Table of Contents

In today’s stock market, investors face the challenge of choosing from many stocks, with many hoping to find undervalued stocks with solid fundamentals. However, market volatility and information asymmetry often make this goal difficult to achieve. In this context, the Piotroski F-score, also known as the Piotroski score or F-score, has become an important tool for investors.

Conceived by the esteemed former University of Chicago professor Joseph Piotroski, the F-score strategy is a comprehensive evaluation of nine financial report conditions. This strategy serves as a reliable guide for investors, providing a holistic view of a company’s financial health. It encompasses aspects of profitability, safety, and growth, offering a multidimensional analytical framework that enables investors to assess a company’s potential value more comprehensively. To delve into the performance of the F-score in the Taiwan stock market, this article construct the F-score strategy, thereby equipping investors with a deeper understanding of the investment benefits that the F-score can potentially unlock.

According to the paper by Professor Joseph Piotroski, to identify undervalued stocks with relatively stable profitability, safety, and growth, the F-score strategy is constructed through the following two steps to generate trading signals:

The 9 fundamental criteria of the F-score strategy are as follows:

Next, let’s generate the trading signals required for the F-score strategy.

First, we obtain undervalued stocks through the following two steps:

With the backtest period set from May 6, 2019, to December 31, 2023, we then import the price and volume data of the above 340 undervalued stocks and the TAIEX-Total Return Index (IR0001) as the performance benchmark.

To calculate the financial criteria needed for the F-score, we use TEJ Quantitative Investment Database to fetch the following 9 financial data points:

Obtain All-encompassing Quantitative Data Above Through TEJ!

The CustomDataset class can import content from a database into Pipeline, facilitating subsequent backtesting. In this example, we use it to import the financial data we get from TEJ Quantitative Investment Database to calculate the F-score into Pipeline. Besides, before calculating the F-score, we use the CustomFactor function to define the following two factors:

The Pipeline() function provides users with the ability to quickly process quantitative indicators and price-volume data of multiple stocks. In this case, we use it to handle:

Utilize TEJ’s simplified version of the Zipline backtesting engine, TargetPercentPipeAlgo, which allows all backtesting parameters to be set in a single line, requiring only the strategy pipeline input for execution.

Parameters adjusted for this strategy:

VolumeShareSlippage.Custom_TW_Commission.

