Since 2020, Taiwan’s passive component industry has faced challenges due to intensified competition between the US and China, the impact of the COVID-19 pandemic, and the Russo-Ukrainian war. However, despite these difficulties, both YAGEO (2327.TW) and Walsin Technology (2492.TW) have strategically leveraged different types of mergers and acquisitions to enhance their products, technologies, markets, and customer base. As a result, their revenues and scale have continued to grow. Additionally, with the rise of applications like electric vehicles, 5G/6G internet, and AI-driven products, Taiwanese manufacturers are seizing opportunities across various domains.

Table of Contents

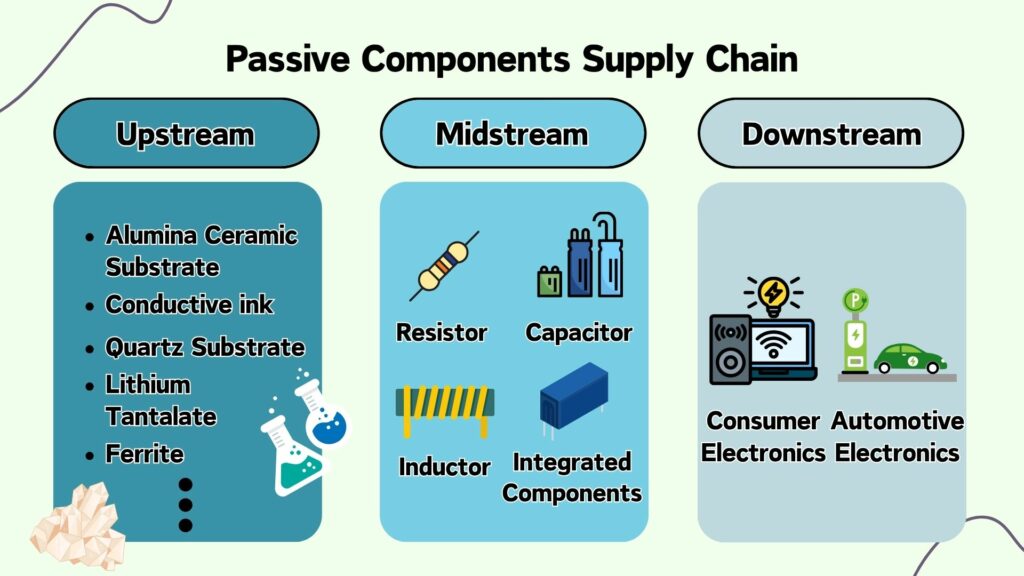

According to the Taiwan Stock Exchange’s Industry Value Chain Information Platform, upstream raw material suppliers for passive components provide materials for resistors, capacitors, inductors, as well as materials for filters and oscillators. The midstream manufacturers perform assembly and production, resulting in the production of RLC components and integrated devices. For instance,

Active components have the ability to operate independently, while on the other hand, passive components play the role of protecting active components.

| Active Components | Passive Components | |

| Functions | Operates actively and independently | Protects Active Components passively |

| Products | Transistors, memories, diodes, etc. | RLC components and integrated components |

Click in to read about “Passive Componenets Industry’s Recovery in 2023”

YAGEO Group, with subsidiaries including YAGEO, Jamicon, CHILISIN, and Global Testing, often utilizes its great advantage in free cash to acquire peers in the industry. YAGEO acquired Xianghua Electronic in 2017, Mag Layers, ZEITEC, Pulse Electronic, Bothhand Enterprise, MAGIC technology in 2018, TONG HSING, KEMET, SOWIN, Kingpak in 2019, and Chinsan in 2020. With the great synergy brought through acquisition, YAGEO Group reached a total of NTD 270 billion in enterprise value by the end of 2020.

YAGEO focused on horizontal integration (peer companies), enhancing capacity and lowering cost to maintain competitiveness in the passive component industry, meanwhile with the hope of achieving economies of scale. Although most companies get delisted after acquisition, some group members aren’t 100% YAGEO group’s subsidiary, including YAGEO (2327.TW), Jamicon (2375.TW), TONG HSING (6271.TW) and Global Testing (AYN.SI).

