Table of Contents

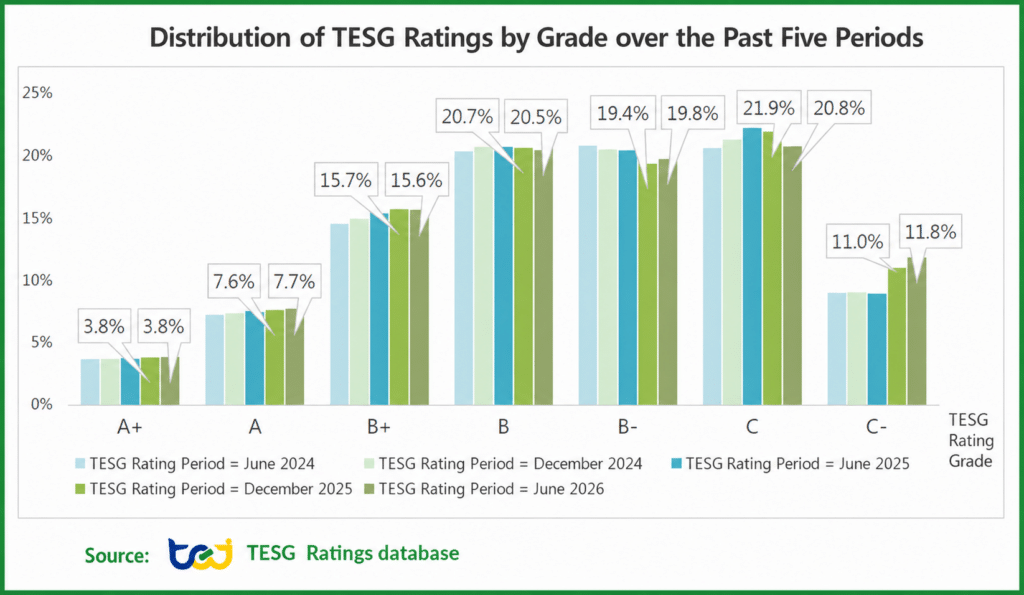

Taiwan Economic Journal (TEJ) released the latest TESG Ratings results on May 4, 2026. This round of TESG ratings covers a total of 2,559 companies, with 41 newly added samples. Looking at the rating structure over the past five periods, the proportion of leading companies, rated A+ and A, has shown a steady and modest upward trend. Meanwhile, the share of companies rated C- has also increased over the past two periods, rising from 8.9% in the first half of 2025 to 11% in the second half of 2025, and further to 11.8% in the first half of 2026, as shown in Figure 1.

TEJ’s ESG Sustainability Consulting Services team explains that the TESG ratings distribution is constructed based on a percentile-based classification mechanism, resulting in an overall normal distribution concentrated in the middle tiers. Therefore, changes in the proportion of each rating category mainly reflect shifts in companies’ relative rankings rather than absolute changes in sustainability performance. To gain a more comprehensive understanding of ESG development trends, it is recommended to analyze TESG score changes together with upgrade and downgrade patterns, thereby improving the accuracy and insightfulness of interpretation.

