Table of Contents

Greenwashing refers to companies trying to gain public trust by claiming to have environmental, social, and corporate governance (ESG) contributions or making carbon reduction declarations, but taking little action. To prevent such behavior and to strengthen corporate focus on sustainable ESG disclosure, the International Financial Reporting Standards Foundation (IFRS Foundation) has developed a globally applicable set of sustainability disclosure standards with an accounting foundation—the IFRS Sustainability Disclosure Standards. In this article, we will start by introducing the IFRS Foundation, and then delve into the main content of the IFRS S1 as well as how Taiwan aligns with international sustainability disclosure standards.

IFRS Foundation is a non-profit organization responsible for developing high-quality global accounting standards, known as IFRS Standards. Their mission is to create standards that enhance transparency, accountability, and efficiency for financial markets worldwide. By fostering trust, growth, and long-term financial stability in the global economy, their work brings public interests.

IFRS Foundation oversees two organizations: International Accounting Standards Board (IASB) and International Sustainability Standards Board (ISSB). While IASB is responsible for publishing International Financial Reporting Standards (IFRS), ISSB is in charge of IFRS Sustainability Disclosure Standards (IFRS S1/S2).

IFRS Sustainability Disclosure Standards is based on SASB standards, TCFD framework, and IFRS accounting concept. In current 2 versions, IFRS S1 stipulates where and how to make sustainability-related financial disclosures, while IFRS S2 emphasizes more on climate-related disclosures.

IFRS S1 requires companies to disclose any risk and opportunity that would impact future cash flows (FCF), financing abilities, and capital expenditure (CapEx). Moreover, risks and opportunities that can be reasonably estimated should be categorized as short-term, mid-term, and long-term. In other words, risks and opportunities that can’t be reasonably estimated are not under the regulation of IFRS S1. Similar to “Conceptual Framework for Financial Reporting” under IFRS, IFRS S1 also serves as a basis for all Sustainability Disclosure Standards, meaning that IFRS S2 and other versions that may be released should all abide by IFRS S1.

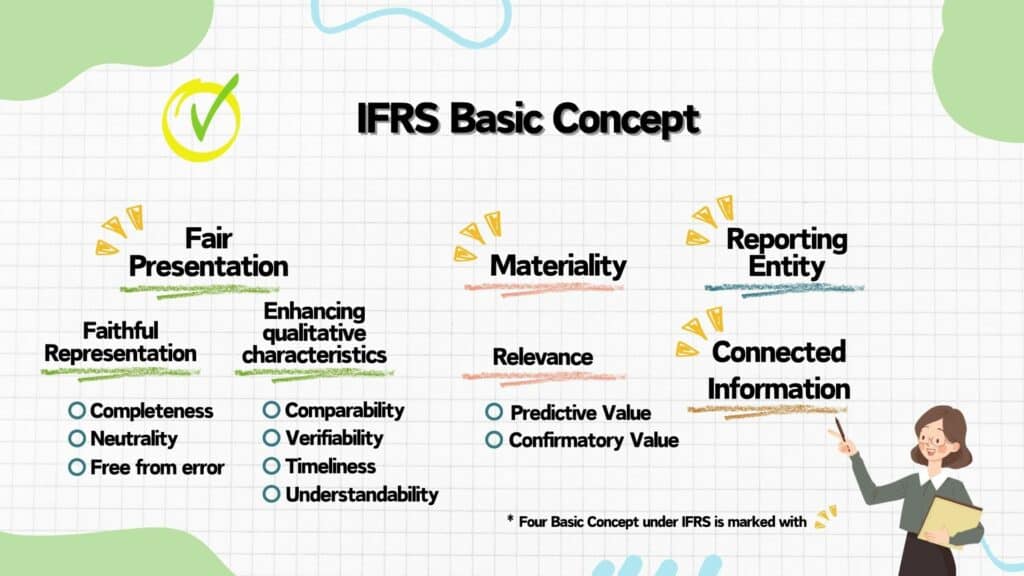

Since sustainability disclosures are still a part of financial reports, IFRS S1 refers to IFRS Conceptual Framework for Financial Reporting and established 4 basic concept:

An entity shall provide a complete, neutral and accurate depiction of all sustainability-related risks and opportunities that could reasonably be expected to affect an entity’s prospects.