Since 2017, due to virtual currency trend, a nationwide internet mining movement has emerged, leading to a rapid increase in demand for related terminal equipment and accessories. Against this backdrop, Yageo Group entered a period of rapid acquisitions. Most companies being acquired ceased public issuance and became part of Yageo Group, resulting in annual growth in production capacity. In terms of production quantity, YAGEO, Jamicon, CHILISIN, and TONG SHING each experienced increases ranging from 25% to 35% in the year of acquisition, demonstrating the positive impact of the acquired entities on overall production line of the group. For the parent company, YAGEO, the acquisition of these companies expanded the production capacity of its product lines, achieving economies of scale.

| Company Name | Productivity of YAGEO group’s subsidiaries | ||||||

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

| YAGEO | 1,257,546 | 1,390,101 | 1,838,253 | 1,927,734 | 2,093,767 | 2,224,648 | 2,250,052 |

| Jamicon | 2,305 | 3,103 | 2,732 | 1,946 | 1,896 | 2,125 | 1,397 |

| TONG SHING | 5,327 | 7,074 | 6,470 | 6,572 | 6,214 | 7,770 | 5,893 |

| CHILISIN | 420,086 | 372,345 | 554,533 | 246,246 | 359,741 | Got 100% acquired by YAGEO in 2021 | |

| Total | 1,685,264 | 1,772,623 | 2,401,988 | 2,182,498 | 2,461,618 | 2,234,543 | 2,257,342 |

| YoY | – | 5.18% | 35.50% | -9.14% | 12.79% | -9.22% | 1.02% |

YAGEO Group not only focuses on horizontal integration but also emphasizes expanding its market presence and venturing into new product areas. In August 2021, Yageo and Foxconn’s subsidiary jointly established a semiconductor company called “XSemi Corporation,” with Yageo holding the majority ownership. Furthermore, in June 2022, XSemi invested NT$3.1 billion in Advanced Power Electronics Corp. (APE), enabling YAGEO to enter the active component market for MOSFET (Metal-Oxide-Semiconductor Field-Effect Transistor) products. This move enables YAGEO to compete with industry peers such as VISHAY and ROHM in the MOSFET segment.

Furthermore, TAGEO closed the acquisition of the high-end thermal sensor division with Heraeus in April 2023, and the acquisition of high-end industrial sensor division with Schneider Elec. in November 2023. These acquisitions demonstrate YAGEO’s ambition to expand its production capacity beyond industry consolidation and to venture into industrial component product lines and patent layouts. By acquiring European brand companies, YAGEO aims to distribute its production capacity worldwide, mitigating operational risks arising from geopolitical factors.

Aside from expanding new business, YAGEO also focuses on internal integration. Through public offerings and the acquisition of significant investments, the company aims to reconfigure production capacity and product lines, with the goal of achieving economies of scale and improving overall financial performance.

| Announcement Date | 2021/05/05 | 2021/06/30 | 2022/05/20 |

| Acquirer | YAGEO | YAGEO | XSEMI |

| Target | XSEMI | CHILISIN | Advance Power |

| Business | Power MOSFETs | Inductor, Resistor, Coil, and Iron (Powder) Core | MOSFET, IGBT, and Power Management IC solutions |

| Means of Transaction | Joint Venture — Cash | Share Transfer | Cash |

| Joint Venture with Foxconn | 1 share of CHILISIN for 0.2002 share of YAGEO | NTD 82.48 per share | |

| Result | Established on August 5th 2021, with YAGEO obtaining 55% of share. | Transfer completed in January 5th 2022, with YAGEO acquiring 100% of CHILISIN | Cash capital increase base date is May 31st 2023 , acquiring 30.08% of share |

| Transfer Consideration | NTD 0.165 billion | NTD 0.478 billion | NTD 2.89 billion |

| Announcement Date | 2022/10/11 | 2022/10/27 | 2023/12/11 |

| Acquirer | YAGEO | YAGEO | KEMET |

| Target | Heraeus Nexensos GmbH | Schneider Electric Telemecanique Sensors | Nantong Haimei Electronics Electrolytic Capacitor |

| Business | Platinum Temperature Sensors | Energy Management and Industrial Automation Components | MOSFET、IGBT, and Power Management IC solutions |

| Means of Transaction | Cash | Cash | Cash |

| € 79 million | € 686 million | USD 11 million | |

| Result | Acquisition date set on April 1st 2023 | Complete in November 1st 2023 | Haven’t complete |

| Transfer Consideration | NTD 2.67 billion | NTD 21.4 billion | NTD 0.35 billion |

Similar to YAGEO group, PSA group (Passive System Alliance) has also acquired lots of subsidiaries, including Walshin Tech. (2492.TW), Prosperity Dielectrics (6173.TWO), Hannstar Board (5469.TW), Global Brands Manufacture (6191.TW), and Walton Advanced Engineering (8110.TW). Unlike Yageo Group, which typically acquires full ownership, PSA Group usually acquires partial stakes in these companies. While they replace the existing management team, the original shareholders continue to participate in company operations. This approach allows for shared success and the exploration of more collaboration opportunities and profits. Between 2017 and 2020, the PSA Group acquired several companies, including ELNA Printed Circuits, INPAQ Technology (6284.TW), Career Tech. (6153.TW), SILITECH (3311.TW), Soshin Electric, and so on, reaching NT$501 billion in enterprise value by the end of 2020.