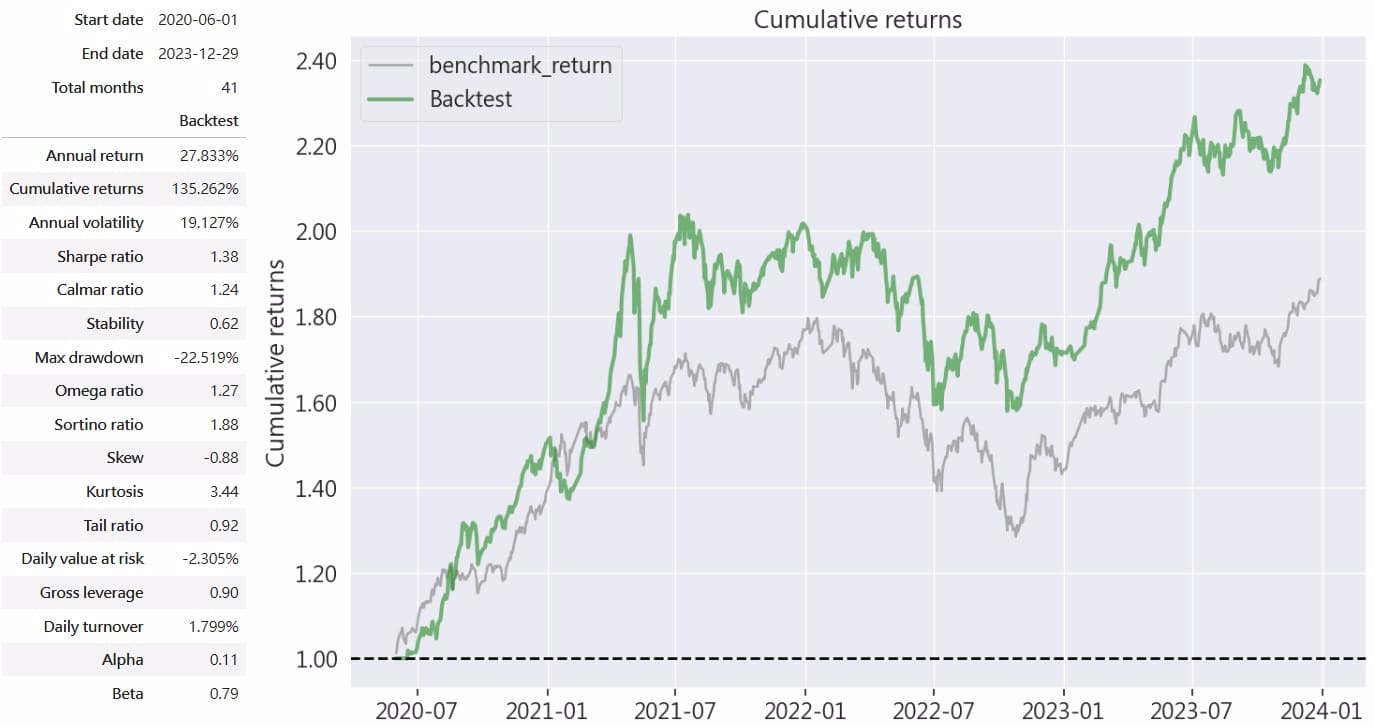

Based on the table above, the F-score strategy outperformed the market. It achieved an annualized return of 27.83%, with an annualized volatility of approximately 19.1%. Furthermore, the Sharpe ratio stands at 1.38, and the alpha value is 0.11, indicating that the F-score strategy generates respectable excess returns for investors under relatively controlled risk. Examining the beta value of 0.79, it suggests that the performance of the F-score strategy is moderately correlated with the market trend, indicating that the 9 stock selection criteria of the F-score strategy indeed help mitigate some systematic risks for investors. In the performance comparison chart, it can be observed that the F-score strategy experienced a smaller decline compared to the market in 2022, and after recovering from the bear market, it outperformed the market, underscoring the strategy’s strong profitability.

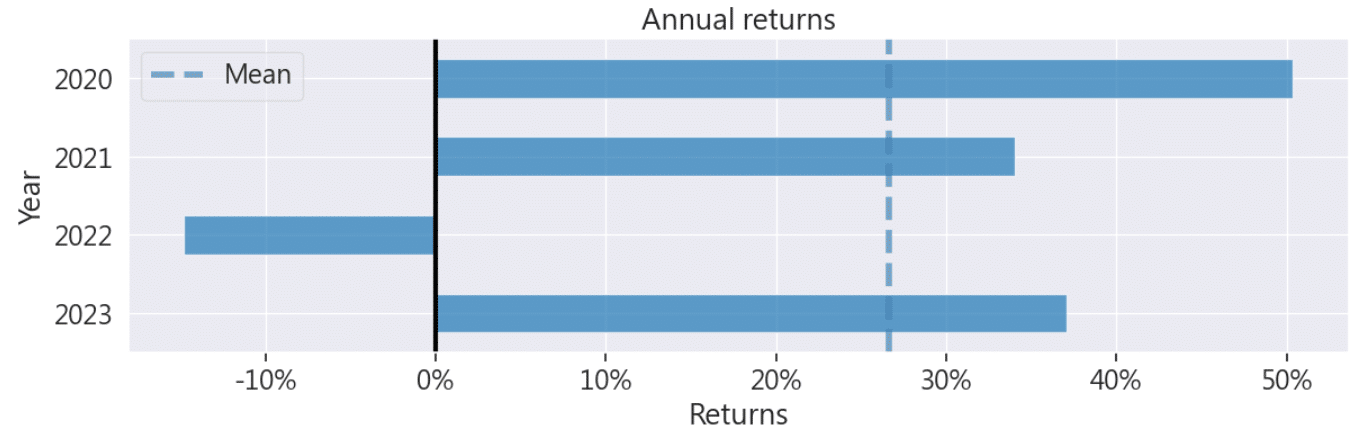

In the annual returns chart, aside from a significant downturn in 2022, the strategy achieved annualized returns exceeding 30% in the other three years.

Furthermore, from the long/short position exposure chart, we can see that setting the maximum leverage to 90% in TargetPercentPipeAlgo keeps the exposure stable around 0.9. This ensures that the F-score strategy retains some flexibility and is less affected by large fluctuations.

This strategy takes Joseph Piotroski’s ( 2002 ) paper as its foundation, aiming to explore whether the F-score strategy can provide stable profits for investors in the Taiwan stock market. In constructing the strategy, we identify undervalued stocks using the book-to-market ratio and calculate the F-score and generate trading signals. Finally, we apply the simplified backtesting engine, TargetPercentPipeAlgo, to conduct strategy backtesting.

The quarterly rebalancing feature of the F-score strategy allows investors to promptly update their portfolios after each quarter’s new financial data release. Performance analysis using Pyfolio further confirms the F-score strategy’s superior profitability compared to the broader market. This demonstrates that even after over 20 years since its introduction, the strategy retains robust capabilities in evaluating company profitability, safety, and growth potential. Moreover, it shows applicability within the context of the Taiwan stock market.

Please note that the strategy and target discussed in this article are for reference only and do not constitute any recommendation for specific commodities or investments. In the future, we will also introduce using the TEJ database to construct various indicators and backtest their performance. Therefore, we welcome readers interested in various trading strategies to consider purchasing relevant solutions from Quantitative Finance Solution. With our high-quality databases, you can construct a trading strategy that suits your needs.

“Taiwan stock market data, TEJ collect it all.”

The characteristics of the Taiwan stock market differ from those of other European and American markets. Especially in the first quarter of 2024, with the Taiwan Stock Exchange reaching a new high of 20,000 points due to the rise in TSMC’s stock price, global institutional investors are paying more attention to the performance of the Taiwan stock market.

Taiwan Economical Journal (TEJ), a financial database established in Taiwan for over 30 years, serves local financial institutions and academic institutions, and has long-term cooperation with internationally renowned data providers, providing high-quality financial data for five financial markets in Asia.

With TEJ’s assistance, you can access relevant information about major stock markets in Asia, such as securities market, financials data, enterprise operations, board of directors, sustainability data, etc., providing investors with timely and high-quality content. Additionally, TEJ offers advisory services to help solve problems in theoretical practice and financial management!