An entity shall disclose material information about the sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s prospects.

An entity’s sustainability-related financial disclosures shall be for the same reporting entity as the related financial statements.

An entity shall provide information in a manner that enables users of general purpose financial reports to understand the connections between the items to which the information relates and the connections between disclosures provided by the entity.

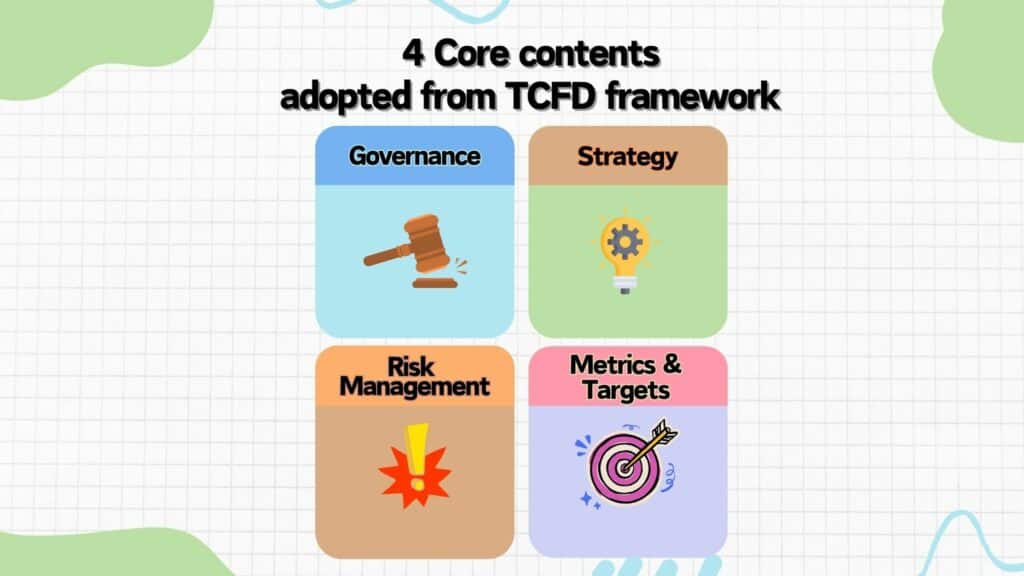

The content of IFRS S1 follows TCFD framework, and requires companies to make disclosures regarding the following four contents.

The governance processes, controls and procedures the entity uses to monitor and manage sustainability-related risks and opportunities

The approach the entity uses to manage sustainability-related risks and opportunities.

The processes the entity uses to identify, assess, prioritize and monitor sustainability-related risks and opportunities.

The entity’s performance in relation to sustainability-related risks and opportunities, including progress towards any targets the entity has set or is required to meet by law or regulation.

Aside from the four core contents, IFRS S1 also has the following five general requirements.

In addition to IFRS S1, an entity shall refer to and consider the applicability of the disclosure topics in the SASB Standards.

An entity is required to provide disclosures required by IFRS Sustainability Disclosure Standards as part of its general purpose financial reports.

An entity shall report its sustainability-related financial disclosures at the same time and cover the same reporting period as the related financial statements.

Unless another IFRS Sustainability Disclosure Standard permits, an entity shall disclose comparative information in respect of the preceding period for all amounts disclosed in the reporting period.

An entity whose sustainability-related financial disclosures comply with all the requirements of IFRS Sustainability Disclosure Standards shall make an explicit and unreserved statement of compliance.