Figure 1. Distribution of TESG Ratings by Grade over the Past Five Periods

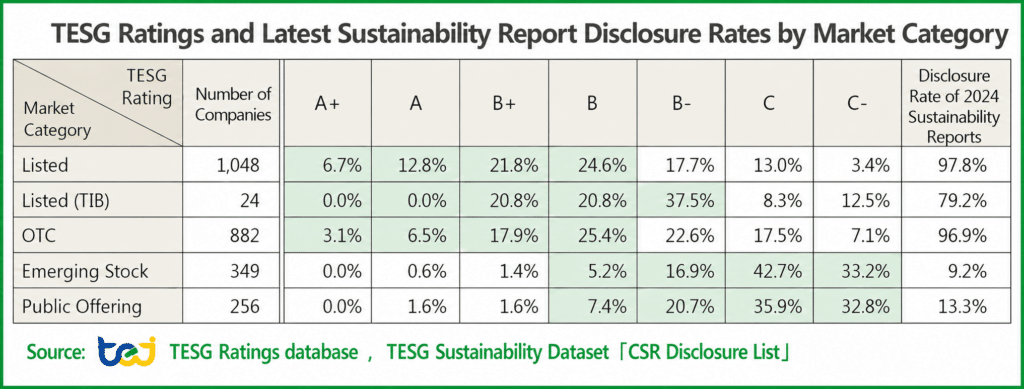

By market category, TESG rating distribution shows clear differences from 2024 sustainability report disclosure rates. Listed and OTC companies generally performed better, with a higher share of leading ratings (A+ and A) and most companies concentrated in the B+ to B range, indicating relatively mature sustainability management. Their disclosure rates reached 97.8% and 96.9%, reflecting high information transparency.

In contrast,Taiwan Innovation Board companies were mostly concentrated in the average rating range (B+, B, and B-), with no companies rated A or above this period. Although their disclosure rate reached 79.2%, they still require a stronger disclosure foundation. Emerging and public companies had a higher share of lagging ratings (C and C-), with disclosure rates of only 9.2% and 13.3%, showing more room for improvement.

Driven by the Regulations Governing the Preparation and Filing of Sustainability Reports, listed and OTC companies are now required to fully disclose 2024 sustainability reports, significantly improving overall disclosure rates. By comparison, Emerging and public companies are not yet fully covered by mandatory disclosure, resulting in lower disclosure rates and more companies falling into lower TESG rating groups.

Table 1. TESG Ratings and Latest Sustainability Report Disclosure Rates by Market Category

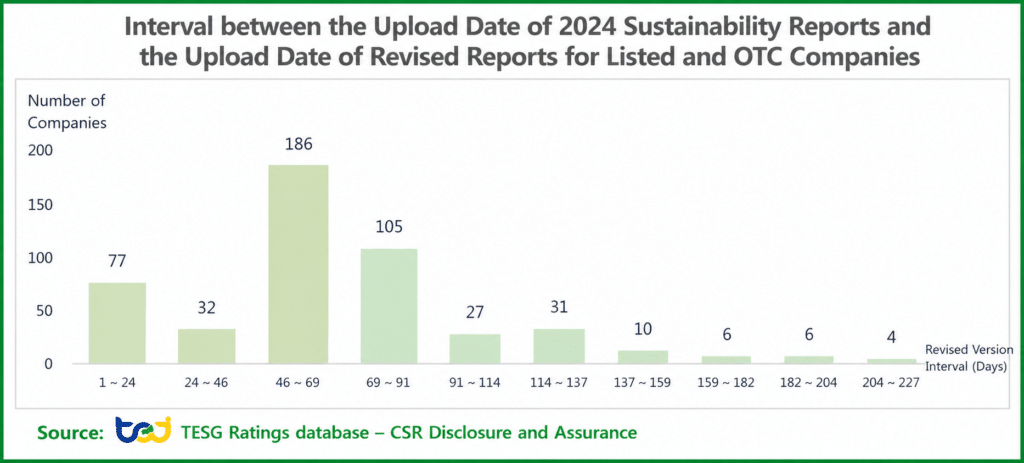

According to TEJ TESG Sustainability Dataset statistics, as of April 2026, a total of 1,997 listed OTC,Emering, and public companies had disclosed their 2024 sustainability reports, including 1,903 listed and OTC companies. Most companies completed their initial filings before the statutory deadline of August 31, while only 7 companies filed after the deadline.

However, even after the initial disclosure, some companies continued to revise, supplement, or update their reports. Among the 484 companies that revised their reports, the largest group completed revisions within 46 to 69 days after the initial filing, totaling 186 companies. This indicates that most revised versions were completed within one to two months after the first disclosure. Another 105 companies revised their reports within 69 to 91 days, while 77 companies completed revisions within 1 to 24 days. Cases with revision intervals exceeding 159 days were relatively rare.

