decisions are influenced by corporate ESG performance. Specifically, companies with stronger ESG performance tend to receive lower loan spreads, larger loan amounts, longer loan maturities, and are less likely to be required to provide collateral. The economic significance is strongest for loan amount, followed by collateral requirement, loan maturity, and loan spread.

Hsieh et al. (2025) find that companies with both strong ESG and financial performance receive consistently more favorable lending conditions, while companies with weak performance in both areas receive less favorable terms. Holding other factors constant, firms with better ESG performance can still obtain better debt financing conditions than firms with weaker ESG performance, suggesting that ESG may help offset weaker financial performance.

Compared with firms that have weaker financial performance, firms with stronger financial performance show a stronger positive relationship between ESG performance and favorable lending conditions. In other words, the positive link between strong ESG performance and better lending terms is mainly driven by firms with strong financial performance.

For firms with mixed performance, companies with strong ESG but weak financial performance receive significantly better non-price lending terms than those with weak ESG but strong financial performance, although no significant difference is found in loan spreads.

Hsieh et al. (2025) find that companies with ESG performance above or below expectations, referred to as abnormal ESG performance, tend to receive worse loan spreads on incremental loans. Firms with ESG performance below expectations receive significantly less favorable lending terms than those with ESG performance in line with expectations.

When firms overinvest in ESG, banks may view this as increasing bankruptcy risk or agency conflicts, reflecting concerns over economic benefits. When firms underinvest in ESG, banks may see higher credit and reputational risks, resulting in generally weaker lending terms.

The relationship between abnormal ESG performance and lending conditions is also affected by financial performance. The negative effect of ESG overinvestment is mainly observed among firms with weaker financial performance, while the negative effect of ESG underinvestment is mainly observed among firms with stronger financial performance. In other words,companies with excessive ESG investment and weak financial performance receive worse lending terms; companies with insufficient ESG investment but strong financial performance also receive less favorable lending terms.

Hsieh et al. (2025) further conduct several robustness tests, including replacing variables, adding control variables, testing ESG sub-scores and firm-level analyses, examining individual ESG dimensions, and using cross-sectional analyses to assess whether the findings are consistent with the main results.

In the E, S, and G sub-score tests, the study finds that the Social score has the strongest impact on lending conditions, followed by Environmental and Governance performance. Cross-sectional tests show that companies issuing ESG reports, firms during the COVID-19 period, and borrowers with relatively poor ESG performance tend to receive better debt financing conditions. Sensitivity tests using different models and ESG rating measures also show results consistent with the main findings.

Under the influence of green finance, whether banks provide loans and how they set lending terms may affect both lenders’ and borrowers’ rights, returns, and costs. In addition to assessing borrowers’ financial condition and repayment ability, banks should also consider ESG-related risks and corresponding risk management measures. Non-financial information related to ESG risks can be obtained from increasingly complete ESG or CSR reports, giving banks a stronger rationale to evaluate both financial performance and ESG performance.

Hsieh et al. (2025) find that banks are more willing to provide favorable lending terms to companies with stronger ESG performance. These firms tend to receive lower loan spreads or no collateral requirement, while loan amount and maturity show no significant increase. The economic effect of ESG performance on lending conditions is significant, especially for loan amount.

In addition, financial performance has a moderating effect. Companies with stronger financial performance show a stronger relationship between ESG performance and favorable lending conditions. Firms with ESG performance above or below expectations tend to receive weaker lending conditions. Overall, the findings provide useful insights for regulators, companies, financial institutions, and the public.

Written by Professor Wan-Ying Lin|Associate Professor, Department of Accounting, National Chengchi University. Her research focuses on financial accounting, group governance, and ESG sustainability, with a long-standing interest in the quality of corporate information disclosure and its practical development.

TEJ’s TESG Rating evaluate companies’ their performance and disclosure depth across the three ESG pillars: environmental, social, and governance. By offering multi-dimensional indicators, TEJ supports companies in understanding international trends and strengthening sustainability disclosure.

TEJ’s Sustainability Solutions provide one-stop support from information disclosure and risk analysis to decision-making applications, helping companies and financial institutions enhance sustainability resilience and align with international standards.