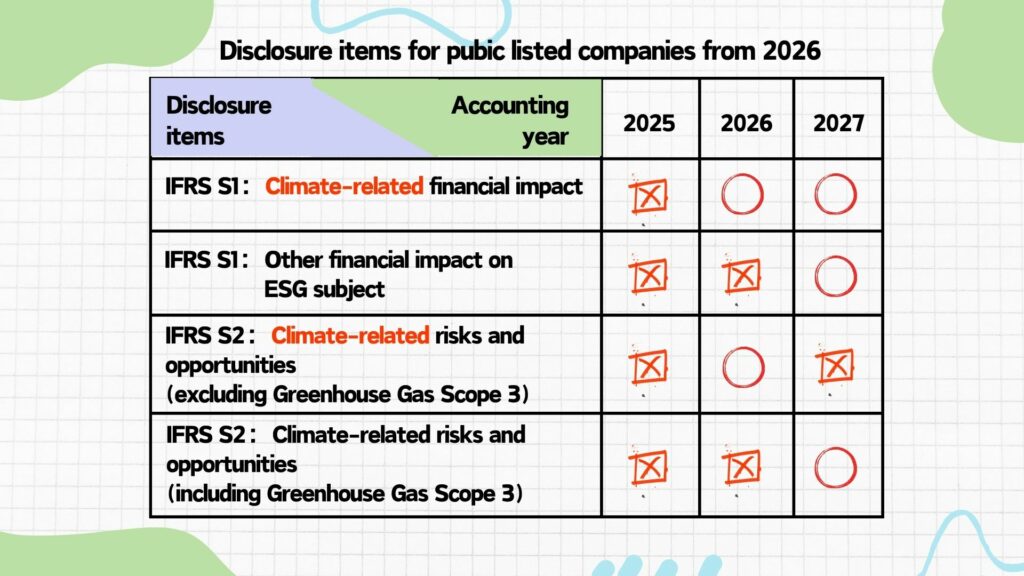

After the emergence of IFRS S1 and S2, in order to gear to international standards, under “Taiwan’s Roadmap to Align with IFRS Sustainability Disclosure Standards”, Financial Supervisory Commision (FSC) began to require listed companies and OTC companies to follow IFRS to disclose sustainability-related information.

“Taiwan’s Roadmap to Align with IFRS Sustainability Disclosure Standards” was released in 2023. Starting from 2026, companies will start to apply IFRS S1 and S2 standards through direct adoption, and will be divided into three stages based on their capital amount. Here are a few characteristic of “Taiwan’s Roadmap to Align with IFRS Sustainability Disclosure Standards”:

Since annual reports in Taiwan are divided into financial reports and shareholders’ meeting annual reports, FSC requires companies to add a dedicated chapter for sustainability information in shareholders’ meeting annual reports, while financial reports only need to abide by IFRS.

Sustainability-related disclosures should be released in annual reports simultaneously with financial reports, and cover the same reporting period.

To provide enterprises with sufficient preparation time, FSC will allow exemptions of specific items in the sustainability standards:

For disclosure items involving great quantification difficulties, qualitative information may be disclosed based on the company’s current technology, resources, and capabilities.

Take Taiwan Cement Corporation (1101.TW) as an example. It is a public listed company with a capitalization of NTD 77.5 billion. Therefore, Taiwan Cement should apply IFRS S1 starting from 2026, meaning that they are required to make sustainability-related disclosures in 2026 annual report on March 15, 2027.

To ensure every country reaches a consensus in sustainability-related disclosures, enabling stakeholders to understand the opportunities and risks companies face in future sustainable development, ISSB introduced the first two bulletins, IFRS S1 and IFRS S2, in June 2023.

Thanks to the effort IFRS S1 and S2 put into making sustainability-related information quantitative, stakeholders can clearly see a company’s contributions to environmental, social, and governance (ESG) aspects,which greatly helps curb the practice of “Greenwashing”.