Unlike YAGEO, which primarily focuses on horizontal mergers to acquire industry capacity and technology, PSA group emphasizes vertical integration. For instance, in 2005, Walsin Tech. strategically allied with Prosperity Dielectrics, a producer of passive component materials. Walsin Tech. aims to vertically integrate passive components and printed circuit boards, providing comprehensive solutions and establishing the foundation for integrated electronic materials services. The table below illustrates the diversity and end-to-end coverage of their products, from upstream raw materials to midstream manufacturing of active and passive components within PSA Group’s supply chain.

| Product | Amount | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Chip Resistor | Million Pieces | 320,986 | 398,723 | 544,409 | 638,912 | 601,824 | 652,370 | 707,566 |

| RF components | Million Pieces | 1,290 | 1,290 | 1,800 | 1,800 | 2,760 | 5,250 | 5,783 |

| Dielectric ceramic powder | Thousand Kilogram | 2,984 | 3,744 | 4,554 | 4,554 | 4,554 | 4,862 | 4,862 |

| Capacitor | Million Pieces | 309,096 | 363,304 | 459,282 | 544,782 | 564,413 | 642,521 | 654,656 |

| Protective Components | Million Pieces | 0 | 0 | 0 | 0 | 11,100 | 20,000 | 20,000 |

| Others | Million Pieces | 677 | 875 | 988 | 813 | 572 | 401 | 653 |

| Total (Without Powder)* | 632,049 | 764,192 | 1,006,478 | 1,186,306 | 1,180,668 | 1,320,542 | 1,388,658 | |

| YoY | – | 20.91% | 31.70% | 17.87% | -0.48% | 11.85% | 5.16% | |

| Capital Expenditure (billion) | 1.39 | 2.07 | 6.10 | 8.27 | 5.61 | 1.02 | 4.72 | |

| Product | Productivity of Hannstar Board and its subsidiaries | |||||||

| Amount | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

| EMS | Million Pieces | 217 | 236 | 211 | 331 | 152 | 157 | 146 |

| YoY | – | 8.49% | -10.41% | 56.42% | -54.08% | 3.29% | -7.00% | |

| PCB | Thousand Square Feet | 108,600 | 111,600 | 123,055 | 126,139 | 122,284 | 124,079 | 122,263 |

| YoY | – | 2.76% | 10.26% | 2.51% | -3.06% | 1.47% | -1.46% | |

| Company Name | Productivity of PSA’s Subsidiaries | ||||||

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

| Walton Advanced Engineering | 2,870 | 3,030 | 3,070 | 3,150 | 2,800 | 6,970 | 6,970 |

| PSAITC | 30 | 27 | 29 | 26 | 20 | 26 | 31 |

| Career Tech. | ✯ | 1,157 | 1,498 | 1,129 | 1,291 | ||

| SILITECH | ✯ | 158 | 174 | 188 | |||

| JOYIN | ✯ | 1,500 | 1,500 | ||||

| Total | 2,900 | 3,057 | 3,099 | 4,333 | 4,476 | 9,799 | 9,980 |

| YoY | – | 5.41% | 1.37% | 39.82% | 3.30% | 118.92% | 1.85% |

Compared to YAGEO group’s aggressive acquisition strategy, PSA group tends to stabilize its position in the domestic market before expanding internationally. Their strategy focuses on gradual acquisitions to achieve alliance synergies. For instance, in April 2021, INPAQ became the biggest shareholder of Joyin, which manufactures passive protective components, such as NTCs (Negative Power Thermistor) and VDRs (Voltage Dependent Resistor).

In addition to external acquisitions, PSA group has been implementing internal optimizations in recent years. Apart from job rotations, the primary goal is vertical integration of resources within the group. Initially, in early 2021, Prosperity Dielectrics sold its specialized inductor production facility in Hunan to a subsidiary of INPAQ, changing focus to core products such as capacitors, resistors, and ceramic powders. INPAQ, with its resistor and inductor production capabilities, can further integrate resources and control raw material prices to achieve overall group synergy.

| Announcement Date | 2021/01/27 | 2021/04/28 | 2022/01/13 |

| Acquirer | INPAQ | INPAQ | Walsin Tech. |

| Target | Prosperity Dielectrics — Hunan Specialized Inductor Production Plant | JOYIN | Matsuo Electric |

| Business | Manufacturing and selling magnetic components | NTCs (Negative Power Thermistor) and VDRs (Voltage Dependent Resistor) | Tantalum Capacitors, Film Capacitors, and Circuit Protection Devices |

| Means of Transaction | Cash | Cash | Cash |

| CNY 95 million for 100% of shares | NTD 276 million, for 22.84% of shares | JPY 783 per share for 638000 of shares, accounting for 19.89% of company shares | |

