Table of Contents

Quantitative Investing requires historical data to perform backtesting, examining the feasibility of our investing strategy. Therefore, it is pivotal to ensure that the data used for analyzing always aligns with the information the investors have when making their decisions. For instance, in order to pursue correctness, accounting databases update new numbers when financial restatements occur. However, using the data after financial restatement for backtesting will prevent investors from accurately reconstructing the actual market conditions at that time, and will lead to information bias, reducing the credibility of the backtesting result.

Due to the fact that the misuse of financial restatement data often causes backtesting errors, this article aims to discuss the difference of backtesting results before and after financial restatements through the portfolio performance of factor investing.

A financial restatement is the alteration of released financial reports. Reasons for financial restatements include the adjustment of accounts in accounting, the amendment to IFRS, and the requirement from supervisory agencies. Normally, a company is asked to restate financial reports when the following occurs,

If investors mistakenly use updated financial information for analysis, it can lead to bias in backtested returns. In simple terms, if there is little difference between financial statements before and after restatement, the effect on investment risk due to misinterpretation is low. Conversely, if there is significant disparity between pre- and post-financial restatement, the investment risk arising from misinterpretation becomes substantial. Therefore, when conducting backtesting analysis, having data that accurately reflects the historical context is crucial for precise and effective return calculations.

TEJ Quantitative Database, based on the “Point in time” concept, helps recover information at the exact spot the event occurred, avoiding survivorship bias and look-ahead bias. The following examination is conducted with TEJ Quantitative Database’s pre-financial restatement Point in time data (PIT) and post-financial restatement data (TEJ IFRS Finance).

After referring to relevant researches, the following representative factors are chosen for constructing our portfolio,

For simplicity, in the following section, PITW (PIT wins) is used to describe the situation where the return calculated using PIT data is higher than that of using TEJ IFRS Finance.

Find the Solutions to all Your Financial Difficulties!

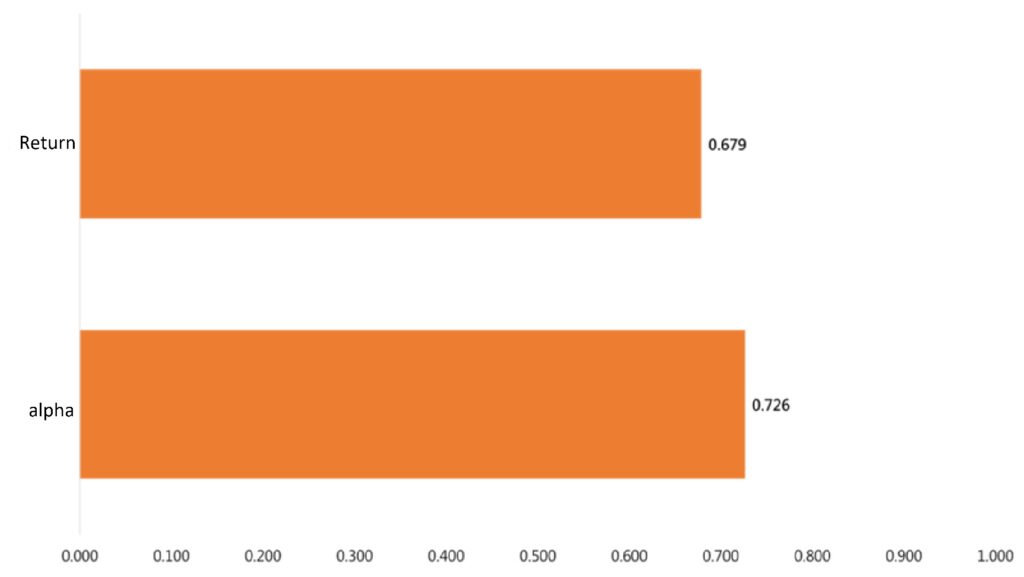

In order to examine whether or not using PIT data results in higher return, backtesting is conducted on all the factors, and the results are divided into ten groups based on their performances — the first group collects the top 10% portfolio with the highest return. Given that investors tend to invest in targets with better performances, the following test result only takes the first group into consideration.

Based on Graph 1, when comparing the first group’s return, PITW has a probability of almost 68%; when comparing the first group’s alpha (Excess Return), PITW has a probability of over 70%. This indicates that for companies with top 10% performance, applying “PIT data” instead of ”IFRS Finance data” results in a significantly higher return.

Factor

In previous strategies, PITW occurs with a probability of roughly 70%. This can be credited to three characteristics — Low Volatility, Low Speculation, and Low Downside Risk. Hence, if managers wish to manipulate financial statements, they tend to disguise themselves as a company with low volatility, low downside risk, and high quality. Moreover, the phenomenon also matches our hypothesis — Market sees companies with greater value when using PIT data. Despite this phenomenon going against the core value of any firm, it allows a firm to achieve better performance in the short run.