Overall, although most companies completed sustainability information disclosure within the statutory deadline, follow-up revisions show that sustainability reports are not one-time static documents, but dynamic information sources that may continue to be refined and updated. Therefore, when interpreting corporate sustainability performance, users should consider both the initial disclosure and subsequent revisions to gain a more comprehensive view.

Figure 2. Interval between the Upload Date of 2024 Sustainability Reports and the Upload Date of Revised Reports for Listed and OTC Companies

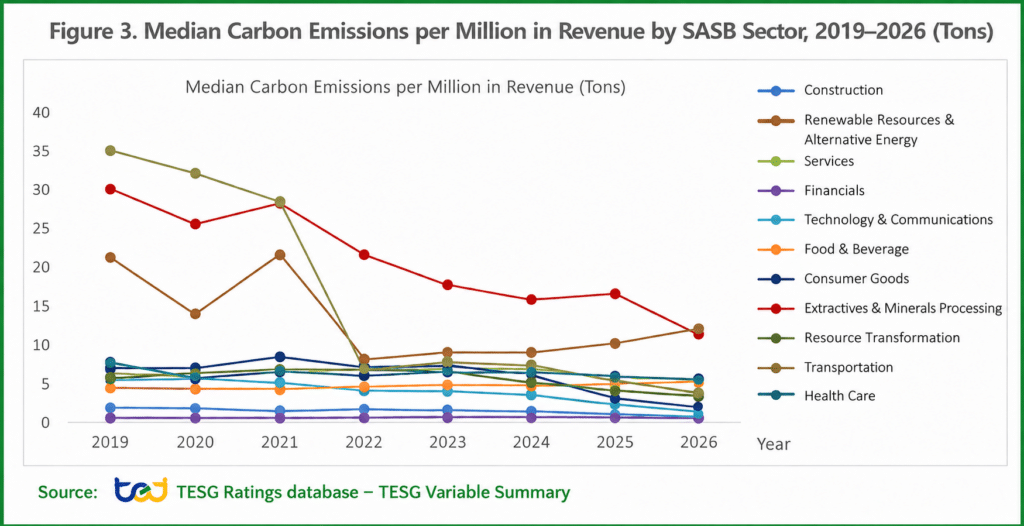

In assessing cross-industry ESG performance, incorporating SASB materiality weights helps better identify differences in risk exposure and governance responses across sectors. First, in terms of greenhouse gas emissions, industries with higher environmental impact, such as Extractives & Minerals Processing and Transportation, show significantly higher median carbon emissions per million in revenue than other sectors. Although these figures have been declining, the pace of improvement remains constrained by industry-specific production processes.By contrast, sectors such as Financials, Technology & Communications, and Services generally have lower carbon intensity, as their business models rely less on physical assets, as shown in Figure 3.

Figure 3. Median Carbon Emissions per Million in Revenue by SASB Sector, 2019–2026 (Tons)