| Result | Transaction date on April 30th 2021 | Take into account on April 28th 2021 through Equity Method — Investment in associate | Take into account on January 13th 2022 through Equity Method — Investment in associate |

| Transfer Consideration | NTD 410 million | NTD 276 million | NTD 137 million |

| Announcement Date | 2022/06/17 | 2022/06/17 | 2023/03/15 |

| Acquirer | Prosperity Dielectrics & Walsin Tech. | INPAQ | TAI-TECH |

| Target | JOYIN | ELECERAM TECH. | APAQ Tech. |

| Business | NTCs (Negative Power Thermistor) and VDRs (Voltage Dependent Resistor) | Piezoelectric Transformers, Piezoelectric Actuators, Ultrasonic Oscillators | Wound Solid-State Capacitors and Surface Mount Solid-State Capacitors |

| Means of Transaction | Cash | Cash | Selling shares |

| Prosperity Dielectrics & Walsin Tech. together obtained 30.4% of shares, paying NTD 317 million and NTD 55 million respectively. | NTD 210 million for 72.9% of shares | Sold 17.607 million of shares for NTD 102 million | |

| Result | Take into account in July 2022 through Equity Method — Investment in associate | Completed in July 1st 2022 | Sold all of its share to TAI-TECH |

| Transfer Consideration | NTD 372 million | NTD 210 million | NTD 102 million |

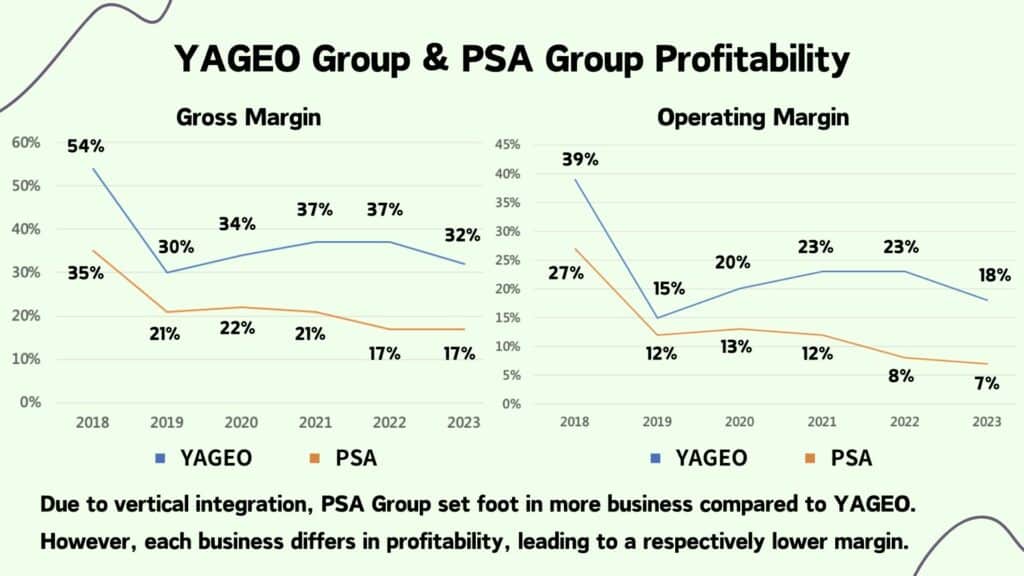

Due to different acquisition integration styles, the two major groups have varying revenue performance in response to market events. YAGEO group relies on horizontal integration, expanding its passive component offerings to maximize the benefits of production and sales across various types of passive components. As a result, YAGEO group outperformed PSA group in 2018 and 2021. However, because of the concentration of risk in the same industry, YAGEO experienced larger declines during passive component downturns, such as in 2019 and 2023. Nevertheless, as YAGEO gradually diversified into active components, the revenue volatility in 2023 improved slightly compared to 2019.

On the contrary, PSA group has a vertical supply chain layout and diversifies across multiple industries. While its revenue can keep pace with YAGEO group, the profit margins and operating margins in each industry vary. As a result, PSA’s profit margins and operating margins are lower than those of YAGEO. Additionally, during favorable market conditions for passive components, PSA’s profitability may be diluted due to diversification. Furthermore, PSA is also affected by underperforming subsidiaries within the group, leading to lower profits compared to YAGEO. However, PSA mitigates risk by spreading across different industries, resulting in more stable revenue, gross margins, and operating margins even when the passive component market faces challenges.

YAGEO Group and PSA group currently hold the top two positions among domestic passive component manufacturers in Taiwan. Between 2017 and 2023, these two groups engaged in a total of 16 acquisitions and 7 strategic alliances. However, their approaches to integration differ significantly, resulting in distinct positioning.

TEJ datasets specifically provides the information required for basic analysis of the securities financial market, quickly solve your data needs, and efficiently help your decision-making.

Check what TEJ dataset provide!