Holding Period

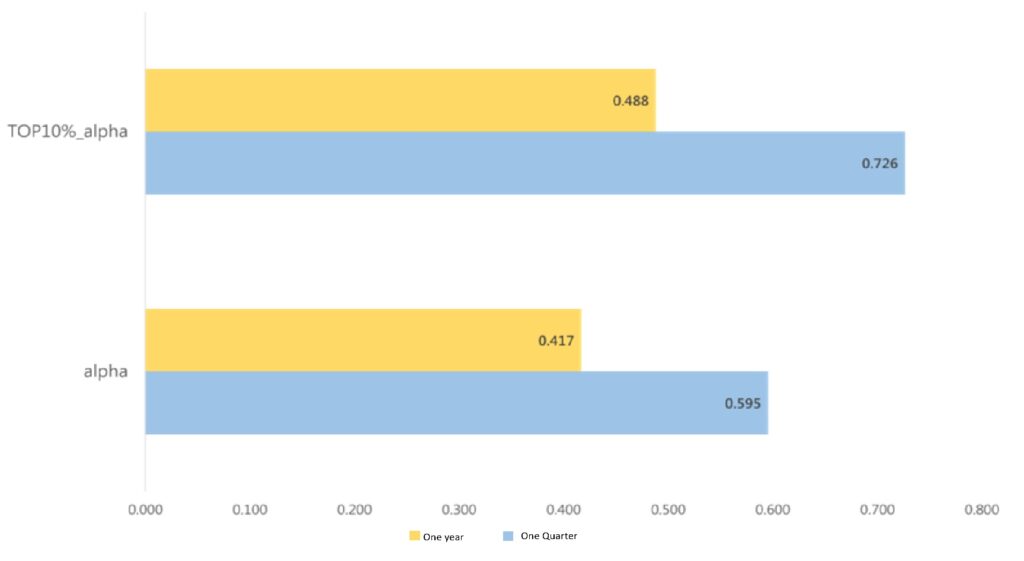

As time goes by, the correct information will gradually be disclosed. Therefore, the test extends the original holding period, three months (One Quarter), to a year.

According to Graph 2, PITW in alpha declines from 59.5% to 41.7% once the holding period is extended. Furthermore, if only the first group is considered, PITW in alpha drops significantly from 72.6% to 48.8%. The result suggests that with the disclosure of correct information, overvaluation gradually recovers. Hence, once the holding period is extended to a year, the return calculated using IFRS Finance exceeds the return using PIT.

In addition, even if only targets with low volatility, low speculation, and low downside risk are considered, after extending the holding period to a year, almost every factor’s PITW fell below 70%. As a result, regardless of volatility and risk, excessive return based on PIT disappears as time passes.

For investors, the adoption of data after financial restatement leads to errors in estimating returns. This is mainly because recognition errors often cause overpricing in the market. Consequently, once the error is disclosed, correction on the stock price is inevitable.

Through results from factor investing, PIT data outperforms as long as the holding period is within three months, but its performance declines as the holding period increases. Hence, for investors, it is always important to choose “available and accurate” historical data when performing backtesting, since the disclosure time of financial data can lead to substantial errors in calculating returns.

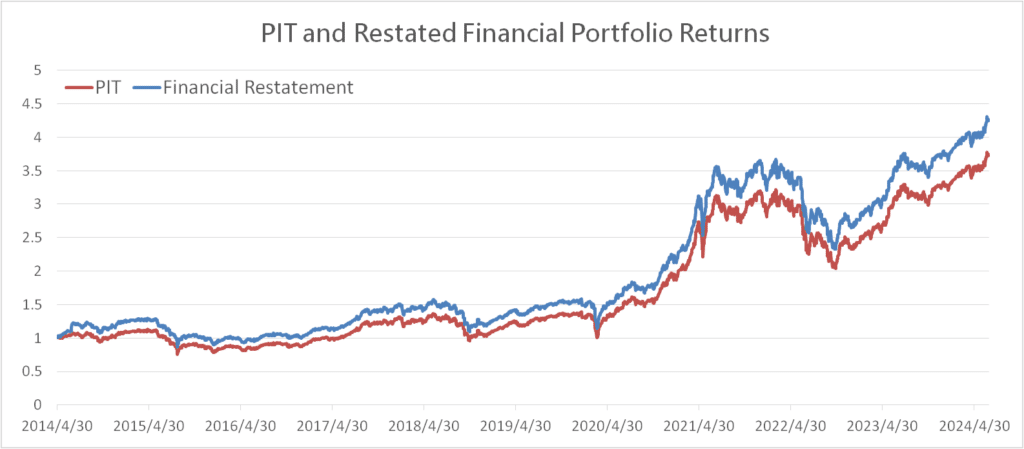

Finally, we further conducted a backtest comparing financial statements before and after restatement over the past 10 years. Using the top 150 companies by market capitalization in Taiwan as a sample, we selected the top 20% of stocks based on net profit margin growth rate as the stock-picking criteria. We established two portfolios: one using PIT (Point-In-Time) financial data and the other using non-PIT (restated financials covering historical data).

The results showed that the portfolio using restated historical data appeared to perform better due to the use of future data, leading to a look-ahead bias. This causes the backtest results to inaccurately reflect the actual market conditions. Therefore, restated data is typically used to overwrite historical data. If an unorganized, uncleaned database is used, it will lead to inaccurate backtest results.

In TEJ Quantitative Finance Solutions, the concept of Point in time is not limited to financial databases. Information regarding ex-dividend, dividend revision, and alteration of share capital also possess PIT characteristics. Apply PIT data for backtesting, investors can effectively conduct quantitative analysis and find out the best investing strategy!