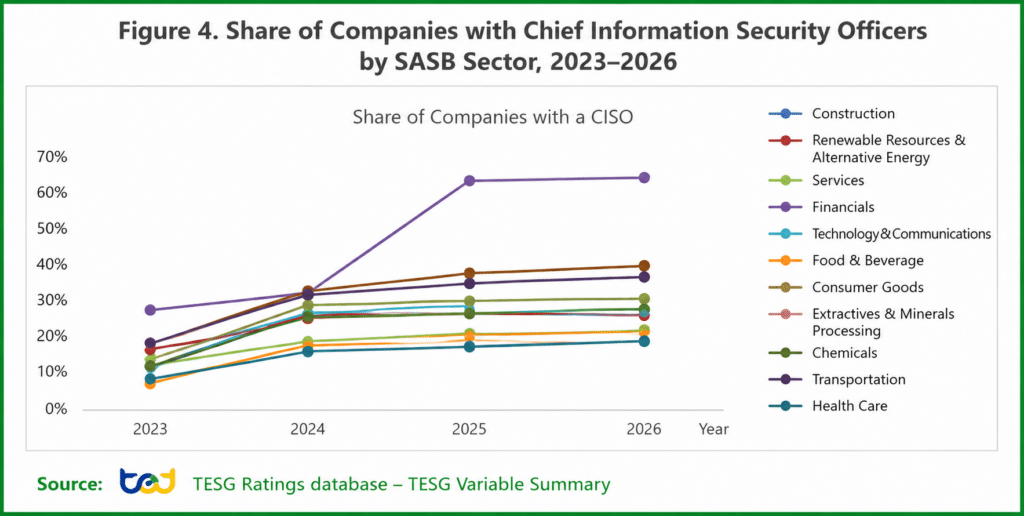

Data security has become a key issue under the social dimension of ESG. By appointing Chief Information Security Officers (CISOs) and establishing related governance mechanisms, companies can strengthen the identification, management, and oversight of cybersecurity risks, translating issue materiality into concrete governance actions.

Under Taiwan’s Regulations Governing Establishment of Internal Control Systems by Public Companies, companies meeting certain criteria are required to appoint a CISO and establish a dedicated information security unit. According to SASB industry classification, Financials, Health Care, and Technology & Communications all identify data security as a highly material issue.

As shown in Figure 4, the overall CISO appointment rate increased significantly from 2023 to 2026, with the most notable improvement in the financial sector. However, the appointment rates in Technology & Communications and Health Care remain relatively low, suggesting that industries highly dependent on data and privacy protection still have room to strengthen their cybersecurity governance mechanisms.

Figure 4. Share of Companies with Chief Information Security Officers by SASB Sector, 2023–2026

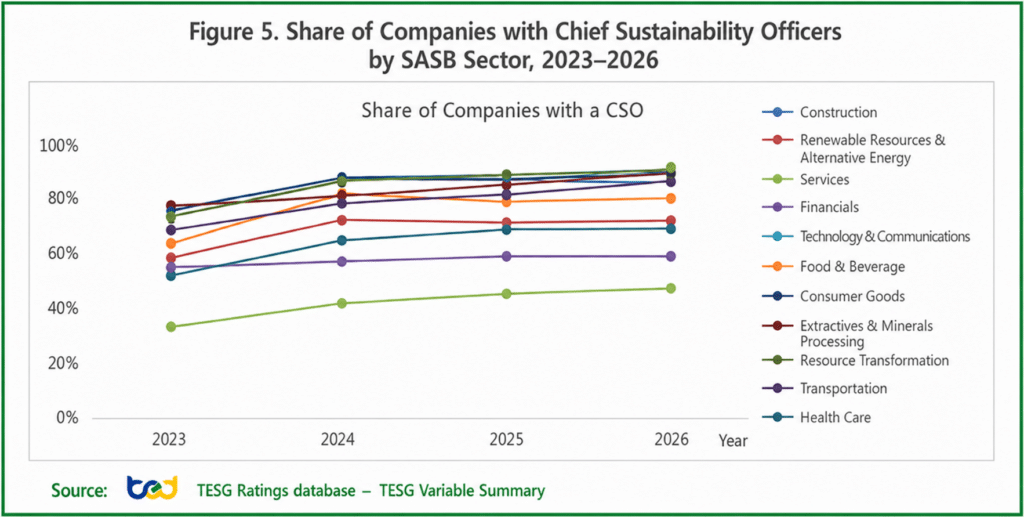

The appointment of Chief Sustainability Officers (CSOs) serves as an indicator of corporate commitment to sustainability governance. Unlike CISOs, whose appointment is subject to explicit regulatory requirements, CSO appointments are mainly driven by the FSC’s Sustainable Development Action Plans for TWSE- and TPEx-Listed Companies, reflecting companies’ growing emphasis on sustainability.

As shown in Figure 5, the overall appointment rate has reached a relatively high level, suggesting that most industries have moved beyond the initial stage of governance framework establishment and entered a phase of deeper governance integration. In sectors such as Consumer Goods, Construction, and Resource Transformation, where climate, resource, and supply chain issues have significant financial implications, the focus is shifting toward linking decarbonization and resource efficiency with operating performance and capital allocation.

By contrast, growth in the Services and Financials sectors has slowed, indicating that sustainability functions are increasingly embedded into risk management, investment and financing, and human resources systems. Going forward, the key to competitiveness lies not only in whether a company appoints a CSO, but also in whether the role can drive cross-functional integration, embed material ESG issues into decision-making, and translate them into measurable performance and long-term value creation.

Figure 5. Share of Companies with Chief Sustainability Officers by SASB Sector, 2023–2026

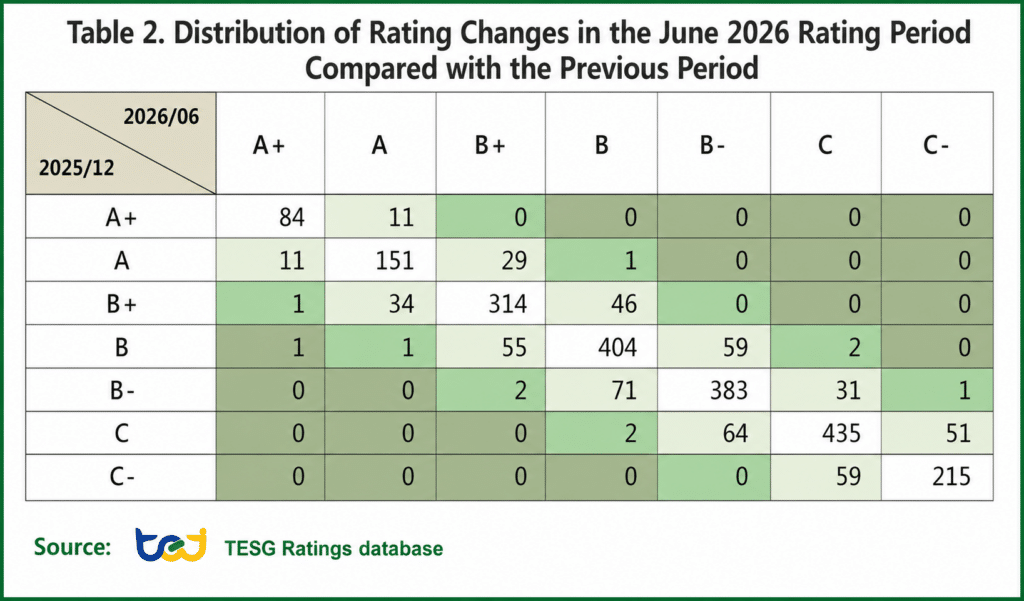

This rating update is mainly based on 2024 sustainability data. As the overall rating methodology remained relatively stable, most companies stayed within their original rating tiers or moved only slightly. The results show that 301 companies were upgraded and 231 companies were downgraded this period. Among them, 11 companies changed by more than two rating levels, mainly due to industry classification adjustments, changes in group control type, CISO appointments, and major negative ESG events.

Significant rating changes were mainly driven by continuous updates to daily, monthly, and quarterly indicators, as well as some companies’ subsequent sustainability report revisions and data corrections. Overall, rating movements reflect adjustments from more refined data and updated information, rather than structural changes in corporate sustainability performance.

TESG ratings are divided into seven grades from A+ to C-. The rating changes from the previous period are summarized in the table below.

Table 2. Distribution of Rating Changes in the June 2026 Rating Period Compared with the Previous Period

TEJ’s TESG Rating helps companies evaluate their performance and disclosure depth across the three ESG pillars: environmental, social, and governance. By offering multi-dimensional indicators, TEJ supports companies in understanding international trends and strengthening sustainability disclosure.

TEJ’s Sustainability Solutions provide one-stop support from information disclosure and risk analysis to decision-making applications, helping companies and financial institutions enhance sustainability resilience and align with international standards.